inflation trades take a backseat as recession concerns quietly emerge.

As inflation concerns triggered by the conflict in Iran gradually escalate, bond investors are beginning to contemplate a deeper issue: could surging oil prices ultimately pose a threat to economic growth?

According to Zhitong Finance, as inflation concerns triggered by the conflict in Iran gradually escalate, bond investors have begun to contemplate a deeper issue: will surging oil prices ultimately evolve into a threat to economic growth?

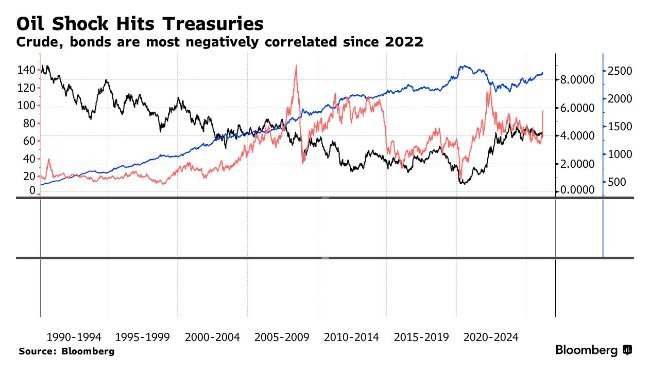

Currently, crude oil prices have climbed to their highest level since the Russia-Ukraine conflict in 2022—the last time when U.S. Treasuries and crude oil were highly correlated. Naturally, upward pressure on inflation has become the primary risk in investors’ eyes. This is also expected to be a key focus for Federal Reserve officials at this week’s interest rate meeting.

However, as the conflict enters its third week, market expectations of Fed rate cuts are gradually fading. An increasing number of people are beginning to discuss how soaring energy prices could ultimately undermine the economy, especially given the already weakening labor market and consumer spending. Priya Misra of JPMorgan Asset Management believes that, against this backdrop, the rise in the 10-year Treasury yield from 3.94% at the end of February to 4.25% or higher is starting to look attractive.

“You never want to catch a falling knife,” the portfolio manager said, “but when the market has undergone significant repricing and positions are cleaner, it might be a good opportunity to position for a ‘growth shock’—which typically follows an inflation shock.”

Misra’s perspective captures the growing tension brewing in the bond market: whether to respond immediately to the initial rise in oil prices or anticipate their subsequent impact on economic growth, the market finds itself in a dilemma.

This debate over which force will dominate the market could shape the core trading logic of U.S. Treasuries in the coming months—indicating potential room for the market to turn bullish, forcing traders to price in more easing policies from the Fed, thereby pushing yields lower again.

March Reversal

The sell-off in U.S. Treasuries this month marks a significant shift. As recently as February, concerns that artificial intelligence (AI) might disrupt certain industries had driven a rally in the bond market.

Since the United States and Israel struck Iran and Iran retaliated, inflation concerns have taken center stage. The global benchmark Brent crude closed last week at around $103 per barrel, up about 40% from the end of February, adding further pressure to already elevated inflation.

The surge in oil prices has placed the Federal Reserve in a dilemma—it has failed to meet its 2% inflation target for five consecutive years. Dario Perkins of TS Lombard noted that while not every major oil market shock has been accompanied by a recession, the most severe economic downturns in the United States—including those in 1974, 1981, 1990, 2001, and 2008—all occurred after sudden spikes in energy prices.

Morgan Stanley strategists told clients last Friday that U.S. Treasuries ‘have the conditions for a reversal triggered by demand destruction.’ They are using the one-year forward one-year inflation swap rate to identify signals of when rising oil prices might lead to a cooling rather than an increase in inflation.

‘Once rising oil prices no longer push up the 1y1y inflation swap rate but instead cause it to decline, we believe investors should increase their holdings of U.S. Treasuries,’ they stated.

Macro strategist Edward Harrison: ‘After a supply disruption, for the oil market to rebalance, prices must rise to levels sufficient to force a reduction in demand. A decline in demand requires a slowdown in economic activity and weaker growth. This is a classic stagflationary shock, and it remains unclear whether slower growth or higher inflation will become the dominant factor.’

At this week’s Federal Reserve meeting, markets will closely watch whether officials stick to their December forecast of a single interest rate cut in 2026.

The swaps market currently predicts less than one full rate cut by the Fed this year, compared with expectations of three cuts just two weeks ago. Data compiled by the Atlanta Fed even shows option pricing indicating more than a 20% probability of a rate hike before December.

Barclays strategists believe the market may be underestimating growth risks. Last week, they recommended a series of bond-bullish positions, including going long December 2027 short-term interest rate futures, betting that the Fed will implement more easing than the market anticipates.

James Athey, portfolio manager at Marlborough Investment Management, said he had increased his exposure to U.S. bonds after the recent sell-off and believes that while Fed rate cuts may be delayed, they will not be canceled.

‘We are indeed facing more severe consequences from rising oil prices,’ he said. ‘If developments move in this direction, I believe this should not be viewed as an inflationary shock — which is how the current market is pricing it — but rather as a growth shock driven by risk aversion.’

Overall, financial markets have not yet signaled significant concerns about growth, with the S&P 500 index down only about 5% from its all-time high set in January.

A 2024 study by the Federal Reserve found that the surge in oil prices following the outbreak of the Russia-Ukraine conflict pushed up overall inflation but had limited impact on core inflation and broader economic activity, partly because energy accounts for a relatively small share of production and consumption in the U.S.

The key question, however, is how long oil prices will remain at elevated levels. The threat of persistently high oil prices is rising after U.S. President Trump and Iran’s new Supreme Leader Mojtaba Khamenei adopted tough stances last week. This undoubtedly increases risks against the backdrop of an economy already showing signs of losing momentum.

John Briggs, Head of U.S. Interest Rate Strategy at Natixis North America, stated that given data showing U.S. employers cut jobs in February and the unemployment rate rose, markets are underpricing the probability of the Federal Reserve implementing easing policies before June.

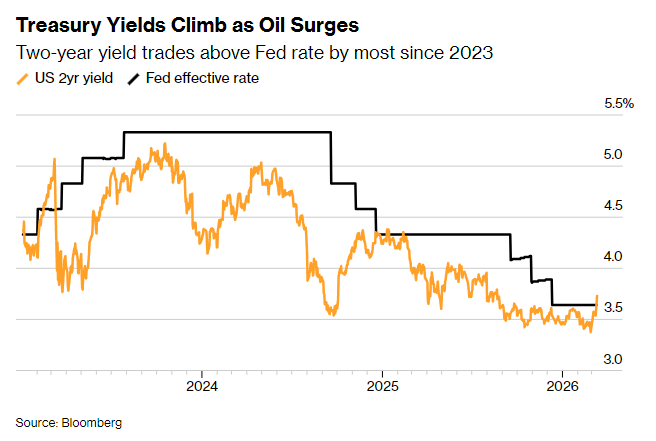

He believes the two-year Treasury yield, at around 3.7%, higher than the Fed’s effective federal funds rate, has entered a buyable range.

“It is worth gradually building positions in two-year Treasuries because they should benefit from downside risks to growth,” he said.

Faces Headwinds Amid Municipal Bond Stability")