Global government bonds experience a broad-based rally as market logic shifts from ‘rate hike panic’ to ‘recession pricing.’

Amid concerns that conflicts in the Middle East could disrupt global economic growth, demand for previously sold-off government bonds rebounded, driving a broad-based rise in global sovereign bond prices.

According to Zhitong Finance, demand for previously sold-off government bonds rebounded as markets worried that conflicts in the Middle East could disrupt global economic growth, leading to a broad rise in global sovereign bond prices.

During Asian trading hours, U.S. Treasury bonds rose in tandem with those of Australia and Japan, driven by expectations that the surge in crude oil prices might be a precursor to a prolonged fuel shortage. This boosted demand for government bonds, which had been under continuous selling pressure due to concerns over accelerating inflation overshadowing their traditional safe-haven appeal.

Gareth Berry, a strategist at Macquarie Group Limited, stated: “The market is now trying hard to imagine what the global situation will look like if the war in the Middle East remains unresolved within a month. People have started comparing it to the COVID-19 pandemic, with the risk of an economic shutdown this time triggered by fuel shortages.”

This rally in government bonds followed weeks of selling, primarily due to fears of surging oil prices and central bank interest rate hikes. Recent market focus has shifted to slowing economic growth, alleviating concerns that central banks would need to adopt an aggressively hawkish stance to control inflation.

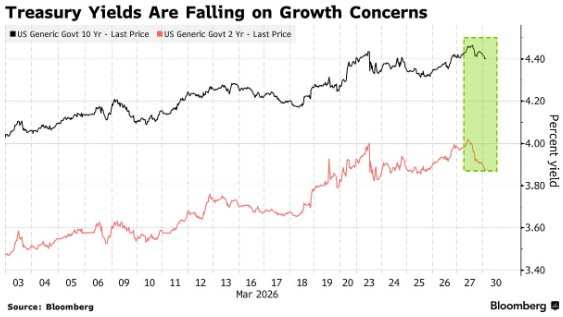

The yield on two-year U.S. Treasury bonds, which are most sensitive to changes in monetary policy, fell by 3 basis points to 3.88%, after declining by 7 basis points last Friday. The benchmark 10-year Treasury yield dropped by 4 basis points to 4.39%.

Australia’s three-year government bond yield once plummeted by 9 basis points to 4.71%, while Japan’s two-year government bond yield declined by 2 basis points to 1.36%.

Strategist Garfield Reynolds opined: “As investors shift focus from digesting the war-induced spike in inflation expectations throughout March to concerns about slowing economic growth, the ‘bull steepening’ trend in the bond market may continue.”

Major U.S. bond funds such as Pacific Investment Management Company (PIMCO) have indicated that financial markets are underestimating the risks of a sharp economic slowdown caused by the war in Iran. Goldman Sachs noted that the probability of a recession within the next year has risen to about 30%.

Ed Yardeni, a veteran Wall Street analyst, stated that since the outbreak of the conflict, “bond vigilantes” have become active globally, leading to excessively bearish sentiment in some segments of the bond market.

In his research report discussing U.S. Treasury bonds, Yardeni wrote: “The front end of the yield curve has already priced in expectations of tightening policies, but we believe this will not occur, meaning this segment is currently oversold.”

Apollo Global Management stated that the yield on the 10-year U.S. Treasury should be around 3.90%, significantly lower than the current level above 4.40%. Torsten Slok, the firm’s chief economist, wrote in a client note: “The key point is that the 10-year yield is 55 basis points higher than a reasonable level, and investors need to carefully consider the reasons behind it.”