Seven Reasons to Buy the Dip in U.S. Tech Stocks

Goldman Sachs believes that technology stocks currently present a good buying opportunity, listing seven reasons.

According to Zhitong Finance APP, Goldman Sachs stated that now is a good time to buy the weak US tech sector on dips. This year, concerns over artificial intelligence’s disruptive changes and the Iran war have heavily impacted this segment. The bank listed seven reasons why the current valuation is attractive to investors.

At the beginning of 2026, the US tech sector encountered a difficult start as investors began to worry that artificial intelligence might fundamentally disrupt business models across various industries, while concerns persisted about surging capital expenditures by hyperscale data center operators.

The SPDR Technology Select Sector Index ETF (XLK.US) has fallen 5.7% this year and is down 10.4% from its peak on October 29 last year. However, in a report to clients written by Peter Oppenheimer, Global Equity Strategist at Goldman Sachs on Tuesday, it was noted that now could be an excellent time to start buying into the sector, referring to it as a ‘value opportunity’ and providing seven key reasons.

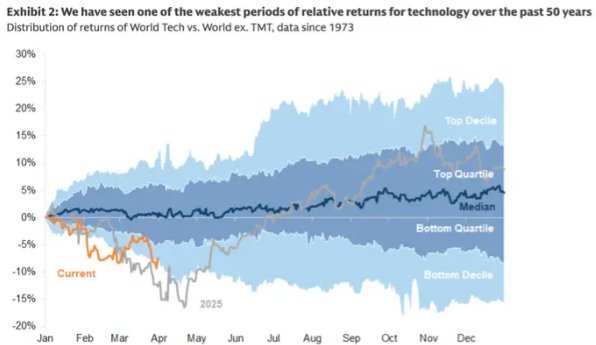

1. For the technology sector, this is one of the worst starts to a year since at least 1976 when viewed from the perspective of the past half-century, having retreated from higher valuation levels.

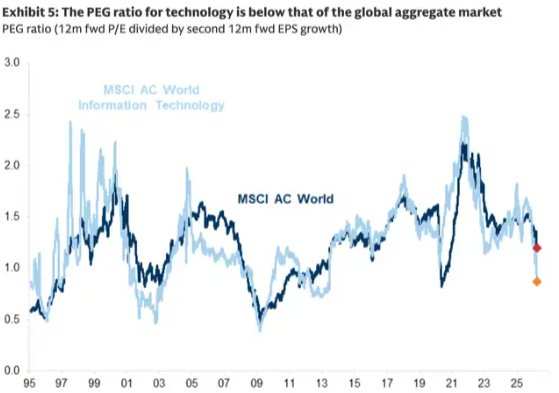

2. Secondly, the forward PEG ratio of the global technology industry is now significantly below the overall global market level. The PEG ratio (Price/Earnings to Growth ratio) measures the expected earnings for the next 12 months against the anticipated earnings growth rate for the following 12 months. The forward PEG ratio of the technology sector has fallen below 1, indicating that the sector is undervalued.

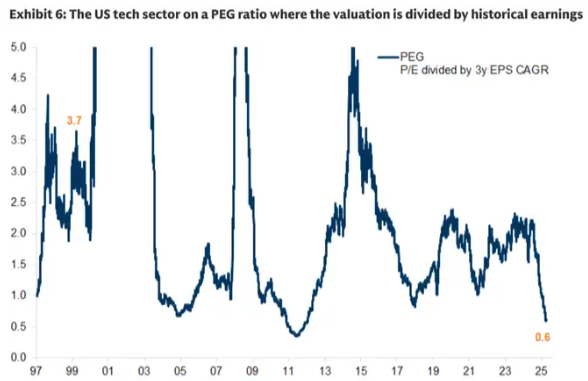

3. The rolling PEG ratio of technology stocks also remains in undervalued territory. This metric compares the past 12 months of earnings with the earnings growth rate over the past three years, removing uncertain elements. The bank stated: ‘The collapse of the technology stock ‘retrospective’ PEG suggests significant future earnings declines, which have already dropped to trough levels after the tech bubble burst between 2003-05.’

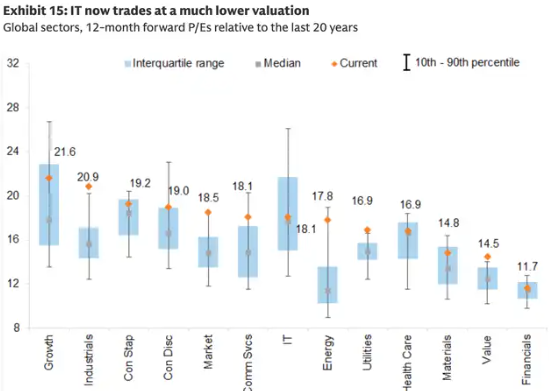

4. The forward price-to-earnings ratios of global technology and software stocks relative to other sectors worldwide are also at their lowest levels since at least 2019.

5. By the same valuation metrics, global technology stocks are currently trading nearly in line with their 20-year median. Only the financial sector is trading close to its historical levels, while all other sectors are valued above their historical averages.

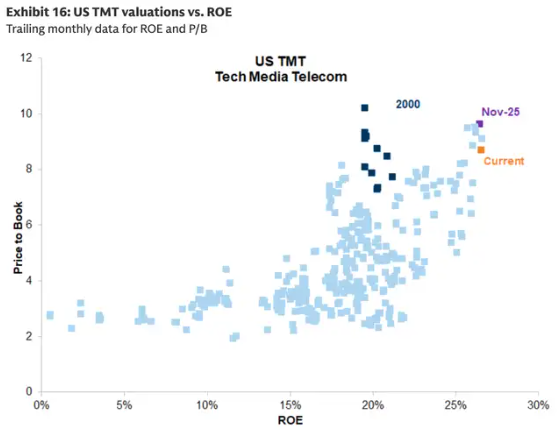

6. Furthermore, although US Technology, Media, and Telecommunications (TMT) stocks exhibit a relatively high Price-to-Book (PB) ratio, their Return on Equity (ROE) is also high, suggesting they remain historically reasonable and in line with trends. ROE refers to the ratio of company profits to its market value. Goldman Sachs stated that this should alleviate concerns about excessive spending on AI infrastructure. In contrast, during the peak of the internet bubble, ROE did not align with PB.

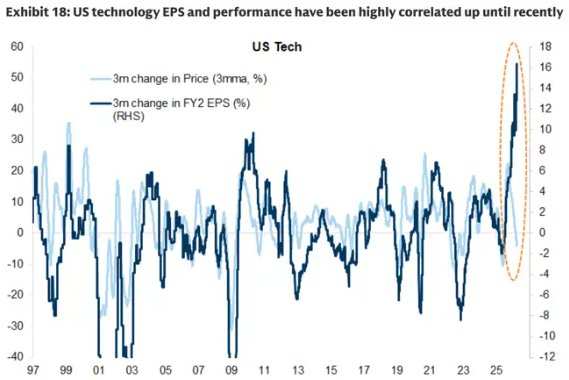

7. Finally, despite the recent sell-off, the net percentage of positive revisions in analysts’ earnings forecasts for technology stocks in 2026 and 2027 still exceeds that of all other industries.

Goldman Sachs is not the only Wall Street investment bank that believes the U.S. technology sector presents an attractive buying opportunity on dips. Wells Fargo & Co also considers the valuations of information technology stocks to have reached an appealing level for investors. The Wells Fargo Investment Institute has upgraded its rating for the sector from ‘neutral’ to ‘favorable,’ citing the sector’s underperformance compared to the S&P 500 Index and the robust growth prospects supported by the widespread adoption of artificial intelligence.

The company’s global investment strategy team stated that despite concerns over valuation, capital expenditure, and the disruptive impact of artificial intelligence, the fundamentals of the information technology sector remain strong. They cited double-digit earnings growth in the fourth quarter as an example. The strategists also noted that since the outbreak of the US-Iran war, the information technology sector has outperformed the S&P 500 Index, highlighting the industry’s long-term growth and quality characteristics.

Bill Baruch, head of investment at the asset management giant Blue Line Capital, has also pointed out that the U.S. software industry holds tremendous opportunities following the recent market turbulence. He believes that software giants such as ServiceNow (NOW.US), Oracle (ORCL.US), and Microsoft (MSFT.US), which have been heavily impacted since February by the pessimistic narrative of ‘AI disrupting everything,’ are now attractive investment targets at current price levels. During an interview, Baruch expressed a bullish outlook on the broader U.S. equity market while specifically highlighting technology stocks that were unfairly punished during the recent sell-off.

In addition, seasoned strategist Ed Yardeni’s latest comments this week echoed the aforementioned views. He believes that after retreating from last year’s record highs, U.S. technology stocks have returned to levels that are appealing for investors willing to make long-term investments.