Gold Surges 65%, Dollar Weakens, Trump’s Return Shakes the Globe

Although most investors had long anticipated that the market landscape in 2025 would be different with Trump returning to the helm of the world’s largest economy, few could have foreseen the volatility and ultimate outcome of this trend.

Although most investors had long anticipated that the market landscape in 2025 would be different with Trump returning to the helm of the world’s largest economy, few could have foreseen the volatility and complexity of this trend, as well as the ultimate outcome.

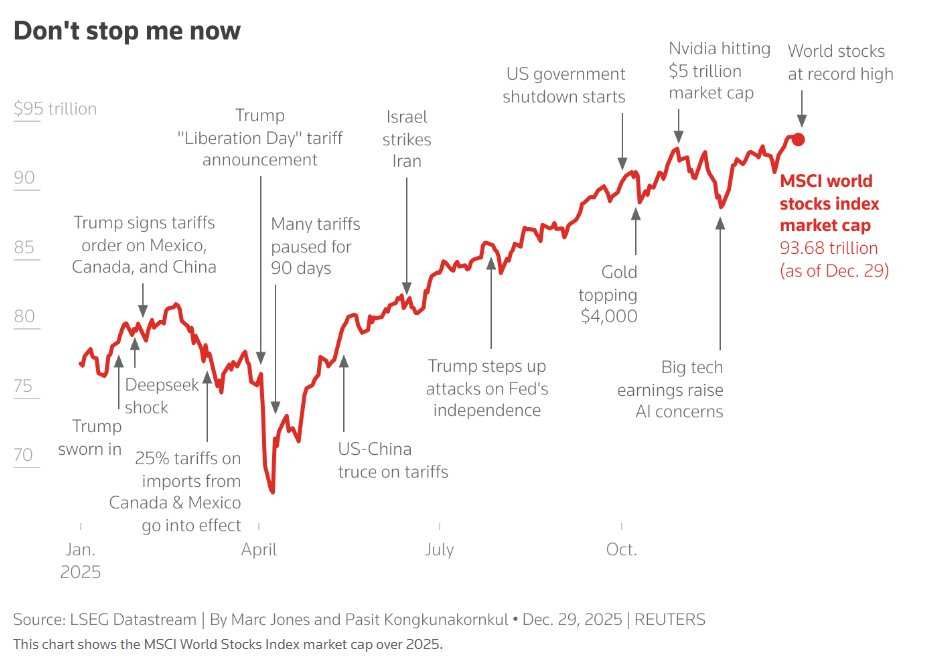

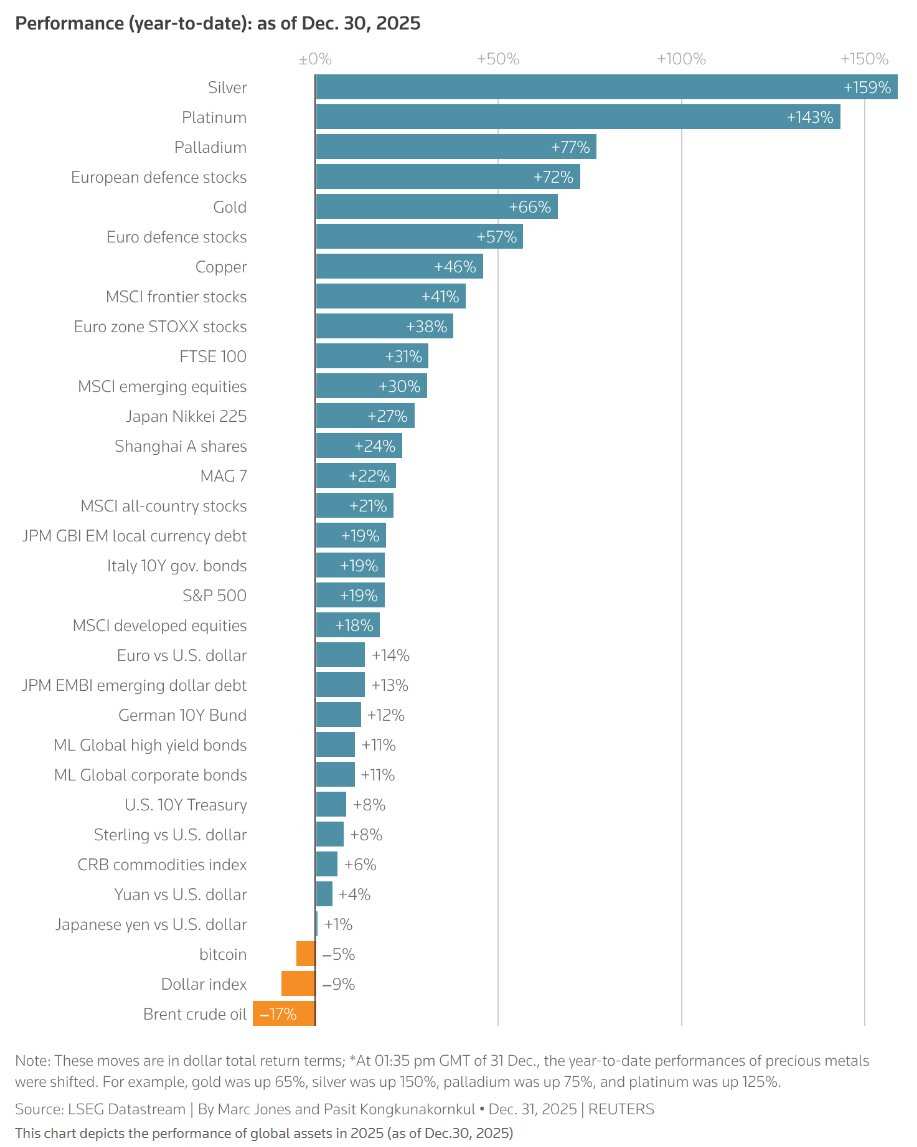

Global equities strongly rebounded from the slump triggered by the ‘Liberation Day’ tariff policy in April, with a full-year gain of 21% in 2025, marking the sixth double-digit growth in the past seven years. However, across other asset classes, surprises were abundant.

Gold, widely regarded as a safe haven in turbulent times, experienced its best year since the 1979 oil crisis, with annual gains approaching 65%. In contrast,$USD (USDindex.FX)$the stock market fell nearly 10%, crude oil prices dropped by approximately 18%, while the riskiest segment of the bond market, junk bonds, surged unexpectedly.

Since the artificial intelligence (AI) leader NVIDIA$NVIDIA (NVDA.US)$became the world’s first company to surpass a market capitalization of $5 trillion in October, the luster of America’s ‘Magnificent Seven’ seems to have dimmed somewhat,$Bitcoin (BTC.CC)$with its market value abruptly shrinking by one-third.

Bill Campbell, a portfolio manager at DoubleLine Capital, described 2025 as ‘a year of transformation and surprises.’ He noted that the sharp fluctuations across various asset classes were ‘closely intertwined’ with three major disruptive themes: trade wars, geopolitical tensions, and debt issues.

Campbell remarked, ‘If someone had told me beforehand that Trump would return to the White House and implement aggressive trade policies at the current pace, I would never have anticipated valuations remaining as robust or elevated as they are today.’

Influenced by Trump’s policies, European defense stocks surged 56% for the year. Earlier signals indicated that the Trump administration would scale back military protection for Europe, compelling European nations and other NATO members to accelerate their military build-up.

This trend also propelled European bank stocks to their best annual performance since 1997;$Korea Composite Index (.KOSPI.KR)$gains reached 75%, while the return on Venezuelan defaulted bonds approached nearly 100%; silver and platinum also shone brightly, surging 145% and 125% respectively.

Three interest rate cuts by the Federal Reserve during the year, public criticism of the Fed by Trump, and mounting global concerns over debt collectively impacted the bond market.

The ‘big and beautiful’ spending plans introduced by the Trump administration once fueled$U.S. 30-Year Treasury Bonds Yield (US30Y.BD)$In May, it broke through 5.1%, reaching the highest level since 2007. Although the current yield has retreated to 4.8%, the ‘term premium’—the widening spread between long-term and short-term interest rates as described by bankers—is once again causing market panic.

$Japan 30-Year Treasury Notes Yield (JP30Y.BD)$It also climbed to a record high. Paradoxically, global bond market volatility is at a four-year low, while emerging market bonds denominated in local currencies are experiencing their best year since 2009.

Companies have borrowed heavily to position themselves in AI, making AI an important factor influencing the debt market. Goldman Sachs estimates that large-scale ‘hyperscale’ AI companies will invest nearly $400 billion in 2025, and this figure is expected to rise to $530 billion by 2026.

Gold is not the only asset shining brightly.

The weakening of the US dollar drove the euro to a nearly 14% gain in 2025, with the Swiss franc rising by 14.5%; although the yen plummeted in December, its exchange rate ended the year flat.

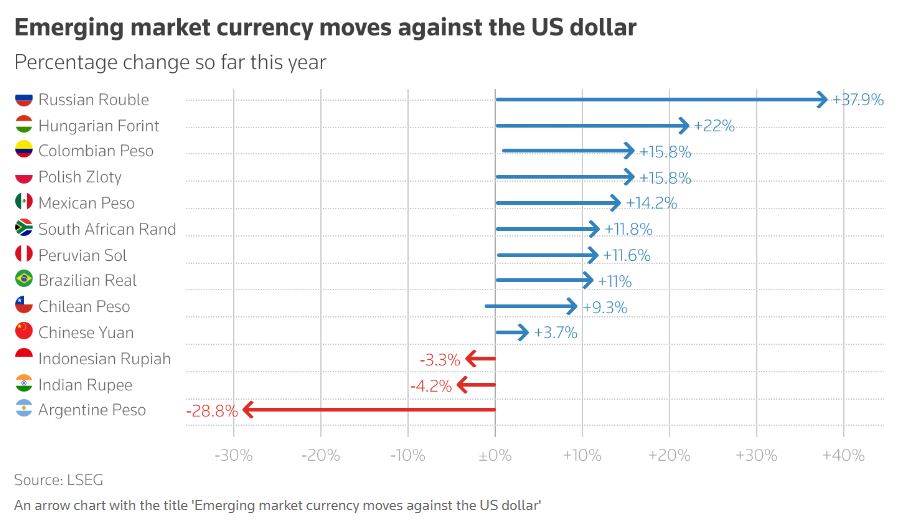

Trump’s renewed engagement with Russian President Putin spurred a 40% surge in the Russian ruble. However, the ruble remains constrained by stringent sanctions, and the title of the best-performing currency for the year was ultimately claimed by the Ghanaian cedi — the currency of this gold-producing nation surged by 41% for the year.

The Polish zloty, Czech koruna, and Hungarian forint gained between 15% and 21%; in May, the New Taiwan Dollar soared by 8% against the US dollar within just two days; the Mexican peso and Brazilian real both achieved double-digit gains despite trade war headwinds.

Jonny Goulden, Head of Emerging Markets Fixed Income Strategy Research at JPMorgan, stated: “We believe this is far from a short-term phenomenon. The 14-year bear market for emerging market currencies has now bottomed out and reversed.”

Argentina’s market also performed impressively. In September, Argentine President Javier Milei suffered a crushing defeat in local elections, causing a sharp downturn in the country’s markets; however, weeks later, the Trump administration pledged $20 billion in aid, helping Milei secure a major victory in the national midterm elections, prompting a sharp rebound in Argentina’s markets.

The cryptocurrency sector also experienced significant turbulence. Trump launched his own Meme coin and pardoned Binance founder Changpeng Zhao as president. Bitcoin prices briefly exceeded $125,000 in October, setting a new all-time high, but subsequently plummeted below $88,000, resulting in a cumulative annual decline of over 6%.

New Year, New Worries

The market opening in 2026 is bound to be anything but calm.

Trump has been actively campaigning for the November midterm elections and is expected to soon nominate a new Federal Reserve Chair—a appointment critical to the Fed’s independence.

Israel plans to hold parliamentary elections by the end of October, with the fragile ceasefire in Gaza continuing to capture market attention; an end to the Russia-Ukraine conflict remains fraught with difficulties; Hungarian Prime Minister Orban will face the toughest electoral test of his tenure in April; Colombia and Brazil will also hold key general elections in May and October, respectively.

Moreover, numerous unknown variables remain in the AI sector.

Matt King, founder of Satori Insights, pointed out that based on valuation levels, the market is entering 2026 in an ‘extraordinary’ state; political leaders like Trump are ‘scrambling for excuses’ to offer concessions to voters through economic stimulus or tax cuts.

Matt King stated, ‘The effects of loose monetary policy are being pushed to their limits, and this risk continues to persist.’

‘From the rise in term premiums in the bond market, to the sudden crash of Bitcoin, to the continued rally in gold, cracks have already begun to appear at the fringes of the market.’

Editor/Rocky