Global Market Insights Samsung Electronics And 2 Other Stocks Estimated To Be Trading Below Their Intrinsic Value

In a global market environment characterized by geopolitical tensions and energy market volatility, investors are seeing major U.S. stock indexes rally amid signs of potential de-escalation in the Middle East. As markets navigate these uncertainties, identifying stocks trading below their intrinsic value can provide opportunities for those looking to capitalize on potential undervaluation in sectors resilient to current economic shifts.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Xi’an NovaStar Tech (SZSE:301589) | CN¥155.53 | CN¥307.44 | 49.4% |

| Nordisk Bergteknik (OM:NORB B) | SEK11.35 | SEK22.55 | 49.7% |

| Nemetschek (XTRA:NEM) | €64.80 | €129.27 | 49.9% |

| Higold Group (SZSE:001221) | CN¥61.75 | CN¥122.39 | 49.5% |

| Haypp Group (OM:HAYPP) | SEK120.80 | SEK238.56 | 49.4% |

| Geely Automobile Holdings (SEHK:175) | HK$23.82 | HK$47.28 | 49.6% |

| Elekta (OM:EKTA B) | SEK54.45 | SEK107.92 | 49.5% |

| Dana Gas PJSC (ADX:DANA) | AED0.871 | AED1.74 | 49.9% |

| B&S Group (ENXTAM:BSGR) | €5.85 | €11.66 | 49.8% |

| Airbus (ENXTPA:AIR) | €165.14 | €326.99 | 49.5% |

Let’s take a closer look at a couple of our picks from the screened companies.

Overview: Samsung Electronics Co., Ltd. operates globally in consumer electronics, information technology and mobile communications, and device solutions, with a market cap of approximately ₩1.13 trillion.

Operations: The company’s revenue segments include Device Solutions (₩130.13 billion), Device Experience (₩187.97 billion), SDC (₩29.84 million), and Harman (₩15.78 million).

Estimated Discount To Fair Value: 10.5%

Samsung Electronics is trading at ₩186,600, slightly undervalued compared to its estimated future cash flow value of ₩208,493.38. The stock trades at 10.5% below its fair value estimate and shows robust earnings growth expectations of 34.7% annually over the next three years, outpacing the Korean market average. Recent strategic moves include a significant investment in AI and semiconductor technology and a new partnership with AMD for advanced memory solutions, potentially enhancing future cash flows.

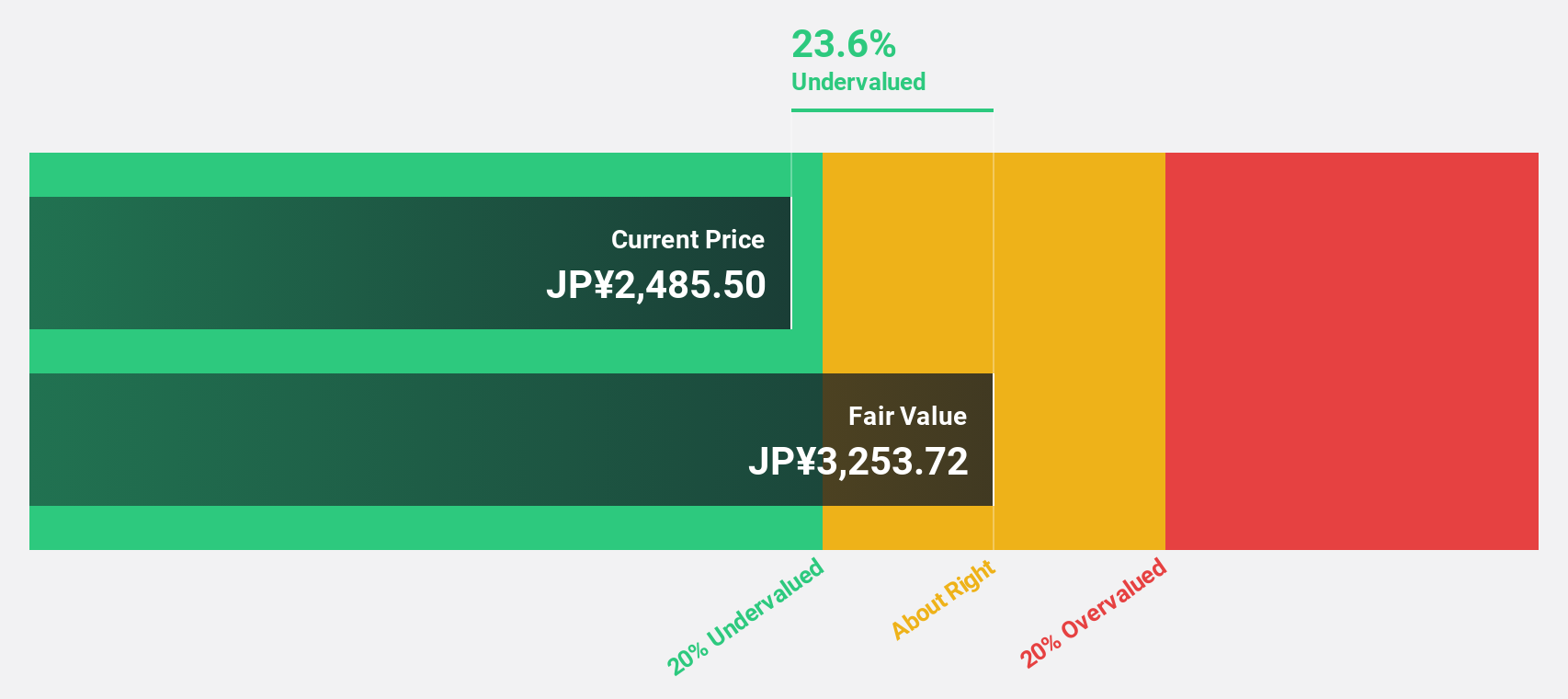

Overview: Kakaku.com, Inc., along with its subsidiaries, offers purchase support and restaurant review services in Japan, with a market cap of ¥421.69 billion.

Operations: The company’s revenue segments include Tabelog at ¥38.52 billion, Kakaku.Com at ¥23.98 billion, Kyujin Box at ¥18.67 billion, and Incubation at ¥9.54 billion.

Estimated Discount To Fair Value: 13.6%

Kakaku.com is trading at ¥2,227.5, undervalued by 13.6% compared to its estimated future cash flow value of ¥2,579.42. The company forecasts an annual revenue growth of 11%, outpacing the JP market average of 5.4%. Despite a slight decline in net income year-over-year, recent organizational changes include establishing an AI Product Development Department to enhance operational efficiency and governance, potentially supporting future cash flows and profitability improvements.

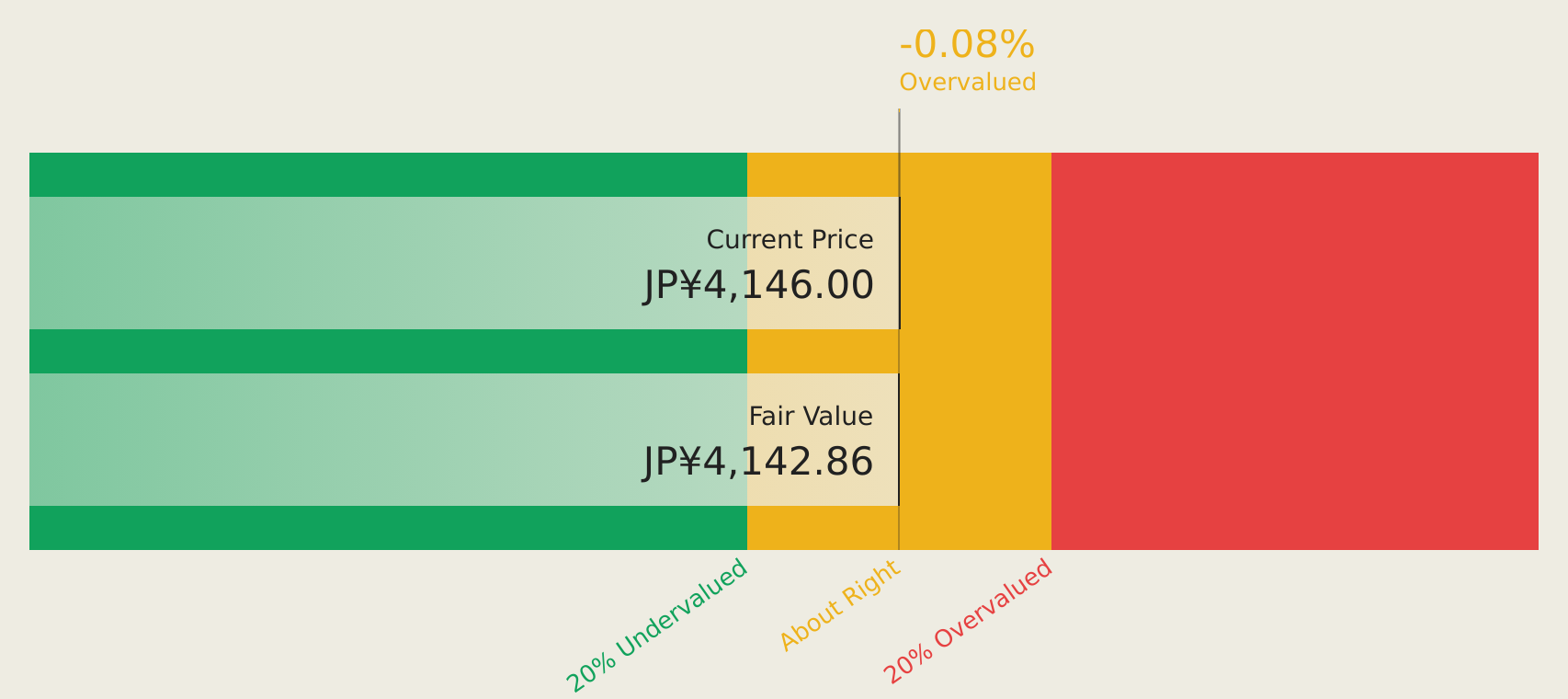

Overview: Murata Manufacturing Co., Ltd. is engaged in the development, manufacturing, and sale of ceramic-based passive electronic components and solutions both in Japan and globally, with a market cap of ¥6.33 trillion.

Operations: Murata Manufacturing generates revenue primarily from its Components segment, which accounts for ¥1.13 trillion, followed by the Devices and Modules segment at ¥656.54 billion.

Estimated Discount To Fair Value: 11.3%

Murata Manufacturing is trading at ¥3,783, slightly undervalued compared to its estimated future cash flow value of ¥4,263.5. The company expects significant annual earnings growth of 21.7%, outpacing the JP market’s 9.9%. Despite a recent decline in net income and a highly volatile share price, revised guidance anticipates increased revenue due to yen depreciation and rising demand for electronic components in AI servers and smartphones. Recent auditor changes may impact investor confidence short-term.

Key Takeaways

Searching for a Fresh Perspective?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice.

It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com