Weekend Reading | A trillion-dollar IPO myth is set to unfold in 2026, but the ‘small unicorns’ have already collapsed.

Source: Tencent Technology

Author: Xiaojing

The year 2025 just passed witnessed an unprecedented ‘technological paradox show’ in the capital markets.

On one side are newly-listed tech giants whose stock prices have plummeted like kites with severed strings. Once high-flying star companies have seen their market values evaporate by tens of billions of dollars within months, with some experiencing devastating declines exceeding 50%. The market’s ‘chill’ has spread rapidly, causing a wave of star companies planning to go public to postpone their IPOs out of fear.

On the other side, the ‘ardent hopes’ of capital are burning fiercely.

On the other side, the ‘ardent hopes’ of capital are burning fiercely.

A brand-new ‘trillion-dollar club’ is gathering outside the gates of the capital markets. From Elon Musk’s aerospace empire SpaceX, to Sam Altman’s OpenAI, to the rising giant Anthropic, these companies are preparing for historically unprecedented mega-IPOs, with valuations reaching hundreds of billions or even trillions of dollars.

Cold and heat, collapse and jubilation, retreat and advance.

This trial by ice and fire—does it mark the beginning of the market’s return to rationality, or is it the prelude to capital’s extreme divergence? With the clock striking for 2026, will the logic behind this ‘dual reality’ persist, and has the future flow of capital already shifted?

01, 2025 Tech IPO Review: The Chill of Breakdowns and Plunges

In 2025, although there were signs of recovery in the number of tech company listings (around 23, significantly more than in 2024), overall performance was bleak: over two-thirds of companies saw their share prices fall below the issue price, with a median decline of 9%, significantly underperforming the nearly 18% rise in$S&P 500 Index (.SPX.US)$。

However, after a brief period of fervor, tech stocks returned to a cold, harsh reality.

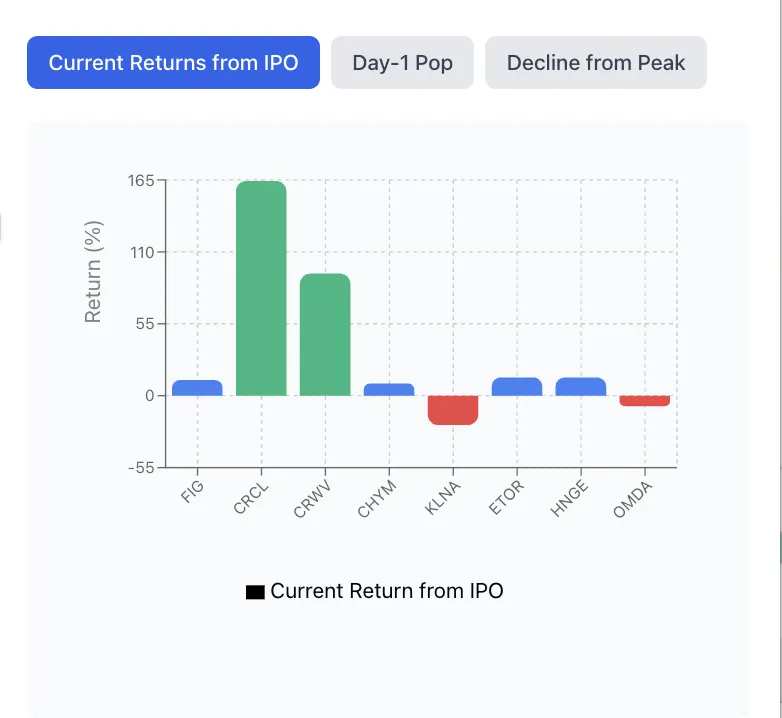

Among numerous star startups,$Circle (CRCL.US)$(Stablecoin issuer) becomes one of the few survivors: benefiting from favorable policies, its stock surged on the first day of listing and, despite a subsequent pullback, remains solidly in positive territory, standing as the only firm winner.

By contrast, other unicorns have underperformed. Figma initially sparked widespread discussion at its IPO but has seen its stock plummet significantly from its peak due to intensified AI competition and slowing growth. $Klarna Group (KLAR.US)$ (Installment payment), $Stubhub Holdings (STUB.US)$ (Ticketing platform), and $Navan (NAVN.US)$ (Business travel software) collectively lost billions in market value post-IPO, exposing the secondary market’s aversion to the ‘growth-at-the-cost-of-losses’ model.

The worst performer is cryptocurrency exchange $Gemini Space Station (GEMI.US)$ . Hit by both financial losses and regulatory pressures, its stock price has been halved compared to the issue price, plunging by 58%.

On the other hand, capital is exercising unprecedented patience in betting on ‘scarcity.’ While small- and mid-cap tech stocks struggle due to insufficient liquidity and extended trust cycles, the entry of supergiants like SpaceX, OpenAI, and Anthropic could single-handedly reignite market enthusiasm.

This extreme polarization indicates that the secondary market’s preferences have shifted: investors are no longer buying into ‘growth stories,’ but instead are fiercely competing for positions in a select few ‘must-have’ top-tier sectors.

By contrast, small and medium-sized publicly listed technology companies with an average market capitalization of approximately USD 8.3 billion face challenges such as higher valuation thresholds, insufficient liquidity, and prolonged trust-building cycles, making it difficult to attract sustained attention from index funds and retail investors.

Behind this situation lies a serious ‘trust gap.’ On the one hand, company founders and venture capital firms are reluctant to lower valuations for IPOs; on the other hand, public investors, under the shadow of the AI bubble, have become extremely sensitive about companies’ profitability prospects and internal cash-outs. Coupled with banks attributing pricing difficulties to environmental volatility, the multi-party game has reached a deadlock, ultimately resulting in an awkward situation where no party benefits.

This chill is rapidly spreading to companies planning to go public in 2026. For example, Perk (formerly TravelPerk), a corporate travel software company, has postponed its IPO plans to 2027. If market sentiment does not improve significantly by 2026, there may be a large number of potential listed companies ‘waiting in line but too afraid to ring the bell.’

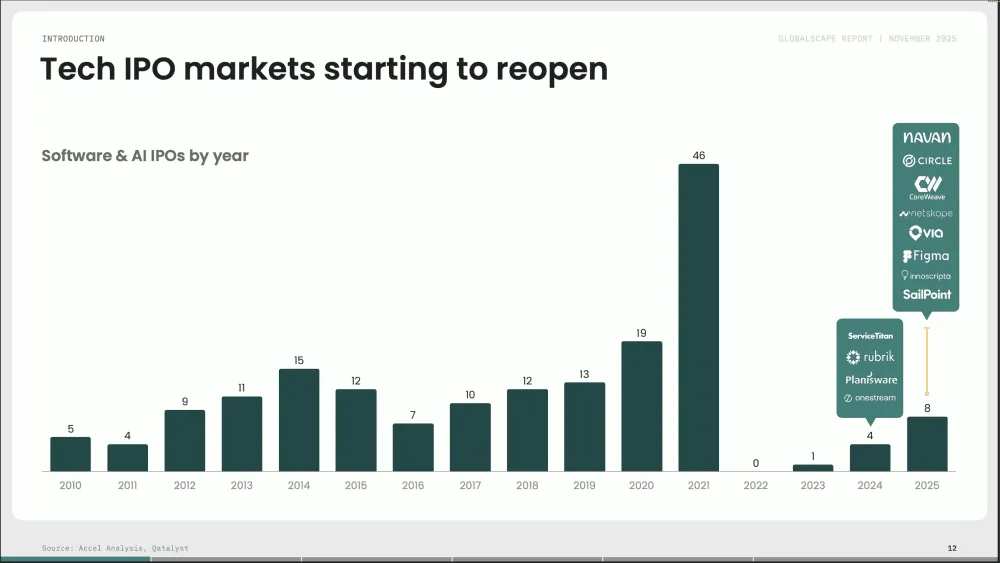

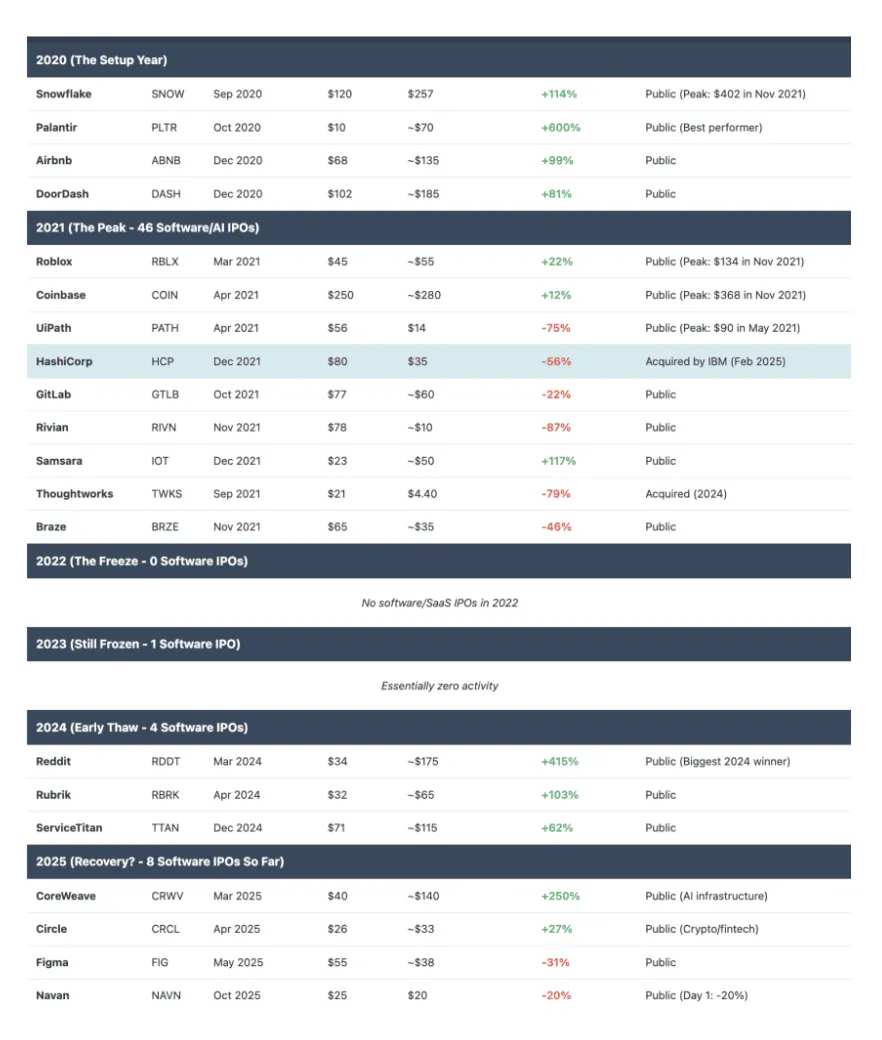

From a historical perspective, the recovery in 2025 is still far from reaching prosperous levels. Data from Accel Analysis and Qatalyst show that the number of IPOs in the software and AI sectors peaked between 2019 and 2021, with 13, 19, and 46 listings respectively. This was followed by a collapse during 2022-2023, with zero and one listing respectively, and then a recovery phase in 2024-2025 (4 and 8 listings).

However, the number of IPOs in the software and AI sectors in 2025 is only about half of the peak in 2021, falling below the ‘normal’ baseline of 9-10 per year between 2010 and 2018. This indicates that the tech IPO market still has a long way to go before returning to true normalization.

Failure Case Analysis: The Collision of High Valuations and Market Realities

Navan’s experience is quite typical.

This corporate travel management platform went public in October 2025, with its valuation trajectory resembling a parabola: peaking at USD 9.2 billion during Series G financing in 2022, shrinking to USD 6.2 billion at IPO pricing (USD 25 per share), and closing below the issue price on its first trading day, with the stock price dropping to USD 20 and the market capitalization left at only USD 4.7 billion.

Ironically, Navan is not a shell company. It boasts an annual run-rate revenue of $613 million (a 32% increase) and over 10,000 corporate clients, with a solid business scale and genuine cash-generating capabilities. However, market pricing logic has undergone a dramatic shift: a similar company could easily achieve a price-to-sales ratio (P/S) of 15-25 times in 2021, but in the 2025 environment, even at a valuation of just 10 times, the market still deems it “too expensive.”

The core issue behind this cold reception lies in the breakdown of the ‘Rule of 40.’ Although Navan exhibits 30% revenue growth, its net profit margin of approximately -30% offsets this, resulting in a score close to zero. According to this golden criterion for measuring the health of software companies, only when the sum of growth rate and profit margin reaches or exceeds 40% is a company considered to have achieved a balance between ‘expansion’ and ‘efficiency.’

$Figma Inc (FIG.US)$ serves as a microcosm of the extreme volatility in tech stocks. Despite surging 2.5 times after its IPO in July, the stock plummeted by 60% from its peak following the release of an earnings report indicating slowing guidance. This volatility stems primarily from two factors: first, structural imbalances—only 8% of shares were tradable at the time of listing, creating artificial scarcity, while the release of large blocks of restricted shares in September triggered panic selling; second, excessive valuation—its price-to-sales ratio of 31 times was $Adobe (ADBE.US)$ more than four times higher, making its premium appear fragile in the face of slowing growth.

The chill in the market is spreading comprehensively. From ticketing platform StubHub (down 42%) to commercial space company Firefly (down 36%), from transportation software Via (down 28%) to fintech Klarna (down 22%), companies characterized by ‘high valuations and low profits’ are collectively facing brutal corrections from the market.

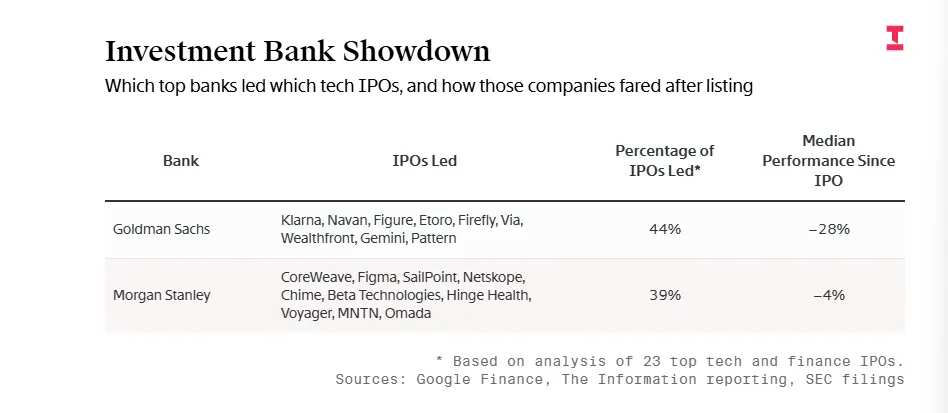

The Dilemma of Investment Banks: The Diminished Prestige of Goldman Sachs and Morgan Stanley—Who Will Pay for the High Valuation Bubble?

The subpar performance of IPOs in 2025 has placed investment banks Goldman Sachs and Morgan Stanley, which have led the majority of tech stock listings, in an awkward position.

IPO projects led by Goldman Sachs (such as Via and Firefly) have seen a median decline of approximately 28%, underperforming the overall market. Morgan Stanley was responsible for Figma and $CoreWeave (CRWV.US)$For such deals, the median drop in IPO share prices underwritten was about 4%, better than the overall median, but each company has already fallen significantly from its peak.

Analysts noted that part of the poor performance is due to factors beyond the banks’ control. Public investors believe that many companies attempting to go public now are not outstanding, while some of the strongest firms remain private.

Samantha Liu, Chief Investment Officer for Small and Mid-Cap Growth Stocks at AllianceBernstein, pointed out that she had tried to tell bankers working on IPOs for companies like Navan to keep pricing reasonable, especially if they do not expect significant retail interest. “Expectations have completely spiraled out of control,” she said.

02, The Rise of Giants: Record-Breaking IPO Preparations by SpaceX and OpenAI Heat Up

While numerous tech startups face a ‘cold spell’ in the public markets, a contrasting wave of enthusiasm is emerging from another corner. In sharp contrast to companies that see their stock prices plummet immediately after listing, a few super tech giants with established dominance and perceived as ‘must-haves’ are gaining attention.

SpaceX: Targeting the Largest IPO in History

According to insiders, SpaceX is actively advancing its IPO plans, aiming to raise over $300 billion at a valuation targeting $1.5 trillion. This scale approaches the record set by Saudi Aramco in 2019.

In terms of scale, if SpaceX sells 5% of its shares at a $1.5 trillion valuation, the $400 billion offering will surpass Saudi Aramco’s $290 billion record, making it the largest IPO in history.

Unlike Saudi Aramco’s extremely low free float, if SpaceX successfully completes an offering of this magnitude, it will fundamentally reshape the global hard tech investment landscape. Management currently favors a listing in the mid-to-late 2026 period, but may delay it to 2027 depending on market volatility.

SpaceX’s confidence in accelerating its IPO stems from explosive business growth: Starlink has become a core revenue pillar, and its ‘direct-to-phone’ service has significantly expanded market boundaries. Meanwhile, advancements in Starship for lunar and Mars exploration have provided immense room for imagination.

Financial data indicates that the company’s revenue is projected to reach USD 15 billion in 2025 and is expected to surge to between USD 22 billion and USD 24 billion in 2026. In addition to its core aerospace operations, the funds raised through the IPO will also be invested in new fields led by Elon Musk, including the development of space-based data centers and related chips.

Elon Musk recently confirmed via social platform X that SpaceX has achieved years of positive cash flow and provides liquidity to employees and investors through regular buybacks. He emphasized that the rise in valuation is an inevitable result of technological breakthroughs in the Starship and Starlink projects. Currently, SpaceX boasts an impressive shareholder lineup, including top-tier institutions such as Founders Fund, Fidelity Investments, and Google.

OpenAI: A Trillion-Dollar IPO Reshapes AI Capital Landscape

It has been reported that OpenAI is also preparing for a major IPO, aiming to raise at least USD 60 billion with a valuation reaching USD 1 trillion. According to insiders, OpenAI is considering submitting its IPO application to securities regulators as early as the second half of 2026.

Meanwhile, OpenAI is also in negotiations for a funding round of up to USD 100 billion, which could potentially increase its valuation to USD 830 billion.

The company aims to complete this round of financing by the end of the first quarter next year and may invite sovereign wealth funds to participate in the investment.

This financing effort comes as OpenAI, committed to maintaining its leading position in the AI technology race, has pledged trillions of dollars in investments and formed multiple global partnerships.

The core logic behind this financing points directly to computational supremacy, as OpenAI needs to invest over USD 38 billion in building data centers and server clusters in the coming years. Potential investors fall into four main groups: tech giants (seeking business alignment), sovereign wealth funds (Middle Eastern and Singaporean funds demanding technology implementation and industrial returns), Wall Street investment firms (JPMorgan and others securing pre-IPO positions), and innovative financing models (government energy collaborations, specialized debt instruments, etc.).$Amazon (AMZN.US)$、$NVIDIA (NVDA.US)$、$Microsoft (MSFT.US)$and $Apple (AAPL.US)$

Particularly noteworthy is the deep integration of geopolitical factors into financing negotiations: multiple rounds of investment by the UAE’s MGX Fund, Saudi Arabia’s potential requirement for data center localization, and indirect involvement by the U.S. government through infrastructure cooperation have elevated this financing beyond commercial scope, making it a microcosm of great power technological competition.

If the financing succeeds, OpenAI will set a historical record by surpassing the annual technology budgets of most countries in terms of single-company funding scale.

In addition to SpaceX and OpenAI, AI startups like Anthropic, valued at over 300 billion US dollars, have joined the “hot” category. The rise of these super giants contrasts sharply with the cold reception of most tech IPOs expected in 2025.

Overall, 2026 may witness an IPO wave of highly valued unicorns, with potential candidates including:

Super giants: SpaceX, OpenAI, Anthropic. Their listings will redefine the scale of IPO markets.

AI and infrastructure: Companies in the AI sector seeking capital expansion, such as chipmaker Cerebras, and data center providers Lambda, Crusoe, and Nscale.

Fintech and software: Motive, supported by Index Ventures, which sells safety technology to truck drivers; PayPay, a Japanese fintech company backed by SoftBank; and other medium-sized tech companies.

Companies that have postponed or are waiting: Such as Perk, which has delayed its IPO plans until 2027, and a large group of ‘candidates waiting in line but hesitant to knock.’

Jeff Clow, senior managing partner at Norwest Venture Partners, said: ‘There is a group of potential IPOs waiting to go public, but if market acceptance of IPOs does not improve by 2026, no one will rush to act.’

Notably, B2B industry leaders like Stripe and Ramp, which generate annual recurring revenue exceeding 1 billion US dollars, are currently opting for large-scale private financings or equity acquisition offers rather than going public.

Payment giant Stripe recently completed a tender offer for equity, valuing the company at $91.5 billion. The State Street Private Equity Index now represents a valuation exceeding $5.7 trillion, more than five times the $110 billion in committed capital when it was launched in 2007. The abundance of private capital has alleviated the pressure on companies to endure quarterly earnings call scrutiny and the increased regulatory burdens associated with going public.

Tim Levene, CEO of Augmentum Fintech, the largest fintech fund in Europe, believes that “many of our portfolio companies are likely to exit through mergers and acquisitions rather than opting for an IPO.”

Jeff Crowe, senior managing partner at Norwest Venture Partners, also noted that his venture capital firm is seeing a ‘more favorable M&A environment,’ with three companies from its portfolio recently acquired by major technology firms.

03: The Rules of the Game Have Changed for Tech Stock IPOs

Looking ahead to 2026, the global IPO market is in a critical transition phase moving from a ‘valuation winter’ toward ‘cautious optimism.’ Improvements in macroeconomic indicators, more predictable monetary policies, and the commercialization dividends of AI technology are collectively catalyzing a recovery in market sentiment.

A diversified global pipeline of companies preparing for listing is taking shape. If market volatility can be effectively managed, the momentum accumulated for listings in 2025 is expected to result in a concentrated surge of IPO activity in 2026.

However, the path to recovery is not without obstacles, as the market faces significant entry challenges:

-

Severe IPO backlog: Hundreds of ‘veteran’ unicorns originally scheduled to go public in 2022-2023 are still in the queue. These companies are more mature in size and have a more urgent need for capital.

-

Significantly higher entry thresholds: Market performance during 2024-2025 has demonstrated that buyers are no longer accepting ‘marginal cases.’ Ideal candidates now need to exhibit approximately $500 million in annual recurring revenue (ARR), a growth rate of 50%, and strong unit economics.

-

Complex macro-level dynamics: The pace of IPOs in 2026 will heavily depend on the stability of monetary policy, easing geopolitical tensions, and the robustness of labor markets.

The sharp volatility since 2025 essentially represents the painful correction of the market transitioning from irrational exuberance to value restoration. Except for a handful of top giants, the public market has virtually closed its doors to mediocre companies. Investors are no longer willing to pay for ‘expected growth,’ instead scrutinizing profitability and sustainability with unprecedented rigor.

For entrepreneurs, the rules of the game may have permanently changed, with profitability paths, strategic clarity, and unit economics now serving as essential prerequisites for survival.

Editor/Rice

Opens Retail Access To The SpaceX IPO As Bank Lending Improves")