Vertex Pharmaceuticals Stock: Q1 2026 Revenue Hits $2.99B With Full-Year Guidance Intact

Key Stats

- Current Price: $424 (May 5, 2026)

- Q1 2026 Revenue: $2.99B, up 8% YoY

- Q1 2026 Non-GAAP EPS: $4.47, up 10% YoY

- 2026 Revenue Guidance: $12.95B to $13.1B (8% to 9% growth)

- TIKR Model Price Target: $803 (mid case)

- Implied Upside: ~89%

Vertex Pharmaceuticals Stock Posts 8% Revenue Growth in Q1 2026, Reiterates Full-Year Outlook

Vertex Pharmaceuticals stock (VRTX) reported Q1 2026 total product revenue of $2.99B, up 8% year-over-year, with non-GAAP EPS of $4.47 compared to $4.06 in Q1 2025.

CF remained the volume anchor, with global CF revenue growing 6% year-over-year, split between 5% U.S. growth and 8% international growth, according to Chief Commercial Officer Duncan McKechnie on the Q1 2026 earnings call.

ALYFTREK crossed $1 billion in cumulative global revenue since its U.S. approval in December 2024.

New disease areas contributed roughly 25% of total year-over-year revenue growth for the quarter, with CASGEVY delivering $43M and JOURNAVX generating $29M, according to CFO Charlie Wagner on the Q1 2026 earnings call.

JOURNAVX filled more than 350,000 prescriptions in Q1, compared to roughly 550,000 for all of 2025, with payer coverage now reaching 240 million lives.

Q1 revenue of $29M for JOURNAVX reflected normal inventory destocking between Q4 2025 and Q1 2026 and a seasonal reduction in elective surgeries, according to McKechnie on the Q1 2026 earnings call.

Management reiterated 2026 total revenue guidance of $12.95B to $13.1B, representing 8% to 9% growth, with non-CF product revenue expected to exceed $500M for the full year.

Non-GAAP SG&A expenses increased 30% year-over-year, driven by commercial investments with roughly 40% attributable to JOURNAVX and approximately one-third to renal launch preparation, according to Wagner on the Q1 2026 earnings call.

Vertex repurchased more than 741,000 shares for approximately $344M in Q1, ending the quarter with $13B in cash and investments.

The company also filed a BLA for povetacicept (Pove) in IgAN following a Phase III interim analysis showing a 52% reduction in proteinuria from baseline, and disclosed that the VX-522 mRNA therapy program has been discontinued due to unresolved lung inflammation tolerability issues.

Vertex Pharmaceuticals Stock: Financials

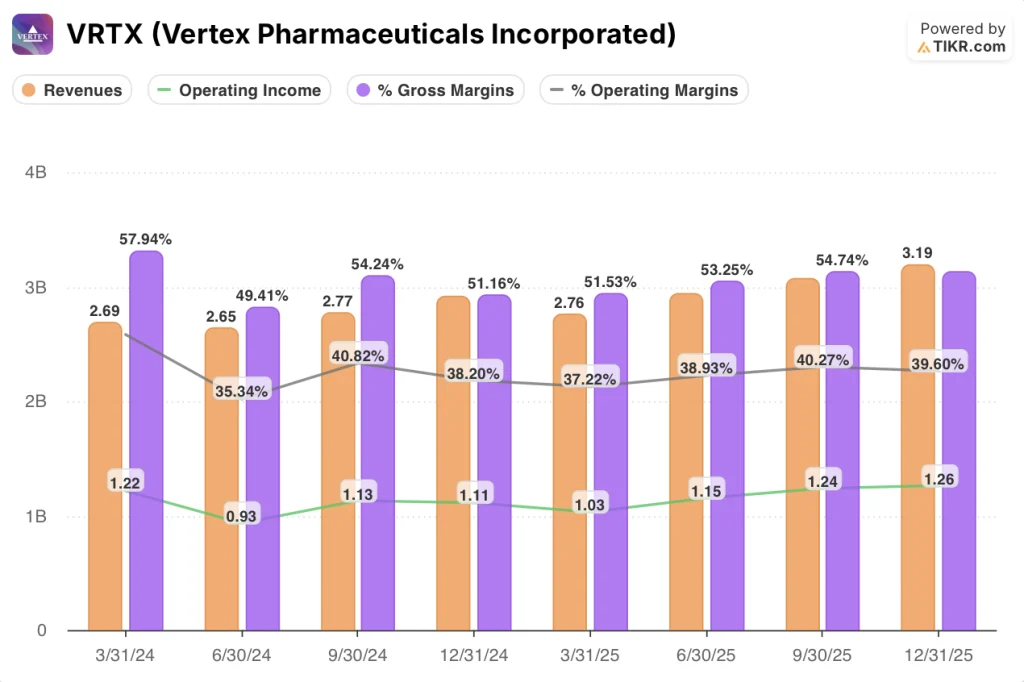

The Q1 2026 income statement tells a margin expansion story, with operating income growing faster than revenue as Vertex absorbs early commercial investment across three product launches.

Revenue trended from $2.76B in Q1 2025 up to $2.96B in Q2 2025, $3.08B in Q3 2025, and $3.19B in Q4 2025 before pulling back to $2.99B in Q1 2026, a sequential step-down that reflects the typical Q4-to-Q1 seasonality visible across prior years.

Gross margin was 51.5% in Q1 2025, recovered to 53% in Q2 2025, 55% in Q3 2025, and 55% in Q4 2025, though the Q1 2026 figure is not directly visible in the screenshot; management guided full-year gross margin to remain just under 86% on a non-GAAP basis, reflecting ongoing investment in manufacturing and the growing non-CF product mix.

Operating income reached $1.31B in Q1 2026, up from $1.18B in Q1 2025, according to Wagner on the Q1 2026 earnings call.

Operating margin tracked from 37% in Q1 2025 to 39% in Q2 2025, 40% in Q3 2025, and 40% in Q4 2025 on the income statement screenshot, establishing a clear step-up from the 45% peak seen in Q1 2024 before the JOURNAVX and CASGEVY commercial buildout absorbed SG&A.

Non-GAAP R&D expenses declined 2% year-over-year, partly due to the timing and mix of clinical trial expenses, with certain Pove manufacturing costs reclassified from R&D to cost of sales following the positive Phase III interim analysis, according to Wagner on the Q1 2026 earnings call.

Non-GAAP net income came in at $1.1B, up $93M year-over-year, driven by revenue growth partially offset by higher operating and tax expenses.

What Does the Valuation Model Say?

TIKR’s model prices Vertex Pharmaceuticals stock at $803 in the mid case, implying ~89% upside from the current price of $424.

The model assumes a revenue CAGR of 10.6% and a net income margin of 43.2% through the 2025–2035 forecast period, both grounded in Vertex’s demonstrated ability to compound revenue while maintaining disciplined commercial spending.

Q1’s on-track financial delivery and reiterated guidance do not change the model assumptions but remove a meaningful source of near-term uncertainty: this is a company executing precisely in line with its stated plan.

For Vertex Pharmaceuticals stock, the investment case is stronger after this report, not because of a dramatic upside surprise, but because execution consistency across three simultaneous launches is exactly the confirmation the model depends on.

VRTX stock trades at a steep discount to TIKR’s fair value estimate, but the gap closes only if the non-CF portfolio scales on the timeline management has outlined.

The weight of the thesis now rests on Pove and JOURNAVX proving out as durable revenue contributors.

What Has to Go Right

- JOURNAVX triples its 2025 prescription count in 2026 as targeted, with gross-to-net normalization through H2 2026 accelerating revenue growth faster than script volume

- Pove secures FDA approval in IgAN and achieves rapid payer access in a market where 70% of patients carry commercial coverage, as outlined by McKechnie on the Q1 2026 earnings call

- CASGEVY’s full-year contribution meaningfully exceeds Q1’s $43M run rate as more of the 500-plus patients who have initiated treatment move through to infusion

- The $500M-plus non-CF revenue target for 2026 is met, establishing a credible floor for the renal franchise build-out that begins with Pove

What Could Still Go Wrong

- JOURNAVX revenue of $29M in Q1 2026 remains well below what’s needed to hit management’s full-year ramp, and gross-to-net normalization depends on securing the remaining Medicare Part D plans and employer formularies on schedule

- CASGEVY’s quarter-to-quarter revenue variability is structural: patients choose infusion timing, making near-term revenue difficult to model and vulnerable to Q-to-Q misses

- SG&A growing 30% year-over-year signals that the commercial infrastructure for Pove’s launch is being built now, ahead of revenue; if the FDA review timeline slips from the BLA filed in Q1 2026, that investment carries without return

- The discontinuation of VX-522 removes the only program targeting the remaining 5% of CF patients who cannot benefit from modulators, narrowing the long-term CF growth ceiling

Should You Invest in Vertex Pharmaceuticals Incorporated?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Vertex Pharmaceuticals stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Vertex Pharmaceuticals Incorporated alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VRTX stock on TIKR for Free →

Is Up 6.0% After Q1 Profit Surge Signals Improved Operational Efficiency")

Is About To Go Ex-Dividend, And It Pays A 0.8% Yield")