Bond Market Gets Nervous about Rising Inflation, Ballooning Debt, Sees Rate Hike. Mortgage Rates Jump to 6.46%

10-Year Treasury yield bounced to 4.35% on Friday, after dipping earlier in the week. 30-year Treasury near 5%. Entire Yield Curve above EFFR.

By Wolf Richter for WOLF STREET.

The 10-year Treasury yield rose 5 basis points in shortened trading on Friday on the release of the jobs report and closed at 4.35%. It had spent the first four days of the week backpedaling 14 basis points, after spiking by 47 basis points from 3.97% on February 27 to 4.44% on Friday March 27.

At 4.35% on Friday, the 10-year yield is where it had been in July 2025. And there were three rate cuts in between, as depicted by the Effective Federal Funds Rate (EFFR, blue line), which the Fed targets with its policy rates, and which the 10-year yield has been blowing off.

The bond market is now very edgy, with inflation fears front and center, followed by supply fears as it is facing Trump’s new budget, formally released on Friday, in which he asked for a 44% increase of the military budget to $1.5 trillion, which added to the concerns about the Treasury debt that has already been increasing at a rate of about $2.2 trillion a year that the bond market has to absorb, with new investors needing to be enticed in, and that may take higher yields (and lower prices for existing bond holders).

There has been a lot wailing and gnashing of teeth about the 10-year Treasury yield rising again, and dragging up economically important interest rates.

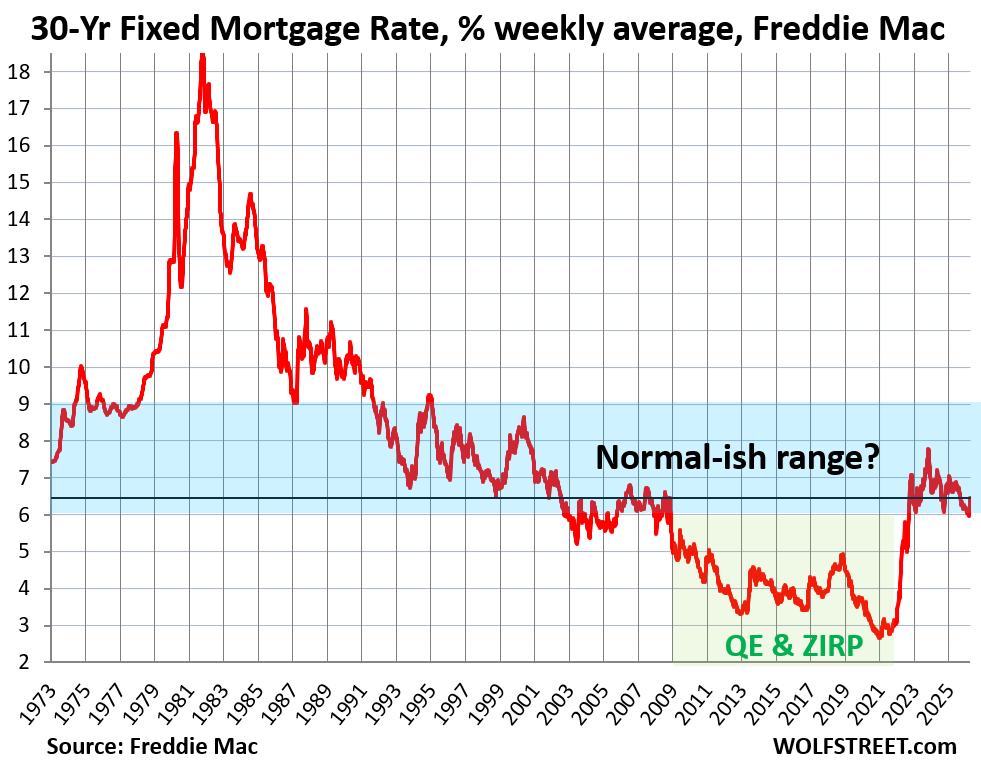

For example, and crucially, the average 30-year fixed mortgage rate, per Freddie Mac, has jumped by nearly 50 basis points since late February, to 6.46%.

Yields of corporate bond have jumped. The average yield of BBB-rated bonds, the low end of investment grade, jumped by 40 basis points since late February. Yields of BB-rated bonds, the high end of junk bonds, jumped by 60 basis points. Yields of B-rated junk bonds jumped by 80 basis points since late February (my cheat sheet for corporate credit ratings by ratings agency).

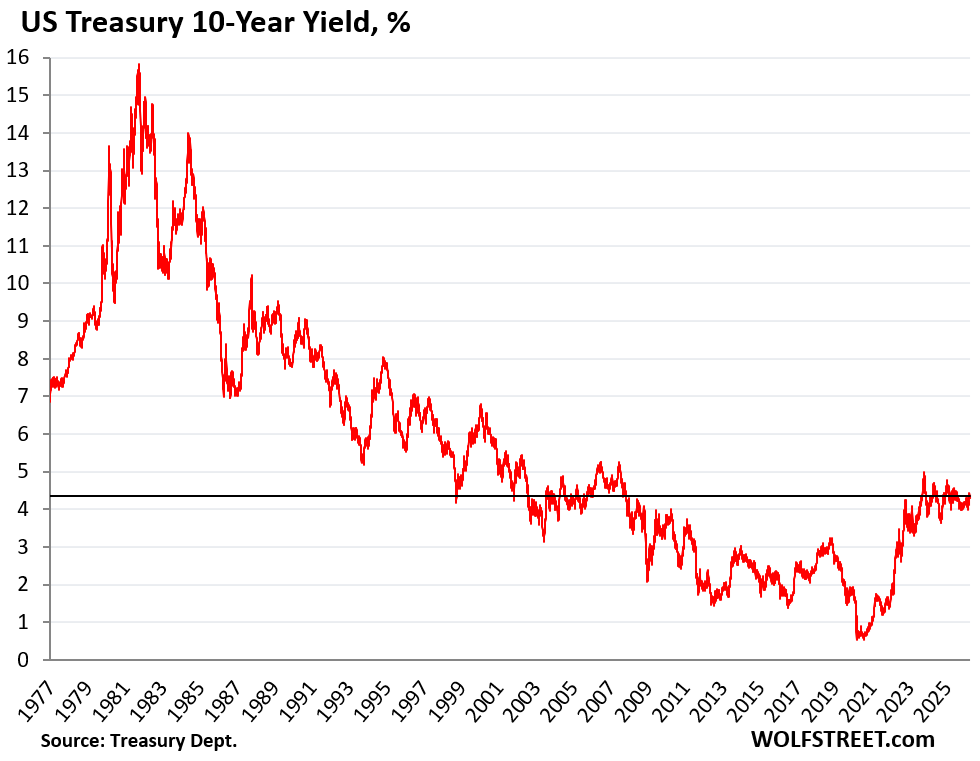

But Treasury yields are still relatively low in a historical context. It’s just that the years of QE and interest-rate repression by the Fed have distorted everything. And now there’s inflation, quite a bit of it, well above the Fed’s target, and once again accelerating. So for the Fed to be buying long-term Treasury securities to push down long-term yields is off the table.

The current 10-year Treasury yield is only about where it had been in 2007, before QE started, and it is much lower than in the decades before 2002.

The Dotcom Bubble and the accompanying big economic growth and very tight labor market occurred in the 1990s when the 10-year Treasury yield was mostly between 5% and 8%.

Bond prices rise when yields fall, and there was this magnificent 40-year bond bull market from 1981 through mid-2020, during which the 10-year yield zigzagged down from nearly 16% to 0.5%. But now there are inflationary pressures everywhere, and it’s a different ballgame than in 2008-2020.

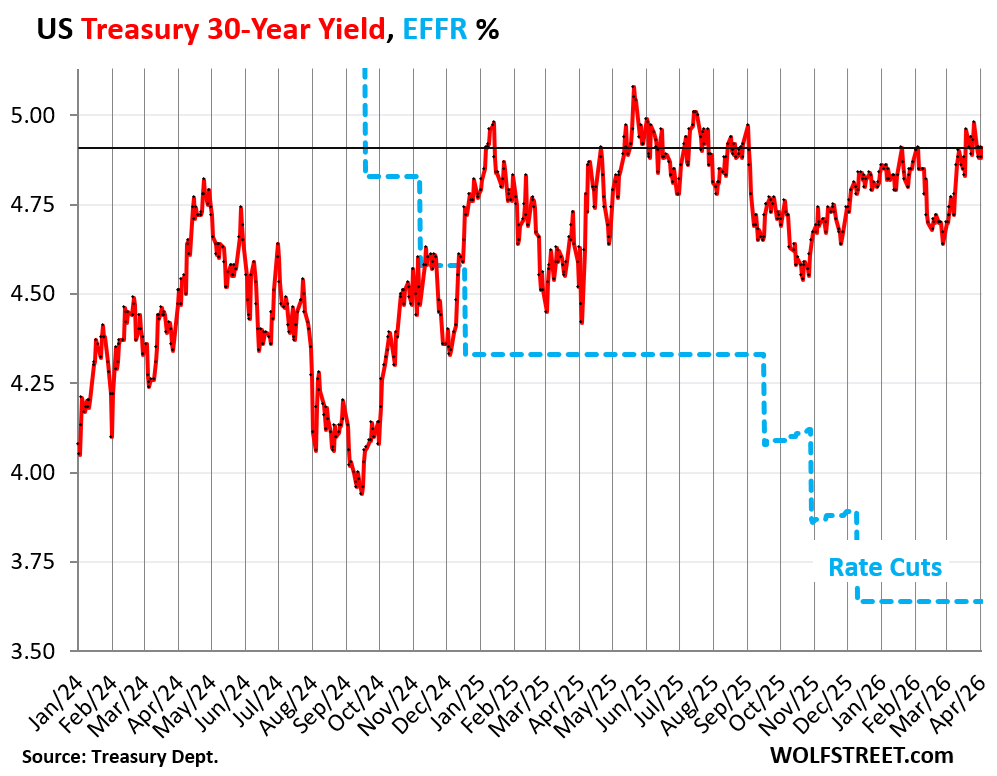

The 30-year Treasury yield rose by 3 basis points on Friday to 4.91%. It has been within a spitting distance of 5% since mid-March.

And it is higher now than it had been before the rate cuts even started in September 2024. The long-term bond market doesn’t care about rate cuts; in fact it worries about rate cuts if inflation still traipses around the economy, and the Fed is lax about it, or ignores it, or “sees through it.”

For holders of long-term paper, that’s a dreadful thought. They want a hawkish Fed that keeps inflation down with an iron fist. Reliably low inflation begets low long-term bond yields.

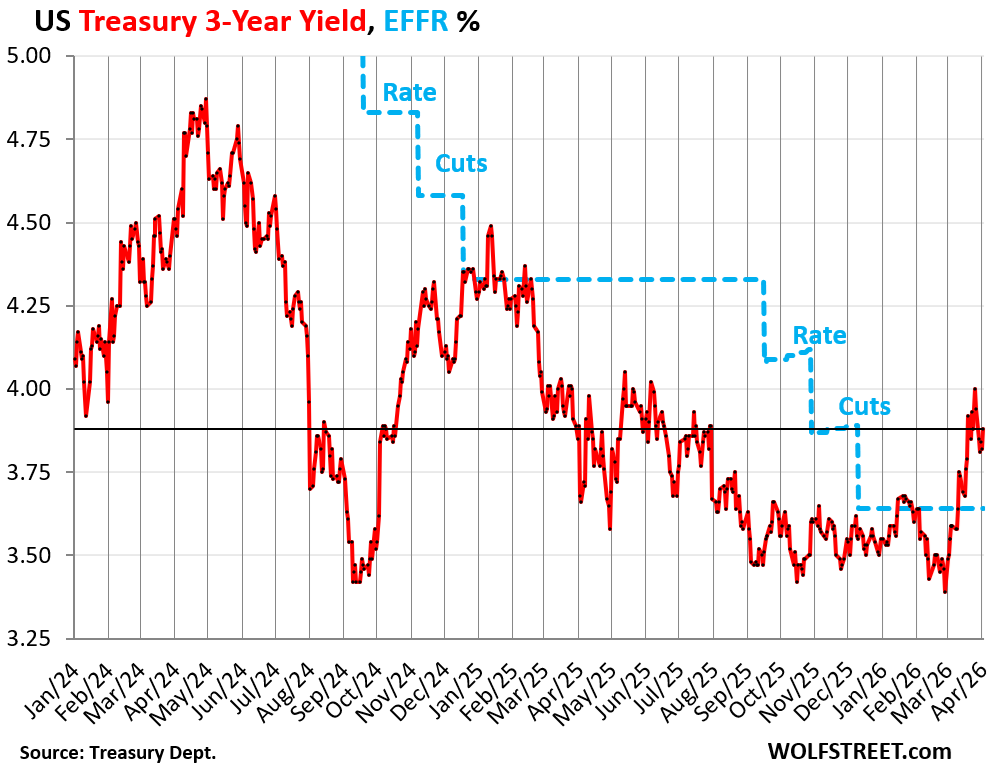

Yields from 1 year to 3 years had spiked in March as rate cuts were swept off the table, and a rate hike as the next move was put on the table.

The 3-year Treasury yield had spiked by 60 basis points in March through Friday last week, from 3.39%, when it was pricing in a rate cut, to 4.0% by Friday March 27, when it was pricing in a rate hike as the next move.

Over the first four days this week, it backpedaled 18 basis points. But on Friday April 3, it rose by 6 basis points and closed at 3.88%, so 20 basis points above the EFFR, and right where the EFFR had been before the last rate cut.

That end of the bond market is counting on a rate hike as the next move. And Friday’s jobs report on Friday gave it more confidence, after wobbling earlier in the week.

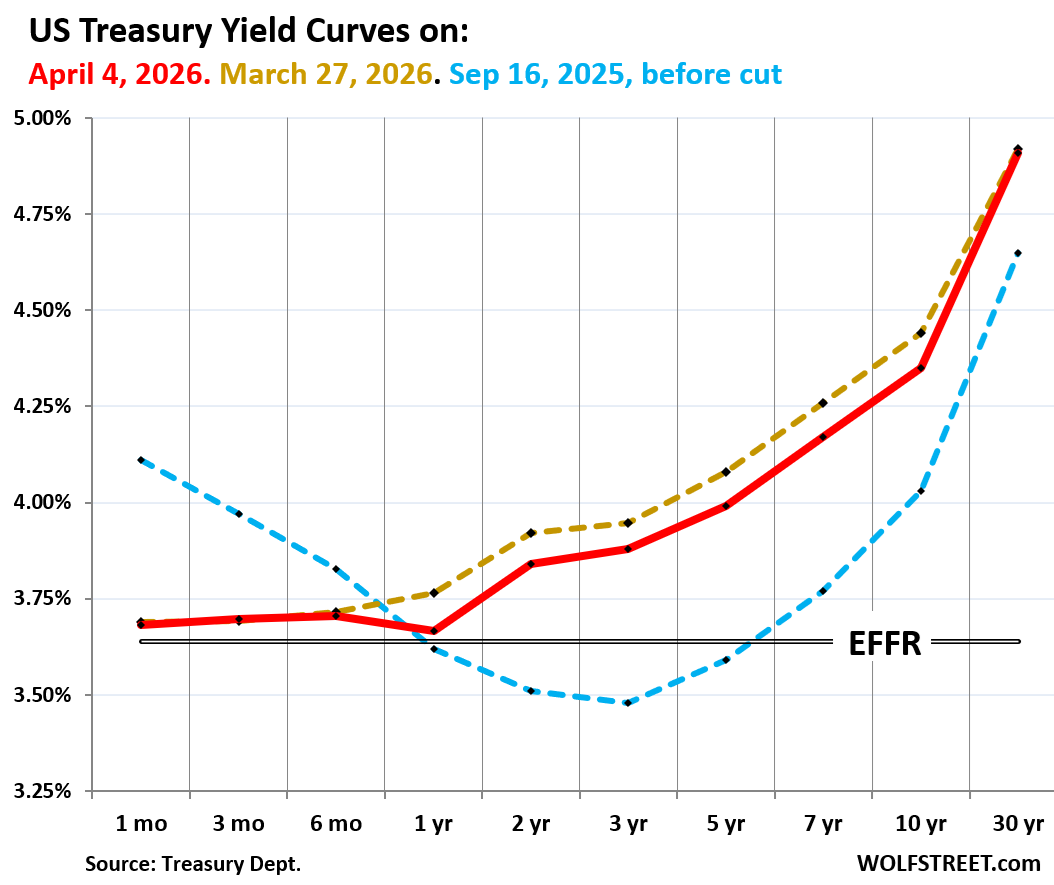

The Treasury yield curve.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates in 2025 and 2026:

- Red: Friday, Apri 3, 2026.

- Gold: March 27, 2026, near the recent high in yields.

- Blue: September 16, 2025, before the Fed’s first of three rate cuts in 2025.

In terms of the 1-year to 10-year yields, after the drop over the first four days, and the partial rebound on Friday, they ended the week a little lower than they had been a week earlier, on March 27. But all were higher than they’d been before the last three rate cuts, which started in September 2025.

The 30-year yield closed on Friday essentially unchanged from March 27.

And the 1-month through 6-month yields were roughly unchanged from March 27. They had been pushed down by the Fed’s rate cuts, and they don’t really move unless the Fed is expected to move in their window, which for the 6-month yields is up to about four to five months out. So that end of the bond market expects no move by the Fed over the next four to five months.

And since about mid-March, the entire yield curve has been above the EFFR (black double line), as the bond market gave up any rate-cut ambitions.

Mortgage rates follow. The real estate industry, which always wants low mortgage rates, needs to understand this: Instead of agitating for rate cuts, it needs to agitate for a hawkish Fed that cracks down on inflation. Low inflation and a hawkish Fed beget lower long-term Treasury yields, which beget lower mortgage rates. Rate cuts in face of accelerating inflation can be toxic for mortgage rates.

Since late February, the weekly measure by Freddie Mac of the average 30-year fixed mortgage rate has jumped by 48 basis points to 6.46%.

Outside of the period of QE and interest rate repression, mortgage rates are now roughly in the normal-ish range that prevailed before 2008, except for the period of very high inflation from the late 1970s through the late 1980s, when CPI topped out at just over 15%, and when mortgage rates topped out over 18%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Is Part Of A 2 Billion AI Debt Wave Shaking Credit Markets")