1 Rule, 3 Stocks: Why One Legendary Investor Would Choose These Stocks Above Any Others Right Now

Charlie Munger was one of the greatest investors to ever live. Sadly, he is no longer with us; however, his investment philosophy lives on. At the core of that philosophy was Munger’s desire to buy high-quality stocks at reasonable prices.

With that in mind, I’ve done some digging; these are the three companies that I think Munger would find irresistible right now.

Image source: Getty Images.

S&P Global

First up is S&P Global (SPGI 0.40%). With a history stretching back more than 150 years, Munger would be impressed with the company’s staying power. Nowadays, S&P generates a subscription-heavy mix of revenue through several segments. It issues credit ratings, manages benchmark indexes (such as the S&P 500), and provides detailed analytics to financial professionals. In short, the company possesses an unassailable moat around its core businesses, built on its prestige and reputation.

Today’s Change

(-0.40%) $-1.71

Current Price

$424.43

Key Data Points

Market Cap

$127B

Day’s Range

$421.34 – $428.27

52wk Range

$381.61 – $579.05

Volume

3.4M

Avg Vol

2.5M

Gross Margin

62.55%

Dividend Yield

0.91%

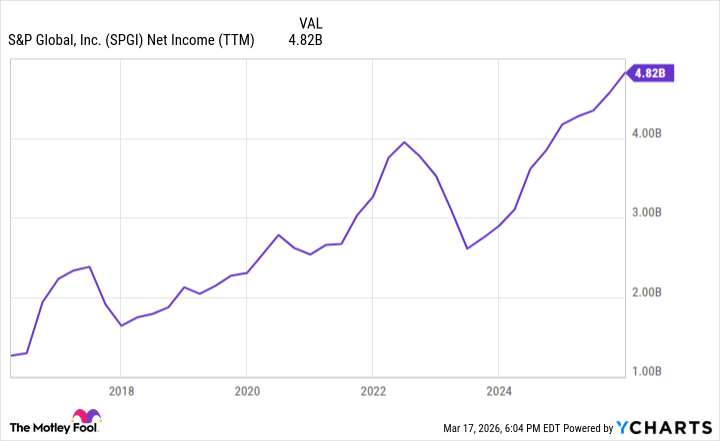

Yet it’s not just the company’s pedigree or revenue streams that would impress the legendary investor. S&P boasts fat margins. Over the last 10 years, its gross margin has averaged 65%, while its operating margin has hovered near 43%. All in all, S&P Global has the type of underlying business that always captured Munger’s attention: It quietly grinds away, compounding income at a steady rate, all while flying under the radar of the latest trends.

SPGI Net Income (TTM) data by YCharts

Granted, there are areas Munger wouldn’t be thrilled with — for example, the stock’s valuation. Shares currently trade with a price-to-earnings (P/E) multiple of 29, which is right around the market average. Yet overall, with shares trading within 10% of their 52-week low, Munger would be eager to buy S&P Global on this most recent dip.

Fair Issac

Next up is another financial stock, Fair Issac (FICO +1.18%). Perhaps even more than S&P Global, Fair Issac fits the bill of a Munger dream investment. The company operates behind a deep, wide moat built around the mortgage application process.

In brief, Fair Issac is the company behind FICO scores, which determine eligibility and lending rates for a wide range of loans, from mortgages to auto loans. In turn, FICO earns a steady stream of business generating those credit scores. In addition, the company operates a subscription-based software unit, focused on fraud detection and customer management.

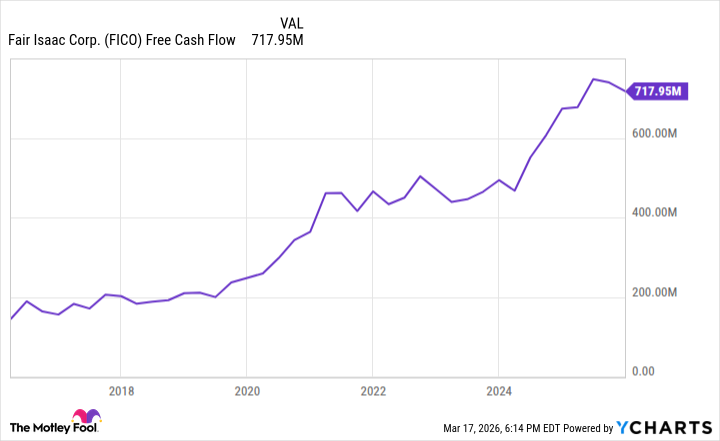

All this results in exceptional profitability. The company’s gross margin now stands at 83%, having grown from 67% a decade ago. In addition, another figure Munger would love is Fair Issac’s consistent free-cash-flow growth. Trailing-12-month free cash flow has increased a stunning 394% over the last 10 years and now stands at $718 million.

FICO Free Cash Flow data by YCharts

Munger’s main complaint with Fair Issac would probably be its leveraged buyback — a mechanism in which a company borrows cash to finance its share repurchases. In addition, he wouldn’t love the stock’s P/E ratio of 44, which remains above the market average.

However, given that, as of this writing (on March 15), shares are trading within 6% of the stock’s 52-week low, I think Munger would still see a massive opportunity in Fair Issac stock.

Today’s Change

(1.18%) $13.18

Current Price

$1126.34

Key Data Points

Market Cap

$27B

Day’s Range

$1097.23 – $1127.08

52wk Range

$1068.67 – $2217.60

Volume

12K

Avg Vol

318K

Gross Margin

82.86%

Home Depot

Last, there’s Home Depot (HD 2.05%). This stalwart of the home improvement industry has found its stock in the cellar. As of this writing, shares are trading within 4% of a 52-week low. That fact alone might not have drawn Munger’s interest, but the company’s long history of success, coupled with strong fundamentals, certainly would.

Home Depot is a dominant home improvement retailer, with approximately 2,300 stores. For the last 25 years, the company has delivered a stable gross margin averaging around 32%. In addition, Home Depot generates over $2 billion in quarterly free cash flow.

If there is one thing Munger wouldn’t like about Home Depot, it would be its balance sheet. The company’s net debt has grown by more than 250% over the last 10 years to nearly $64 billion. Munger would want to see that figure reverse course, and the sooner the better.

Today’s Change

(-2.05%) $-6.73

Current Price

$321.48

Key Data Points

Market Cap

$319B

Day’s Range

$320.30 – $330.00

52wk Range

$320.26 – $426.75

Volume

234K

Avg Vol

4.1M

Gross Margin

31.33%

Dividend Yield

2.88%

Nonetheless, I still think he would jump at the chance to scoop up shares of this iconic retailer at bargain-basement prices. Similarly, those who want to invest like Charlie Munger might consider Home Depot, Fair Isaac, and S&P Global while their stocks are on sale.