Gold stocks experience a ‘roller-coaster’ ride, with some funds erasing their year-to-date gains in a single day. How are fund managers responding to this tough start to the year?

①The actively managed equity funds that performed well in January were mostly those heavily invested in resource commodities, and most of them experienced a drawdown of more than 7% on Monday this week; ②however, some high-performing funds only saw a single-day drawdown of around 2%, significantly lower than the average.

Cailian Press, February 3rd, by reporter Zhou Xiaoya: With the sharp reversal in the precious metals and non-ferrous metals sectors, how will active equity fund managers respond?

Based on the latest net asset value updates of funds, there was a noticeable divergence among funds with leading January returns on Monday. Some funds have already made significant portfolio adjustments, avoiding substantial drawdowns caused by sector corrections; other funds, due to heavy exposure to sharply corrected sectors, suffered large drawdowns on Monday; notably, some products almost wiped out their year-to-date gains in just one day on Monday.

On the day gold stocks plummeted, some fund managers with heavy positions had already adjusted their portfolios in advance

On the first trading day of February, the sharp decline in the gold stock sector became the market’s focus. Zijin Mining fell over 8% on Monday, while Chifeng Gold, Shandong Gold, and CICC Gold, among others, hit the daily limit down.

In the non-monetary ETF market, Shanghai Gold ETFs led the declines, falling more than 12% in a single day, and gold stock ETFs also dropped over 8%.

However, in the active equity fund market, the funds with strong performance in January showed clear divergence in net value drawdowns on Monday. According to Wind data, the Western Lide Strategy Preferred Fund managed by He Qi ranked at the top of the active equity fund market with over 54% net return in January. The fund’s fourth-quarter report indicated that Zijin Mining and Chifeng Gold were its top two largest holdings, each accounting for over 9% of the portfolio, with A-shares and H-shares of Shandong Gold and CICC Gold also among its major holdings.

Nevertheless, the fund’s net value only retreated by 1.86% on Monday, significantly less than the declines of its major holdings, bringing its year-to-date net return to 51.87%.

Similarly, the Western Lide New Power Fund managed by He Qi has also performed well year-to-date, with three out of its top four holdings being gold stocks. However, its single-day decline on Monday was within 2%.

Looking further back, on the last trading day of January, these two products also experienced relatively small net value drawdowns. At that time, signs of adjustment had already emerged in the gold stock and non-ferrous metal sectors, but the single-day net value drawdown of the funds did not exceed 1%.

Multiple top-performing funds this year experienced a single-day drawdown exceeding 7%.

Although some funds had smaller drawdowns, overall, actively managed equity funds that heavily invested in resource sectors and performed well in January mostly saw declines of over 7% on Monday.

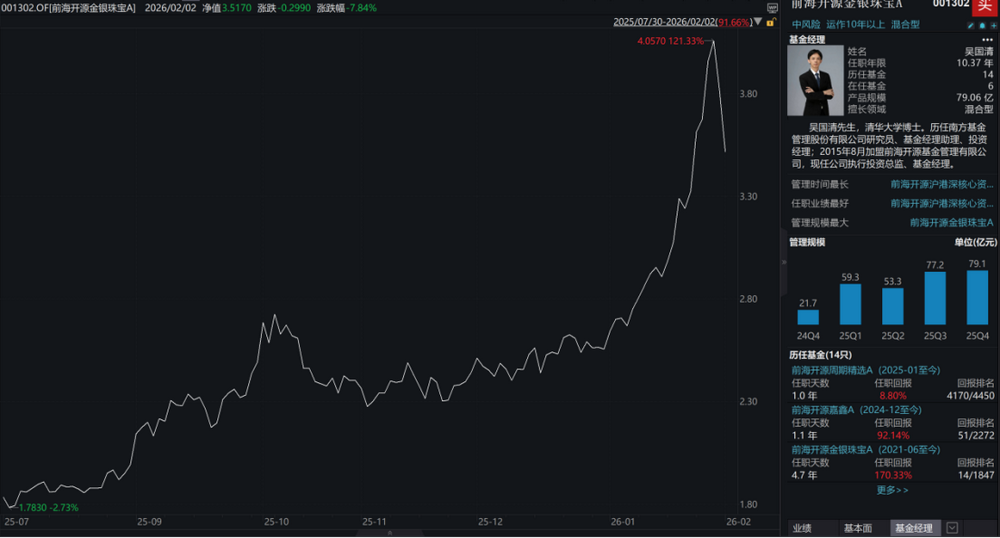

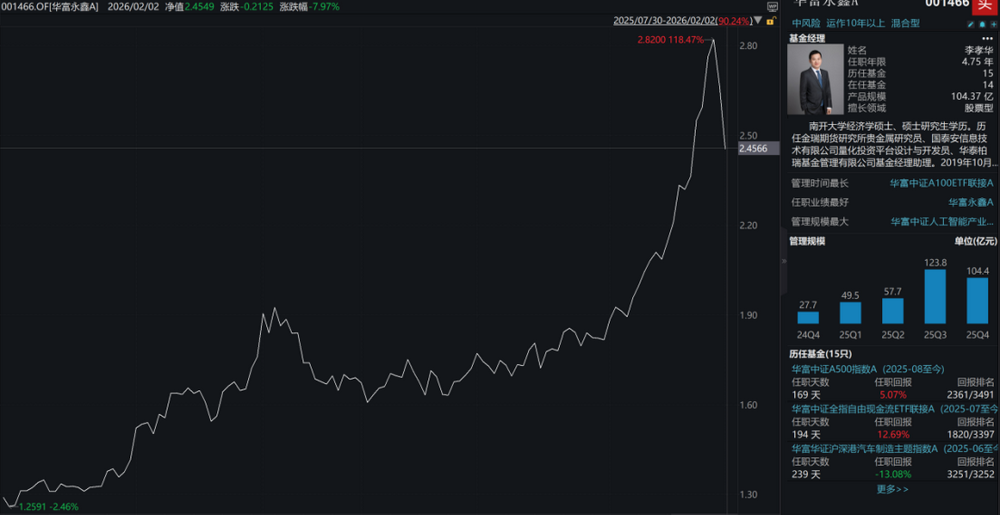

For instance, the Qianhai Open Source Gold & Jewelry Fund experienced a 7.84% drawdown on Monday, with cumulative losses nearing 14% over the last two trading days (Friday and Monday), bringing its year-to-date return to 37.6%. Similarly, the HuaFu Yongxin fund saw a 7.97% drop in net asset value on Monday, reducing its annual return to 35.08%.

The WanJia Cycle Vision Fund recorded consecutive daily declines of more than 7%, losing 8.61% on Monday alone. As of the end of last year, all of its top ten holdings were stocks from the gold sector. The YinHua TongLi Selection and YinHua NeiXu Selection funds, which also held significant positions in gold stocks at the end of last year, both fell more than 7% on Monday, with their year-to-date returns temporarily dropping to 33.28% and 33.09%, respectively.

Overall, according to Wind data, only 36 actively managed equity funds did not record losses in net asset value on Monday, while over 4,600 other products experienced declines. The average single-day drawdown for actively managed equity funds was 3.53%, with more than a hundred funds experiencing drawdowns exceeding 6%.

How should we interpret this adjustment?

Following the significant single-day decline in net asset value, one major uncertainty facing fund investors is how long the market will continue to adjust. In this regard, Long Jiangwei, a fund manager at Hang Seng Qianhai, stated that the significant adjustment in the A-share market on Monday was due to the叠加of multiple short-term negative factors, resulting in a concentrated release of pessimism.

“Despite the large market decline and prevailing pessimism, we believe this pullback represents a normal, rational market adjustment rather than a trend reversal.” He analyzed that the core rationale lies in two points: First, the primary driver of this sell-off is the concentrated release of short-term sentiment and the叠加of multiple negative factors, rather than any fundamental deterioration in macroeconomic conditions or industrial trends; second, the A-share market accumulated substantial profits earlier, and there was an inherent need for correction. This decline essentially serves as a reasonable correction to the previous rapid rise, helping to mitigate market risks, alleviate valuation pressures, and lay the groundwork for healthier market performance going forward.

In terms of specific directions, he believes that in the medium to long term, with the ongoing geopolitical dynamics, independent and controllable technological innovation remains a critical area that the nation must strongly support and promote. It is also an essential lever for expanding domestic circulation, fostering new productive forces, and enhancing productivity. Therefore, sectors representing technological innovation, such as domestic computing power, robotics, and commercial aerospace, remain favorable. At the same time, considering continued policy support, he recommends closely monitoring investment opportunities in pro-cyclical sectors tied to domestic demand.

“In the short term, the prior rapid rise in the A-share market coupled with the approach of the Spring Festival has generated an intrinsic need for consolidation and stabilization.” CICC believes that, in the medium term, the factors supporting market performance have not changed, and the A-share market has the potential to form a slow bull market. Regarding allocation, they suggest that large-cap growth styles still dominate, while an increasing number of opportunities for catch-up rallies in previously low-priced stocks are emerging.

Regarding the non-ferrous metals sector, they believe that prices have fluctuated significantly recently, but from a medium-term perspective, the supporting logic has not yet reversed. The technology sector remains a key area for capital allocation. It is recommended to focus on segments of the AI industry chain such as optical modules, semiconductors, cloud computing infrastructure, and energy storage, while on the application side, attention should be paid to robotics and autonomous driving. Cyclical plays represented by the real estate supply chain and broad consumption remain skewed towards the left side. Considering both capacity cycles and enterprises’ aspirations to expand overseas markets, attention should be given to sectors such as chemicals, power grid equipment, construction machinery, home appliances, and commercial vehicles.

Valuation After A 30% One Month Share Price Decline")