Capitalizing on AI Divergence, Navigating Volatility, and Hedging Tail Risks in Tech Stocks

To address volatility changes and headline risks, strategists are actively promoting a range of trading strategies, from conventional tail hedges to customized diversified baskets.

According to Zhitong Finance, as investors are concerned about missing out on further stock market gains while also worrying about the accumulation of geopolitical risks, they might find insights from derivatives strategists at major Wall Street banks. Trading strategies designed to address some of last year’s most significant market contradictions remain active, with the impact of President Trump’s erratic policies taking center stage. These uncertainties include his threats to the independence of the Federal Reserve, rhetoric about military action against Iran, claims to acquire Greenland, and interventions in electricity markets. Market consensus suggests that due to momentum trading being heavily affected by skepticism over excessive valuations—especially in artificial intelligence (AI)-related stocks—the coexistence of rising volatility and climbing stock prices will likely continue into 2026.

Tanvir Sandhu, Chief Global Derivatives Strategist at Bloomberg Intelligence, stated: ‘The momentum in AI and the U.S. government acting as a source of volatility create a favorable backdrop for markets. While right-tail risks are driven by earnings growth, cyclical recovery, and AI adoption, market fragility and high-risk policies amplify instability, potentially supporting a scenario where both the S&P 500 index and volatility rise simultaneously.’

To address volatility changes and headline risks, strategists are actively promoting a range of trading strategies, from conventional tail hedges to customized diversified baskets.

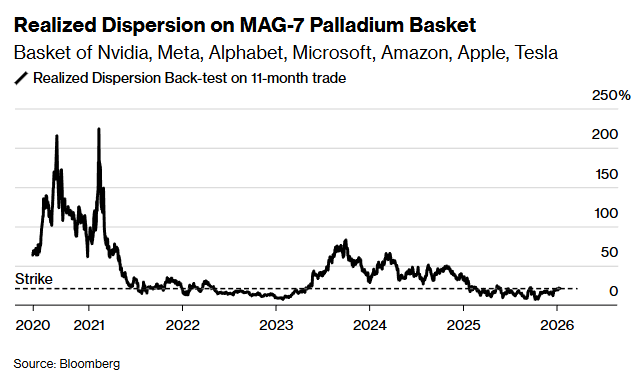

Palladium Structure of the ‘Magnificent Seven’

Large-cap technology stocks are still expected to lead market gains, but options on the ‘Magnificent Seven’ are not cheap. Barclays strategists believe that directly purchasing call options is not cost-effective; instead, the so-called Palladium structure offers an advantage—it bets on the dispersion of gains and losses within a basket of stocks rather than the basket’s overall performance.

This structure capitalizes on divergences among the top ten components of the S&P 500 index, providing higher AI upside exposure with lower volatility risk compared to the Nasdaq 100. Strategists recommend buying a Palladium trade expiring in December, with a strike set at 21% and a premium of 4%.

Realized Dispersion of the ‘Magnificent Seven’ Palladium Basket

Joseph Khouri, Head of Equity Derivatives Structuring for Europe, Middle East, and Africa at Bank of America, stated: ‘The Palladium structure is highly active among a broad client base, including hedge funds, pension funds, and asset managers. Baskets are typically constructed around investment themes such as cyclical versus defensive stocks, beneficiaries versus losers of interest rate cuts, and AI versus robotics.’

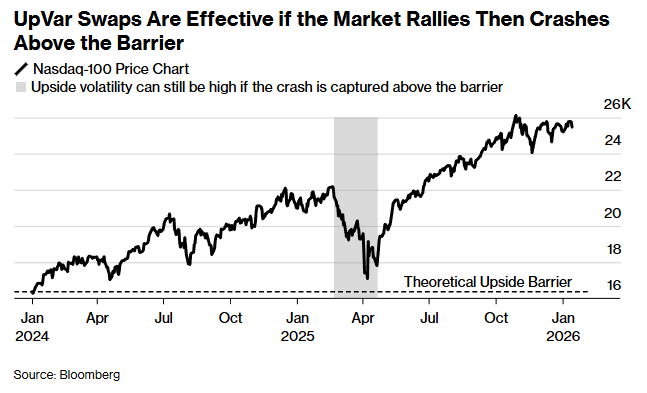

UpVar Swap

As the pattern of simultaneous stock price and volatility increases becomes more evident, trading ideas that bet on this market trajectory are gaining popularity—a phenomenon observed during AI-driven rallies and past speculative phases. Multiple banks are promoting the so-called ‘UpVar swap,’ a strategy that bets on volatility rising when the underlying asset exceeds a certain level. This trade often profits when the market surges sharply and then collapses within a set timeframe.

Strategists from Bank of America, JPMorgan, and Barclays all recommend 1- to 2-year UpVar swaps on the S&P 500 or Nasdaq 100. Priced to focus on relatively cheaper call option strikes rather than higher-volatility put options, these swaps offer a significant discount compared to standard swaps.

The ‘UpVar swap’ works best if the market rises first, then falls and remains above the barrier level.

Currie noted, ‘With skew still relatively steep and absolute volatility low, the pricing of UpVar swaps remains attractive. Investors are expressing a variety of perspectives – some are tactical trades targeting U.S. indices with maturities ranging from six months to two years, aiming to capture rising volatility or spot price increases; others are using arbitrage structures such as selling volatility swaps and buying UpVar.’

Upside Opportunities in European Equities

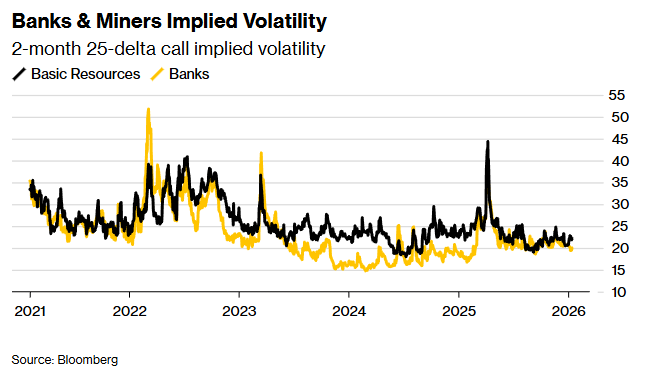

European banks remain a popular allocation, with many strategists expecting their strong rebound in 2025 to continue into this year. Various trades focus on cheaper upside strategies, such as purchasing call options on the Euro Stoxx Bank Index with a higher knockout level. The risk with these cheaper options is that they become worthless if the index reaches the specified level.

European mining stocks are also garnering attention, with strategists recommending exposure to upside opportunities in the STOXX 600 Basic Resources Index. In a recent report, Barclays stated that potential Chinese policy support and AI infrastructure demand could improve sector fundamentals. They find spread structures particularly appealing under conditions of low volatility and flat bullish skew.

Implied Volatility in Banks and Mining – 2-Month 25-Delta Call Implied Volatility

Hedging Tail Risks in Tech Giants

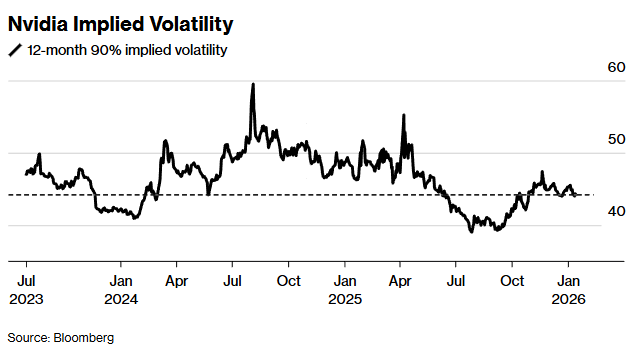

Similar to April last year, investors tend to buy volatility (Vega) exposure in large-cap tech stocks for protection, betting that volatility will surge during sell-offs. Barclays strategists consider ‘crash volatility’ in the tech sector an inexpensive way to hedge concentration risks and uncertainties around AI capital expenditures, with structural flows making put options more attractively priced. They recommend purchasing out-of-the-money December-expiring Apple and NVIDIA put options. Similarly, Bank of America strategists suggest going long deep out-of-the-money long-term NVIDIA put options while delta-hedging, betting on rising volatility when stock prices fall.

NVIDIA Implied Volatility

VIX Spread Strategy

A major issue over the past two years has been whether to hedge macro risks by purchasing call options on the Cboe Volatility Index (VIX) or selling put options on the S&P 500 Index. While VIX call options often provide the potential for quick profits during market sell-offs, volatility spikes tend to reverse rapidly. Additionally, the steep VIX futures curve increases the cost of holding call options, as more expensive forward contracts gradually converge toward the spot index over time.

JPMorgan strategists recommend using short-term call spreads to hedge against headline risks while leveraging the steep skew in VIX call options to limit costs. The JPMorgan strategist team, led by Bram Kaplan, noted: “The VIX appears disconnected from policy risks, but if those risks materialize, it could quickly catch up.” “Systematic investors are heavily positioned, so if we see a shift in market momentum and volatility begins to rise, the deleveraging of these strategies and hedging of convexity products may accelerate market declines and further drive up volatility.”

Editor/Liam