Is the US Treasury pricing in ‘rate hikes’? More precisely, the market is pricing in ‘QE’!

Amid escalating geopolitical conflicts in the Middle East and surging oil prices, there has been an unusual pricing of interest rate hikes in the U.S. rates market. Morgan Stanley believes that while the Treasury bond market appears to be pricing in a year-end rate hike by the Federal Reserve, it is actually pre-pricing an upcoming massive ‘fiscal stimulus’ package from the U.S. government. In the post-pandemic era, investors’ expectations regarding policy responses to crises have fundamentally shifted: rather than waiting for central banks to cut interest rates to rescue markets, they are now betting on direct ‘fiscal intervention’ by governments.

Amid escalating geopolitical tensions in the Middle East and surging oil prices, an unusual pricing for rate hikes has emerged in the U.S. interest rate market: On Friday last week, the market briefly priced in a probability of over 50% for a Federal Reserve rate hike in December this year.

In its latest report, Morgan Stanley’s interest rate strategy team pointed out that while the Treasury bond market appears to be pricing in a Fed rate hike by the end of the year, it is actually preemptively pricing in an upcoming large-scale ‘fiscal stimulus’ from the U.S. government.

The team believes that in the post-pandemic era, investors’ expectations regarding policy responses to crises have fundamentally shifted: rather than waiting for central banks to cut interest rates to stabilize markets, they are now betting on direct ‘fiscal intervention’ by governments.

This paradigm shift is reshaping the risk-aversion logic of U.S. Treasuries and the entire macro trading framework.

Unusual Pricing for Rate Hikes: What Is the Market Trying to Convey?

As the Iran conflict entered its third week, a rare phenomenon occurred in the U.S. interest rate market: On Friday last week, the market briefly priced in a probability of over 50% for a rate hike in December.

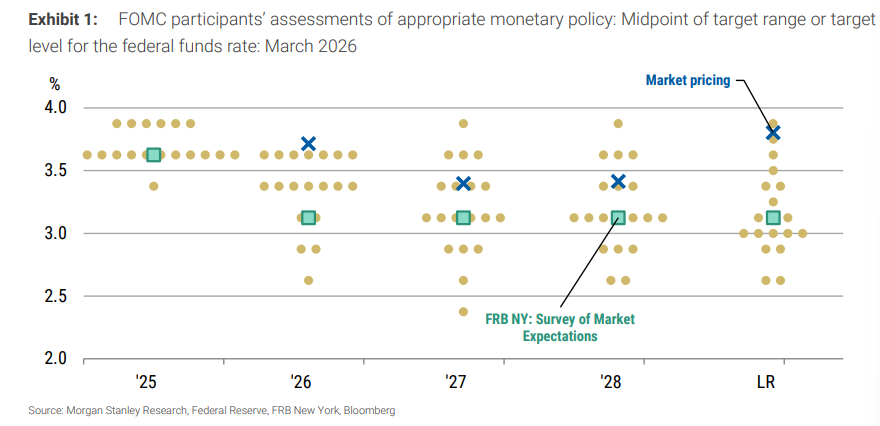

Compared with the Federal Reserve’s dot plot from March and the New York Fed’s surveys of primary dealers and market participants, the current market-implied path for the federal funds rate is significantly higher than expected at all time points—a divergence that has left many investors perplexed.

To explain this significant divergence, Morgan Stanley’s interest rate strategy team conducted an ingenious reverse-engineering of probabilities.

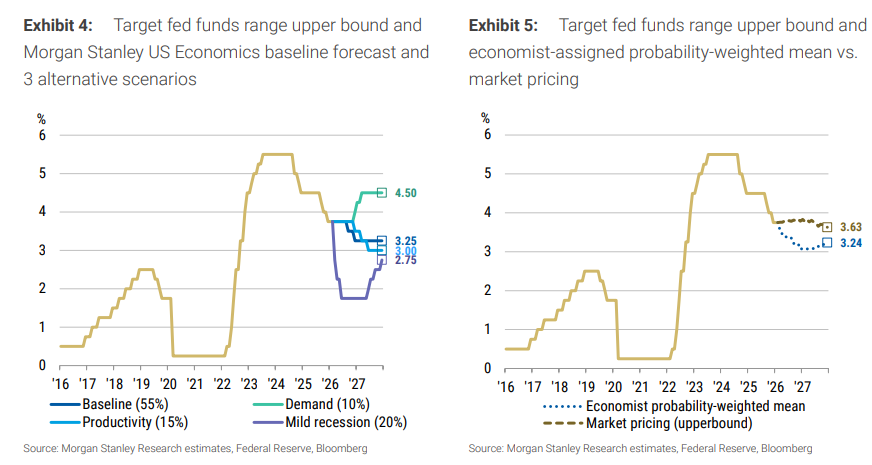

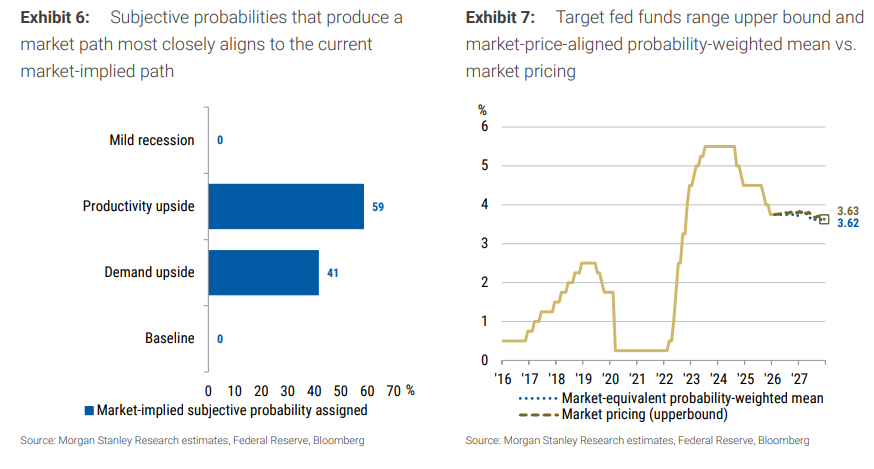

Morgan Stanley compared four macroeconomic scenarios predicted by its economists—baseline (55%), upside demand (10%), upside productivity (15%), mild recession (20%)—with market pricing. The results showed that the economist-weighted endpoint for the federal funds rate was 3.24%, while market pricing reached as high as 3.63%.

To align with this market pricing, Morgan Stanley found that extreme adjustments to probabilities were required: increasing the probability of ‘upside demand’ from 10% to 41%, raising ‘upside productivity’ to 59%, while reducing both the baseline and mild recession probabilities to zero.

This implies that the market has almost entirely ruled out the possibility of economic weakness, fully betting on a strong pulse of demand growth.

In the context of an energy shock and surging oil prices, such pricing appears irrational — unless the market is confident that there exists a substantial external force capable of offsetting the energy burden.

Morgan Stanley’s answer is: fiscal stimulus exceeding expectations.

From ‘Central Bank Bailouts’ to ‘Government Gap-Filling’ — A Post-Pandemic Paradigm Shift

Morgan Stanley wrote in its report:

“The U.S. interest rate market is now focused on proactive government intervention rather than central bank intervention.”

The team pointed out that the pandemic and its aftermath have fundamentally altered investors’ perceptions of crisis policy responses.

Before the pandemic, the market’s reflex was clear: growth crisis → central bank rate cuts → buy government bonds. However, today, investors seem to have formed a new belief — when faced with a growth crisis, the first responder is no longer the central bank but the government, as central banks are preoccupied with waves of inflation issues and may respond too slowly or too late.

In the U.S., investors may be “looking through” the demand destruction effect of high oil prices and instead pricing in the gap-filling effect of fiscal stimulus.

If fiscal stimulus fills the demand gap caused by high oil prices, then energy inflation will exist in “isolation” — meaning demand remains intact but inflation stays elevated, which would precisely force the Federal Reserve to abandon easing and possibly even turn hawkish.

Multiple factors are supporting this macroeconomic shift in expectations:

- The unusual trend in inflation expectations. The one-year forward one-year (1y1y) CPI inflation swap rate, which Morgan Stanley continuously tracks, rose instead of falling after the outbreak of the conflict (contrasting sharply with the decline seen after the ‘Liberation Day’ incident on April 2 last year). As long as the positive correlation between oil prices and the 1y1y inflation swap remains unbroken, it indicates that oil prices have not yet reached the critical point of destroying demand. On the other hand, the market may be anticipating government intervention before demand destruction occurs.

- Europe has set a precedent. The Spanish government proposed a €5 billion energy relief plan, including VAT reductions and subsidies; the Portuguese government approved a bill allowing for temporary electricity price caps during the energy crisis.

However, Morgan Stanley emphasized that fiscal stimulus capable of explaining the current pricing behavior of U.S. Treasuries must far exceed the supplementary military appropriations related to the Iran conflict. Currently, the Pentagon has secured approximately $840 billion in the FY26 base defense appropriation bill, with an additional $150 billion in supplementary appropriations through OBBBA. Morgan Stanley believes it is highly likely that the Treasury will finance the supplementary appropriations for the conflict by issuing Treasury bills (T-bills). The additional $200 billion in supplementary appropriations reported by the media will face significant challenges in passing, according to Morgan Stanley’s public policy strategists. The scale of pure military appropriations alone is insufficient to generate a growth impulse strong enough to force the Federal Reserve to pivot – if the market is indeed pricing in a hawkish pivot, then the fiscal measures it anticipates must directly target the private sector most impacted by energy costs.

Notably, Morgan Stanley’s public policy strategists further pointed out that the political maneuvering surrounding the supplementary appropriations – as well as any targeted fiscal policies linked to economic conditions – could evolve as the conflict persists. The longer the conflict continues, the higher the probability of supplementary appropriations being approved, accompanied by the increased likelihood of additional economic stimulus being passed alongside it.

Other market signals are also corroborating expectations of fiscal expansion:

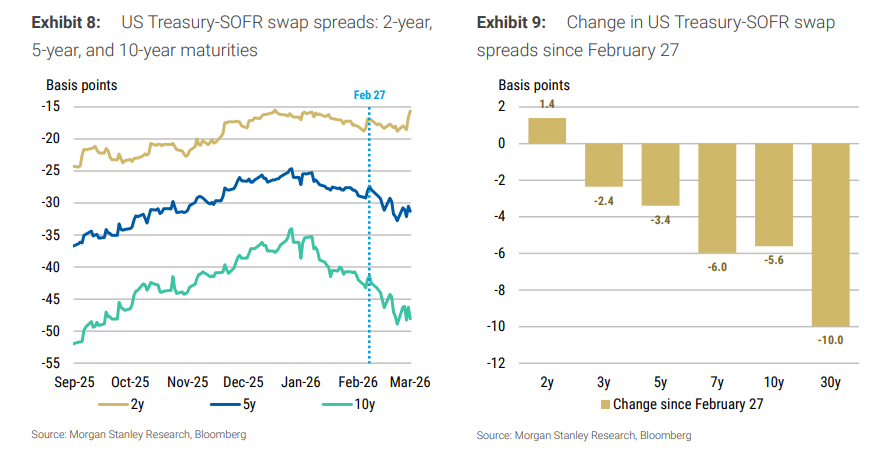

U.S. equities have shown unexpected resilience – the S&P 500 has fallen only about 6% since February 27, significantly outperforming the 13% decline seen during the escalation of the Russia-Ukraine conflict. U.S. Treasuries have notably weakened relative to SOFR swaps – since February 27, the 30-year Treasury-SOFR spread has narrowed by 10 basis points, and even the 2-year Treasuries began underperforming SOFR swaps before the introduction of new capital rules, a classic signal of market concerns over increased Treasury supply.

Meanwhile, Treasuries failed to provide the expected hedging protection during the downturn in risk assets – on one hand, the Federal Reserve was not dovish enough, and on the other, the market was pricing in more Treasury supply driven by fiscal expansion.

$58 billion selloff – Are major Middle Eastern investors cashing out?

Compounding the woes for U.S. Treasuries, beyond the massive supply expectations from domestic fiscal expansion, real selling pressure from external sources has also arrived: Middle Eastern countries may be conducting large-scale liquidations.

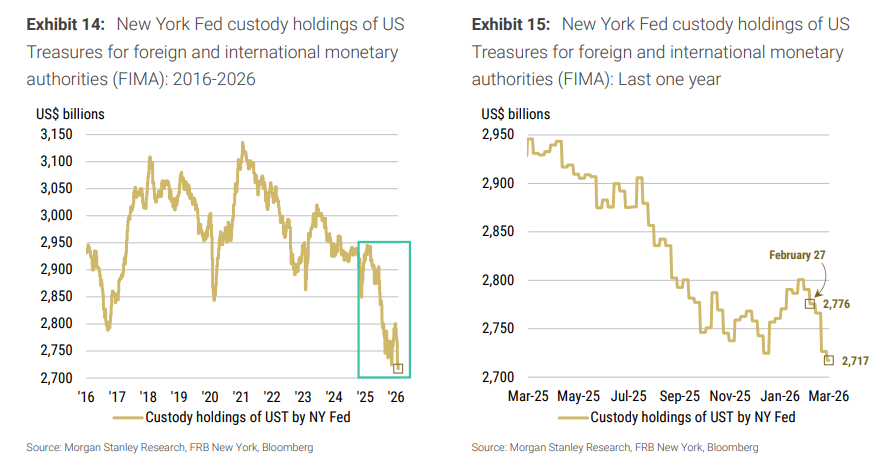

The report disclosed that as of January 2026, Kuwait, Saudi Arabia, and the United Arab Emirates collectively held up to $313.5 billion in U.S. Treasury bonds, with all three countries showing an upward trend in their holdings since 2022.

However, the custodial data from the New York Federal Reserve issued a sharp warning: since February 25 (the outbreak of the conflict), foreign monetary authorities have net sold approximately $58 billion worth of U.S. Treasury bonds.

The destination of the funds is even more alarming.

During the same period, the New York Fed’s reverse repo facility for foreign monetary authorities (FIMA RRP) increased by only $3 billion—indicating that the proceeds from the sell-off did not flow back into the “safe harbor” within the Fed system, and the funds likely truly exited the U.S. bond market.

Against the backdrop of the conflict, the market has reason to speculate that Middle Eastern countries are liquidating U.S. Treasuries to raise funds for defense and potential reconstruction costs.

An underestimated paradigm shift: no longer waiting for central banks to cut interest rates to rescue markets, but betting on governments directly implementing “fiscal stimulus.”

In response to this complex situation, Morgan Stanley advises investors to remain neutral on the duration and curve direction of U.S. Treasury bonds, awaiting further clarity on the impact of the Iran conflict on monetary and fiscal policies.

On the trading side, Morgan Stanley maintains a long position in the spread between the two-year U.S. Treasury bond (maturing September 2027) and the SOFR swap at -14.8bp, targeting -14bp, with a trailing stop-loss at -18.5bp.

However, beyond specific levels, what truly merits deep reflection from investors in this report is a potentially underestimated paradigm shift: in the post-pandemic world, when markets begin viewing fiscal stimulus rather than central bank rate cuts as the first-response tool to crises, the safe-haven attributes of government bonds, the pricing logic of inflation expectations, and even the entire macro-trading framework need recalibration.

On the surface, the market is pricing in “rate hikes,” but in reality, it is pricing in “quantitative easing”—only this time, the protagonist is not the Federal Reserve, but the U.S. government.