How US Fixed-Income Funds Navigated a Turbulent Q1

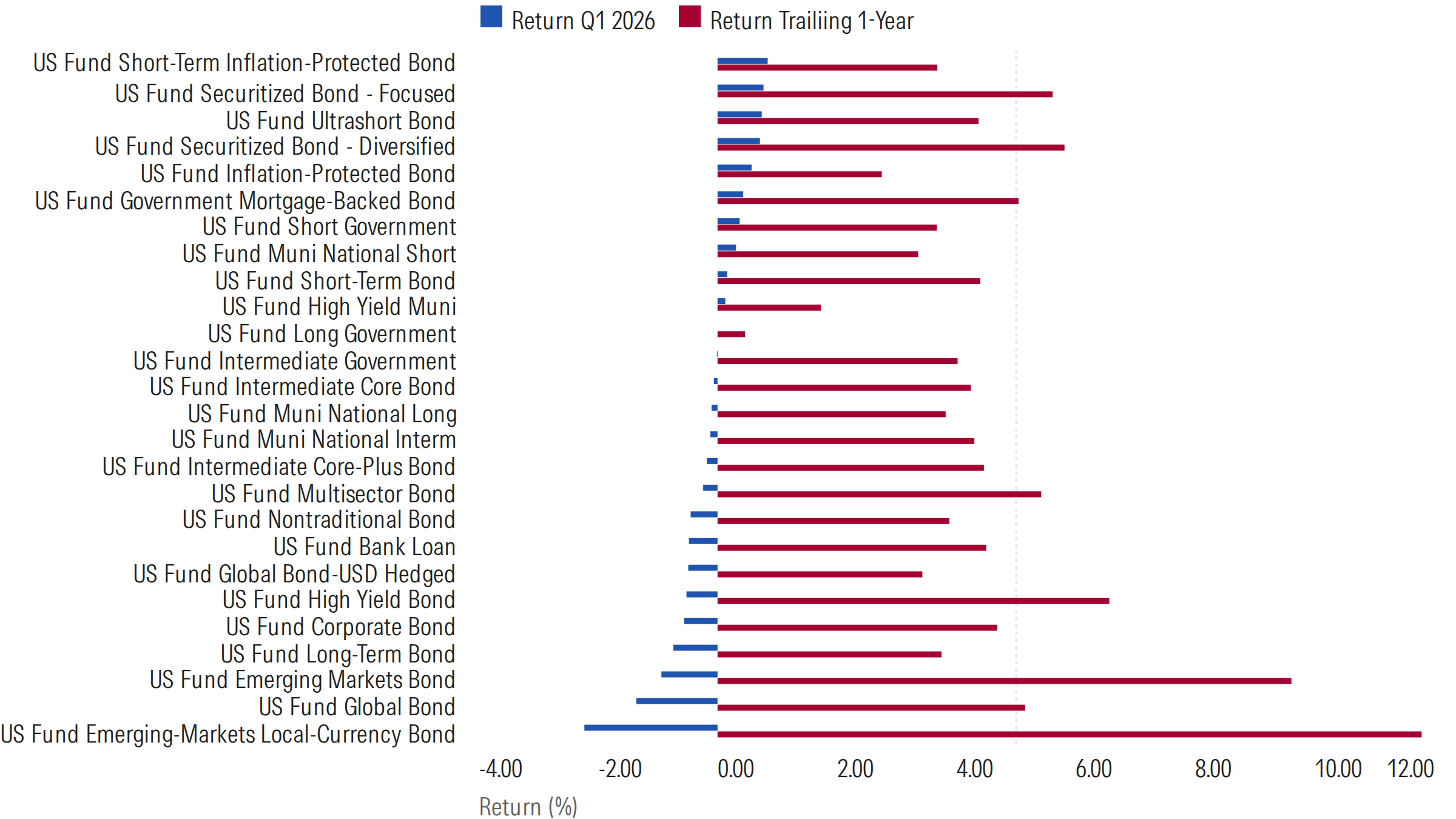

The US fixed-income markets started 2026 on a positive note before the Iran war abruptly changed the macro environment’s tune. The Morningstar US Core Bond Index, a proxy for the US-dollar-denominated investment-grade bond market, gained 1.88% in the year’s first two months before shedding most of those gains in March and settling at a mere 0.10% return for the first quarter.

The period had two very distinct halves. From January through mid-February, softer economic data seemed to pave the way for sooner-than-expected Federal Reserve interest rate cuts. The 10-Year Treasury yield dropped to 3.97% by the end of February, causing prices to rally. The Feb. 28 start of the Iran war tore that path up. Rather than acting as a safe haven, as it often does, the 10-Year Treasury yield climbed to 4.88% by the end of March, which sent prices down. Treasury yields rose across the curve because of fear that higher energy prices would exacerbate inflation. Longer-duration bonds bore the brunt. The typical long-term bond Morningstar Category fund, which invests in long-dated corporate and Treasury bonds and carries a duration of 11.5 years, lost 0.74% during the quarter.

Meanwhile, ultrashort bond funds demonstrated their hallmark quality: capital preservation in stressed markets. With less interest rate sensitivity (a duration of less than one year), the typical fund in the ultrashort bond category gained 0.74% during the quarter.

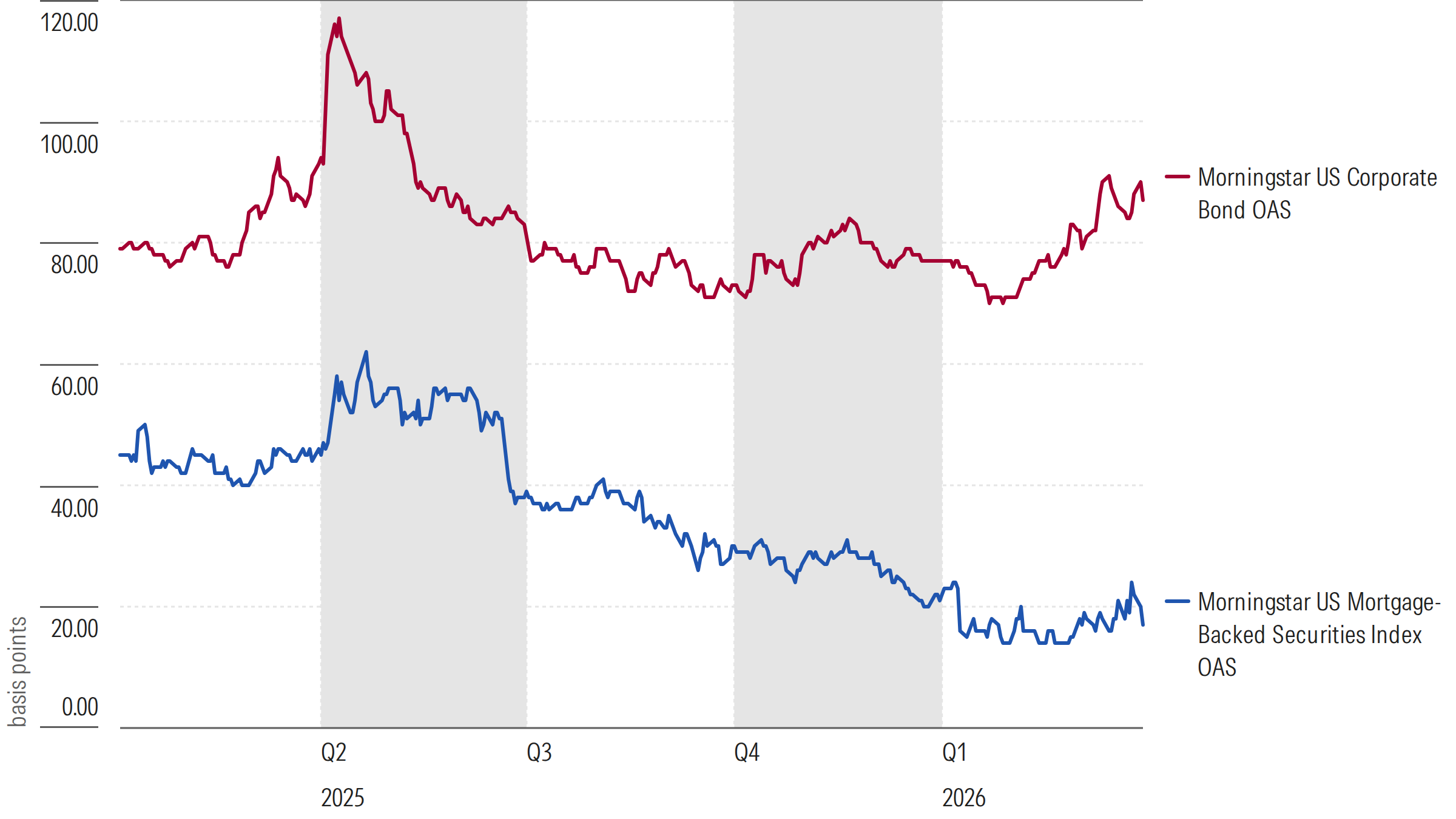

Corporate bonds and the funds focused on them faltered, as the difference between the yields of corporate bonds and Treasuries with the same level of interest rate sensitivity (as measured by duration) widened. Investment-grade corporates, as represented by the Morningstar US Corporate Bond Index, finished the quarter down 0.41%, while the Morningstar US Treasury Bond Index gained 0.01%.

Here’s how some of our favorite managers in a few bond fund categories fared during the quarter.

Emerging-Market Bonds Suffered

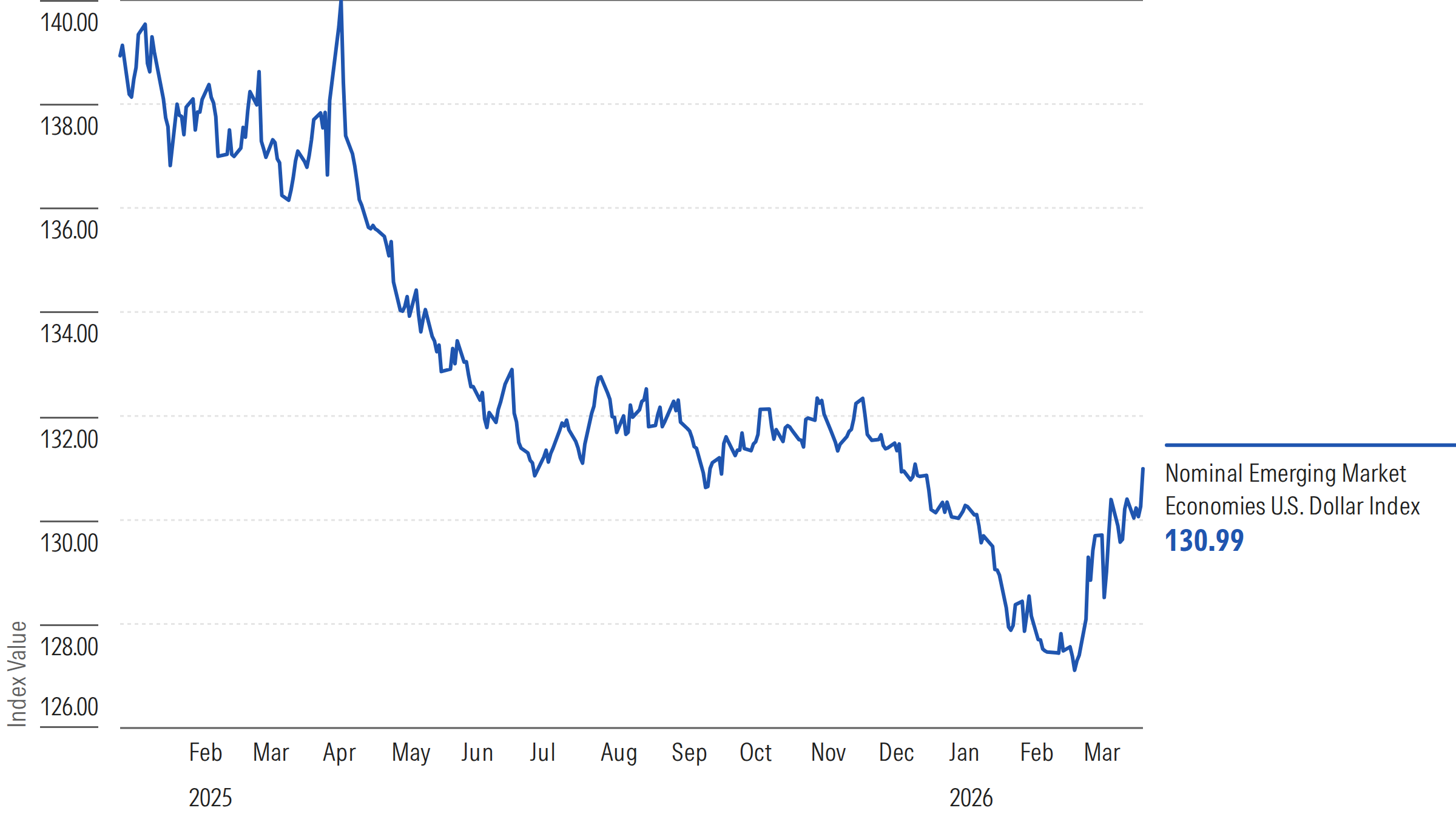

After posting stocklike returns in 2025, emerging-market debt lagged all fixed-income sectors amid rising geopolitical tensions. The typical emerging-market bond category fund, which invests more than 65% of assets in bonds from developing countries, lost 0.94% during the quarter, while its emerging-market local-currency bond counterpart, which takes more foreign-currency risk, lost 2.23%.

The weakening dollar, which had driven emerging-market local-currency debt gains in 2025, strengthened in the quarter as investors reassessed the geopolitical and inflationary outlook. Pimco Emerging Markets Local Currency and Bond PELBX, which has a Morningstar Medalist Rating of Gold, lost 2.64% during the quarter after gaining 22.92% in 2025.

Short-Term Inflation-Protected Bond Funds Delivered

Short-term inflation-protected bond funds were a bright spot. These funds invest in bonds whose returns rise with inflation, such as Treasury Inflation‑Protected Securities. TIPS adjust their coupon payments when consumer price inflation, or the prices paid by US consumers, changes.

The typical short-term inflation-protected category fund gained 0.84% during the quarter. These funds benefited from rising near-term inflation expectations while their low duration shielded them from volatility. Gold-rated Vanguard Short-Term Inflation-Protected Securities ETF VTIP, which tracks the Bloomberg US TIPS 0-5 Years Index, gained 0.97% during the quarter and landed in the category’s top quartile. Its shorter-than-average duration boosted returns as short-term rates rose.

Securitized Debt Outperformed

Securitized debt outperformed US corporate debt during the first quarter thanks to stable fundamentals, strong demand, and a smaller yield gap with Treasuries. The Morningstar US Mortgage-Backed Securities Index gained 0.59% during the quarter, versus the Morningstar US Corporate Bond Index’s 0.41% loss.

The typical securitized-debt focused bond fund, which invests at least 65% of its assets in the investment-grade debt of a single securitized sector, gained 0.77% during the quarter. Bronze-rated Janus Henderson AAA CLO ETF’s JAAA 0.91% gain for the quarter was due to its helping of floating-rate collateralized loan obligations that are less sensitive to interest rate volatility.