How Bond Funds Fared in Q2 2026

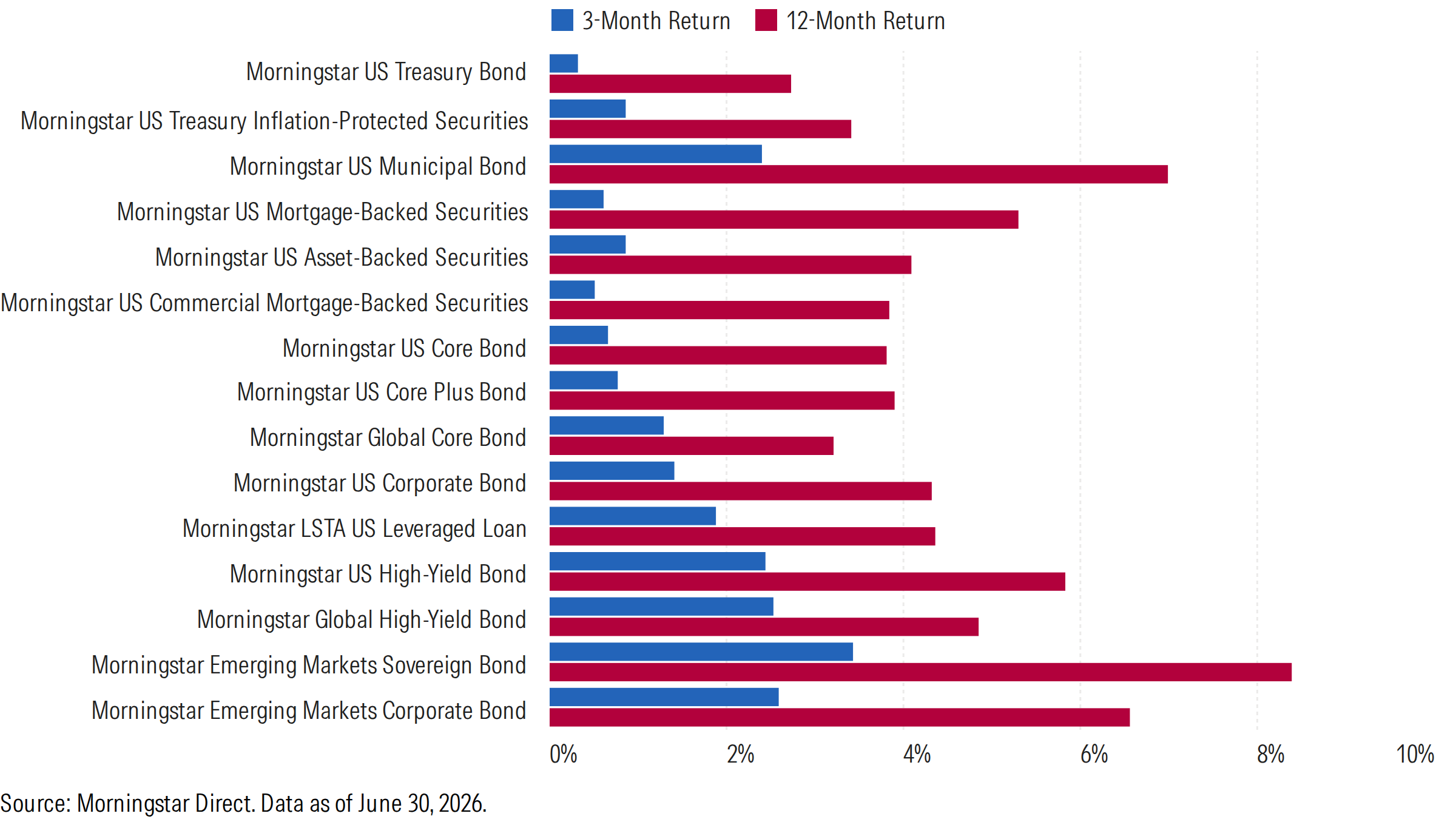

After a turbulent first quarter marked by the onset of the Iran war, the bond market found some footing in 2026’s second quarter. The Morningstar US Core Bond Index, a proxy for the US-dollar-denominated investment-grade bond market, eked out a 0.7% gain in what proved to be another challenging quarter for fixed-income investors.

Persistent interest rate volatility and inflation concerns pivoted market expectations from pricing in multiple interest rate cuts in late 2026 to pricing in the probability of further tightening and federal funds rate hikes. Treasury yields increased, with the short end of the curve increasing more than the long end, causing the yield curve to flatten. Meanwhile, credit spreads remained at historically tight levels on account of continued economic stability and strong corporate fundamentals.

Against that backdrop, high-quality and long-duration bonds, like US Treasuries and agency mortgage-backed securities, failed to keep pace with credit-sensitive sectors such as emerging-market debt, municipal bonds, and high-yield credit during the quarter.

Below, we dig deeper into a few fixed-income categories and highlight how some of our favorite bond managers fared during the quarter.

Emerging-Market Debt Recovered

After suffering in 2026’s first quarter from the strengthening US dollar, emerging-market debt rebounded in the second quarter thanks to strong fundamentals and favorable inflation dynamics. The Morningstar Emerging Market Bond Index’s 3.1% gain beat most major Morningstar fixed-income indexes.

Transamerica Emerging Markets Debt IAADX, which earns a Morningstar Medalist Rating of Silver, climbed 6.1%, shattering the typical emerging-market debt Morningstar Category peer’s 4.5% return, thanks to its bold approach and elevated foreign currency exposure compared with its average rival. Not far behind, Bronze-rated TCW Emerging Markets Income TGEIX gained 6.0%, owing to the strategy’s flexibility to hold up to 35% in corporate bonds; this adds risk but boosts performance in risk-on periods.

Munis Stood Strong

Significant investor demand for muni bonds supported strong performance relative to taxable bonds. The muni market, as measured by the Morningstar US Municipal Index, returned 2.4% and beat its taxable counterpart, the Morningstar US Corporate Index, by 99 basis points. Muni funds with higher interest rate and credit risks reaped the benefits over conservative peers, as longer-dated muni bonds and lower-quality credits outperformed during the quarter.

As such, Gold-rated Baird Core Intermediate Municipal Bond’s BMNIX relatively conservative approach trailed its more aggressive peers during the quarter; the fund’s 1.7% lagged more than 80% of its muni national intermediate category. The team sensibly anchors the portfolio’s duration to its benchmark and parks the bulk of assets in high-quality AA muni bonds. The strategy’s long-term track record remains stellar, though.

Bronze-rated Goldman Sachs Dynamic Municipal Income GSMTX, meanwhile, gained 2.4% and beat more than 75% of rivals, thanks to its flexibility to buy more below-investment-grade debt than its typical peers.

Credit Strategies Continued to Deliver

Strong corporate fundamentals and a healthy economy continued to provide tailwinds for credit-sensitive assets, such as bank loans and high-yield bonds. Bank loans, as measured by the Morningstar LSTA US Leveraged Loan Index, snapped their 14th consecutive quarter of positive returns in 2026’s first quarter but rebounded and rose 1.9% in the second quarter.

High-yield bonds took the spotlight, though, and the Morningstar US High Yield Bond Index returned 2.4%. Some managers took advantage of the favorable environment better than others. For example, Silver-rated Fidelity Capital & Income FAGIX soared 7.6% with the help of the portfolio’s 20% equity stake. While it’s an odd fit in the high-yield bond category, it still beat its average peer by over 500 basis points for the quarter.