Is It Too Late To Consider SSR Mining (TSX:SSRM) After Its Strong Share Price Run?

After Its Strong Share Price Run?")

- If you are wondering whether SSR Mining’s share price still offers value after a strong run, this article will walk through what the current market price might be implying about the business.

- The stock has been active, with returns of 14.4% over the past 7 days, 6.6% over 30 days, 19.3% year to date and 166.1% over the last year, as well as 90.3% over 3 years and 94.0% over 5 years.

- Recent news flow around SSR Mining has focused on its position within the precious metals sector and how investors are reacting to changing expectations for the gold price and miner profitability. These developments help frame why the recent share price moves have drawn more attention to whether the stock might now be pricing in higher expectations or different risk assumptions.

- On our checklist based valuation, SSR Mining currently scores 4 out of 6 for being potentially undervalued. Next, we will look at how traditional methods such as P/E ratios and discounted cash flow models compare, before finishing with a broader way to think about valuation that ties everything together.

Approach 1: SSR Mining Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business might be worth today by projecting its future cash flows and then discounting those back to a present value using a required rate of return.

For SSR Mining, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is $179.32 million. Analyst estimates and extrapolations in the source data point to free cash flow projections in the $600 million to $1.2 billion range over the next decade, with a specific projection of $853 million for 2028 and $1.22 billion for 2035, all in dollar terms.

When these projected cash flows are discounted back, the DCF model arrives at an estimated intrinsic value of $124.75 per share. Compared with the current share price, this implies the stock is 71.7% undervalued according to this method.

On this DCF view, the market price appears to be applying a materially lower value than the cash flow model suggests.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests SSR Mining is undervalued by 71.7%. Track this in your watchlist or portfolio, or discover 5 more high quality undervalued stocks.

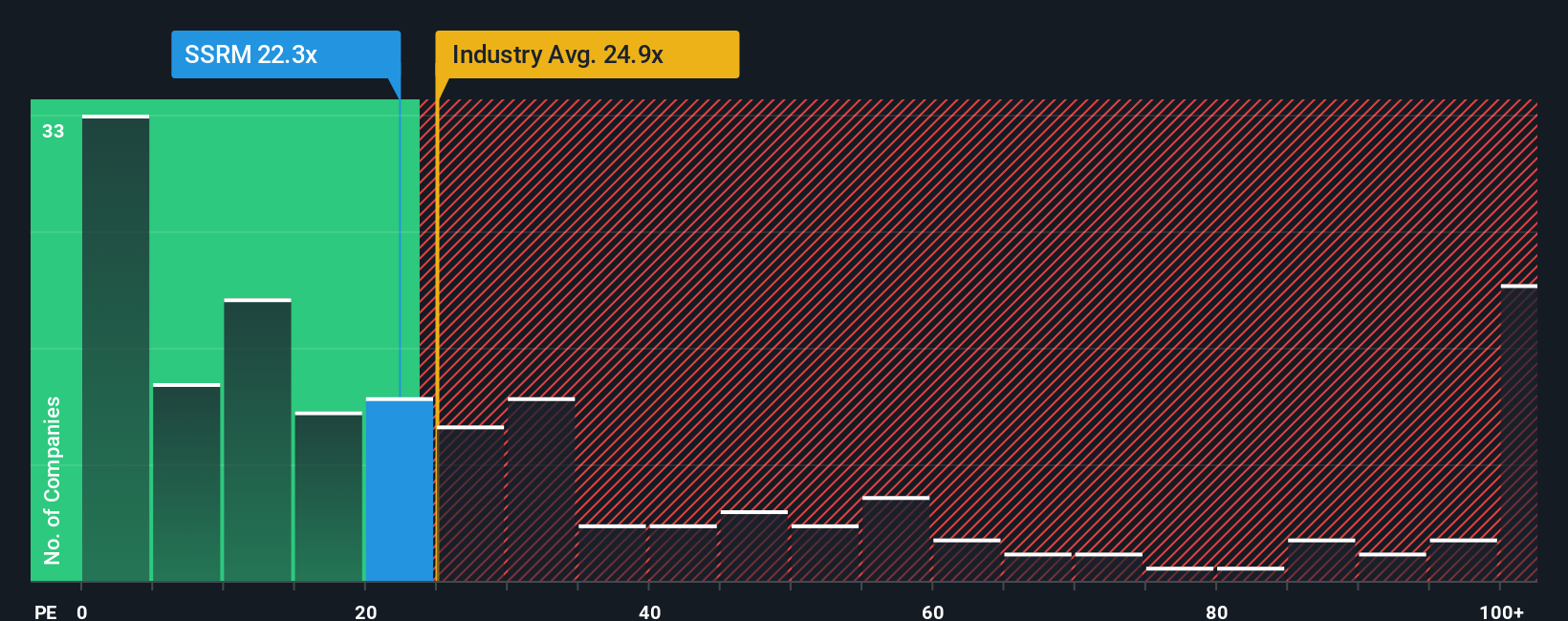

Approach 2: SSR Mining Price vs Earnings

For a profitable company like SSR Mining, the P/E ratio is a useful way to see what investors are currently willing to pay for each dollar of earnings. A higher or lower P/E often reflects how the market views the balance between earnings growth potential and the risks around those earnings.

Growth expectations and risk usually set the range of what looks like a normal or fair P/E ratio. Faster, more resilient earnings and lower perceived risk can justify a higher P/E, while more uncertainty or weaker profitability can point to a lower one.

SSR Mining currently trades on a P/E of 23.94x, which is similar to the Metals and Mining industry average of 23.82x and below the peer group average of 32.98x. Simply Wall St also calculates a proprietary Fair Ratio of 44.18x for SSR Mining, which is the P/E level suggested after considering factors such as earnings growth, industry, profit margin, market cap and company specific risks.

This Fair Ratio can be more informative than a simple comparison with peers or the industry, because it adjusts for SSR Mining’s own characteristics rather than assuming all miners deserve the same multiple. Since 44.18x is above the current 23.94x, this approach indicates that the shares appear undervalued on a P/E basis.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 3 top founder-led companies.

Upgrade Your Decision Making: Choose your SSR Mining Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St’s Community page you can use Narratives, which let you spell out your story for SSR Mining, link that story to specific assumptions for revenue, earnings and margins, and see a resulting fair value that you can compare with the current price. The platform updates those Narratives automatically when new news or earnings arrive. You can, for example, line up with a higher fair value view of about $53.40 per share or a lower one around $29.77 per share, then decide for yourself whether the gap between your chosen fair value and the live market price suggests SSR Mining looks closer to a buy, a hold, or a sell for your portfolio.

For SSR Mining, however, we will make it really easy for you with previews of two leading SSR Mining narratives:

Fair value in this bullish narrative: $53.40 per share

Implied discount to this fair value versus the last close of $35.29: about 34% undervalued

Revenue growth assumption in this bullish view: 40.53% per year

- Assumes higher gold prices, Hod Maden progress and strong execution at assets such as Cripple Creek & Victor support faster revenue and earnings growth than many expect.

- Builds in rising margins, with bullish analysts modeling earnings of US$745.7 million by about September 2028 and a future P/E of 6.6x, using a 7.1% discount rate.

- Flags key risks around Çöpler remediation costs, ESG and regulatory pressures, and higher operating costs, which could weaken this upside case if they escalate.

Fair value in this bearish narrative: $29.77 per share

Implied premium to this fair value versus the last close of $35.29: about 19% overvalued

Revenue growth assumption in this bearish view: 24.91% per year

- Assumes ongoing uncertainty around the Çöpler restart, rising reclamation costs and higher all in sustaining costs at operations such as Marigold and Seabee keep pressure on margins.

- Builds in slower growth and a lower future P/E of 4.98x, with modeled earnings of US$686.0 million by about September 2028 and a 7.0% discount rate.

- Accepts that solid liquidity, project work and mine life extensions could support the business, but still treats current market expectations as too high relative to these risks.

Do you think there’s more to the story for SSR Mining? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com