An analysis of the five key drivers behind the rise in gold prices!

The last time the gold price surged by $1,000 took half a year; will this time be faster? Driven by five key factors, the bull market in gold continues its ‘brutal aesthetics’…

Recently, investor concerns have continued to escalate. Whether it is the decline in bond yields, high stock market valuations, or policy uncertainties surrounding Trump, all have led them to make the same choice: buying gold.

Gold seems to be reaching new milestones at an accelerating pace. Just three months after breaking through what once seemed an unattainable level of $4,000 per ounce, it has now reached the critical threshold of $5,000. By comparison, gold futures took half a year to move from surpassing $3,000 per ounce on March 14 last year to hitting the historic peak of $4,000 per ounce in October.

On Wednesday, gold futures rose by 1.5%, closing at a record high of $4,831.80 per ounce. Since the beginning of this month, the price of gold has surged by over $500, including a single-day spike of $171.20 on Tuesday, setting a new daily gain record. Behind this rally lies Trump’s tariff threat against Europe (later retracted) in pursuit of control over Greenland, as well as mounting concerns about the Federal Reserve’s independence.

Below are the five core factors driving the gold market higher:

“Currency Devaluation Trade”

Among the largest group of gold bulls are investors concerned about the trajectory of the U.S. dollar and other major currencies. They have been aggressively purchasing this precious metal, viewing it as a store of value that can withstand economic shocks.

Recently, a series of actions by Trump have further heightened investor caution. Earlier this month, he authorized military action against Venezuela to overthrow the Maduro regime; pressured Federal Reserve Chairman Powell via a Department of Justice investigation to cut interest rates; and threatened to impose additional tariffs on European allies if they did not cooperate with his plans regarding Greenland.

This strategy, known on Wall Street as the “currency devaluation trade,” is driven by investor fears that governments’ inability to curb inflation or reduce debt will lead to the erosion of the currencies underpinning the global financial system.

In early 2025, Trump’s intensively rolled-out tariff policies caused the U.S. dollar to post its worst first-half performance in 50 years, prompting investors to flock to the gold market. In August of the same year, despite inflation remaining above target levels, Powell signaled that the Federal Reserve would begin a rate-cutting cycle, following which gold prices continued their upward trajectory.

At the same time, the swelling debt levels and expansionary economic policies in Europe and Japan have also fueled the rise in gold prices. Traders’ concerns over a potential U.S.-Europe trade war resurfaced, while Tuesday’s sell-off in the Japanese bond market pushed long-term government bond yields in the country to historic extremes.

Analysts indicate that the stability of these market cornerstones, as well as the credibility of the institutions regulating these markets, may determine the future trajectory of gold.

Daniel Ghali, a strategist at TD Securities, told clients on Tuesday: ‘The rise in gold prices is fundamentally tied to market trust. At present, while cracks in trust have emerged, they have not completely collapsed. If they do collapse, the upward momentum in gold prices will persist for a longer period.’

Persistent decline in interest rates

The Federal Reserve’s interest rate cuts have lowered the yields on government bonds and cash, which is also a significant factor driving investors towards the gold market.

In 2022, in response to high inflation during the pandemic, the Federal Reserve initiated a rate hike cycle, making ultra-safe U.S. Treasuries an extremely attractive investment option. Before the upward trend in interest rates began at the start of 2022, money market funds (primarily invested in government bonds) had a total scale of approximately $5.1 trillion. By the end of last year, this figure had surged to $7.7 trillion.

Currently, the declining yields of government bonds and money market funds have reduced their attractiveness—should Trump’s demands be met and the Federal Reserve further lowers interest rates, these yields could decline even more.

The decline in yields on risk-free assets such as U.S. Treasuries has lowered the opportunity cost of holding gold. Although gold itself does not generate income, its potential for price appreciation is significantly greater.

Even a small shift of funds from the vast pool of money market funds into gold could exert substantial upward pressure on gold prices. According to calculations by Goldman Sachs analysts, exchange-traded funds (ETFs) holding gold account for only 0.17% of U.S. private financial portfolios. For every 0.01 percentage point increase in this proportion due to fund inflows (rather than appreciation in gold prices), the price of gold is expected to rise by 1.4%.

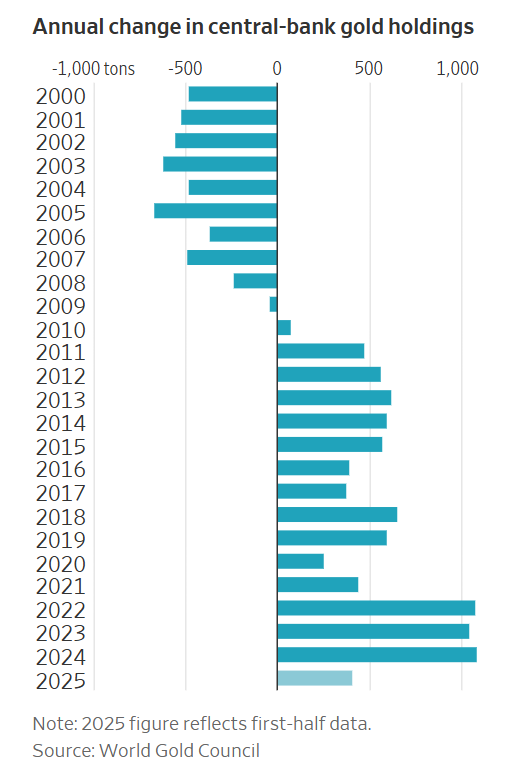

Central banks’ large-scale gold purchases

At the same time, ordinary investors must compete with a class of ‘deep-pocketed’ gold buyers—central banks, for whom the price of gold is typically not a primary consideration.

For many years, central banks around the world have been net sellers of gold. However, following the global financial crisis triggered by the U.S. subprime mortgage crisis in 2010, central banks reassessed their risks and became net buyers of gold. In 2022, central banks further accelerated their gold purchasing pace.

At that time, Western sanctions against Russia due to the Russia-Ukraine conflict prompted central banks of countries with strained relations with the West to significantly reduce their dollar assets and increase their gold reserves, as gold is not subject to external control.

Some other Western central banks are also increasing their gold reserves, such as the National Bank of Poland, which has always been an aggressive buyer of gold. On Tuesday, the bank approved another large gold purchase. These central banks aim to maintain the stability of their national currencies by increasing their holdings of gold, an asset free from sovereign debt risk.

Juan Carlos Artigas, Director of Research at the World Gold Council, stated: ‘Central banks’ purchases of gold are not solely based on its price performance but rather on the role it can play in foreign exchange reserves. Gold is an excellent tool for hedging risks and achieving reserve diversification.’

High stock market valuations

Similar to gold prices, stock market benchmark indices continue to set new historical highs, but their excessively high valuations have made investors increasingly uneasy.

The most commonly used metric for measuring stock valuations is the price-to-earnings (P/E) ratio. One widely used indicator is the cyclically adjusted price-to-earnings ratio (CAPE), which is based on analysts’ forecasts of corporate future profits. Data shows that over the past 100 years, U.S. stock valuations were higher than current levels only during one period—the eve of the dot-com bubble burst in 2000.

Technology stocks have once again become a major concern in the stock market. The movements of a few tech giants such as NVIDIA (NVDA), Tesla (TSLA), and Amazon (AMZN) are sufficient to influence the rise and fall of the S&P 500 Index, while the performance of the remaining over 490 constituent stocks is negligible.

For instance, on Tuesday, all seven major technology stocks referred to as the ‘Magnificent Seven’ closed lower, wiping out $683 billion in total market value and dragging the S&P 500 Index down by 2.1%. Meanwhile, the Russell 2000 Index, representing small-cap stocks, fell by only 1.2%, outperforming the S&P 500 Index for the twelfth consecutive trading day, a phenomenon that also reflects investors’ search for investment opportunities beyond large technology stocks.

Driven by the momentum of its upward trend

The likelihood of gold continuing to rise is extremely high, as the inherent long-term sustainability of its upward trend alone is sufficient to support this assessment. Data from Citi analysts shows that in years where gold futures recorded annual gains of at least 20% over the six-year period leading up to 2025, gold prices continued to rise in five of those subsequent years, with an average increase exceeding 15%.

This pattern remains valid in 2025: following a surge of 27% in 2024, gold prices skyrocketed by 65% in 2025.

, iSh")