The specter of stagflation looms over the globe! Trump’s postponement of measures fails to mask fears as global bond markets briefly mirrored the disastrous performance seen in 2022.

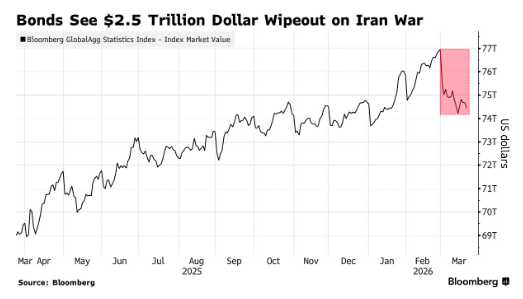

Although Trump abruptly announced a five-day postponement of the threat to destroy Iran’s power plants, the specter of stagflation triggered by the Iran conflict has not been reversed. This panic once led to a global bond market value loss of over $2.5 trillion in March and could result in the largest single-month decline in more than three years.

Although Trump’s sudden announcement of a five-day postponement of the threat to destroy Iran’s power plants has driven a rebound in both global stock and bond markets, with oil prices falling accordingly, the shadow of stagflation triggered by the Iran conflict has not been reversed. This panic once caused the global bond market value to evaporate by more than $2.5 trillion in March and could result in the largest monthly decline in over three years.

On the 23rd local time, U.S. President Trump posted on the social media platform ‘Truth Social,’ stating, “The United States and Iran have had very good and productive talks over the past two days.” He also noted that he had ordered the suspension of all military strikes on Iran’s power plants and energy infrastructure for five days, provided that the ongoing meetings and discussions are successful.

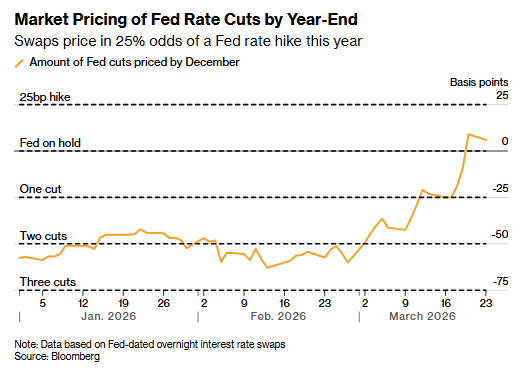

As a result, yields on U.S. Treasury bonds of all maturities fell across the board on Monday, with the two-year Treasury yield, which is most sensitive to changes in Fed policy, leading the decline. At the same time, traders completely abandoned bets on the Fed tightening monetary policy this year, shifting instead to reprice expectations of some easing. Prior to Trump’s remarks, the money market had almost fully priced in expectations of a 25-basis-point rate hike.

Global bonds revisit brutal conditions seen in 2022

Nevertheless, since the end of February when the U.S. and Israel launched military strikes against Iran, the surge in oil prices has accelerated inflation, continuously eroding the real value of fixed-rate bond coupons, causing fierce sell-offs in the bond market. Although the scale of the bond market’s loss in value is smaller than the approximately $11.5 trillion loss in global equities, its sharp decline has been particularly unusual—during periods of geopolitical turmoil, bonds are typically considered a safe haven for funds.

“The market has begun pricing in the upcoming stagflation shock,” said Kathryn Rooney Vera, Chief Market Strategist at StoneX Group Inc., during an interview. “The longer the conflict persists, the higher oil prices may rise.”

Before Trump announced the U.S.-Iran negotiations, relevant indices showed that the total market value of global government bonds, corporate bonds, and securitized debt had fallen from nearly $77 trillion at the end of February to $74.4 trillion, marking a 3.1% drop for the month, potentially the largest decline since September 2022—when the Federal Reserve was in the midst of an aggressive interest rate hike cycle.

Government bonds led the declines: The Bloomberg Global Sovereign Bond Index plummeted 3.3% in March, while the corporate bond index fell by 3.1%.

As the market bet that the Federal Reserve would be forced to raise interest rates to combat inflation, U.S. Treasury yields once climbed to multi-month highs, and U.S. Treasuries declined for a third consecutive week. Asian markets were pressured simultaneously, with government bond yields in India, Japan, and South Korea rising; Australia’s 10-year Treasury yield hit its highest point since 2011 on Monday, while New Zealand’s government bond yields reached a new high since May 2024.

The selloff in the bond market accelerated on Monday, triggered by Trump’s earlier threat: If Iran does not reopen the Strait of Hormuz, it will strike its power plants; Iran immediately retaliated, stating that if the U.S. acts, it will “completely blockade” this critical channel.

BNP Paribas’ interest rate strategists noted in a client report last week that if energy prices remain high and unemployment stays stable, the Federal Reserve’s April policy meeting may signal the possibility of a rate hike. Joachim Nagel, a member of the European Central Bank’s Governing Council, also stated that if the conflict with Iran further increases inflationary pressures, the ECB may need to consider raising rates as early as next month.

Trinh Nguyen, Senior Economist at Natixis Hong Kong, stated: ‘Persistently high inflationary pressures are constraining the central banks’ policy space, forcing some central banks to raise interest rates even during an economic downturn in order to curb inflation and prevent their currencies from depreciating.’

Editor/Lambor