Jazz Pharmaceuticals Stock at $185: Here’s Why Analysts See a New All-Time High in 2026

Key Stats for Jazz Pharmaceuticals Stock

- Past-Week Performance: -4.2%

- 52-Week Range: $95.5 to $198

- Current Price: $185.4

What Happened?

Jazz Pharmaceuticals (JAZZ), an Ireland-based biopharma long defined by its sleep drug franchise, filed a completed regulatory application for zanidatamab, a cancer therapy posting over 2 years of median survival in a tumor where 5-year survival sits below 10%, signaling a structural identity shift now trading at $185.40.

Last week, Jazz confirmed its completed sBLA filing with the FDA for zanidatamab, a HER2-targeting bispecific antibody therapy, in first-line metastatic gastroesophageal adenocarcinoma, a stomach and esophageal junction cancer, triggering the PDUFA review clock and opening a path to a potential H2 2026 commercial launch.

Jazz’s Q4 2025 revenue of $1.2 billion beat the $1.17 billion consensus by roughly 3%, while Modeyso, a brain cancer drug launched in August 2025 with no prior approved alternative, generated $37 million in its first full quarter against a peak U.S. sales target above $500 million.

Amal Melhem-Bertrandt, Head of Oncology Clinical Development, stated on the March 3 TD Cowen conference that “we’ve now completed the filing for the sBLA for GEA, so PDUFA clock starts,” confirming the submission milestone that positions zanidatamab for a potential H2 2026 launch.

With zanidatamab’s FDA review now running, a second interim OS readout for the GEA trial due mid-year, the ACTION frontline brain cancer trial reading out late 2026 or early 2027, and management guiding for double-digit oncology and epilepsy growth, Jazz Pharmaceuticals’ commercial identity is shifting structurally from a sleep franchise toward a multi-indication rare disease platform worth watching.

Wall Street’s Take on JAZZ Stock

The completed sBLA filing for zanidatamab, a HER2-targeting cancer therapy, on March 3 shifts Jazz from a sleep-drug story into a genuine rare-disease platform with a near-term commercial launch catalyst, directly lifting the forward revenue ceiling.

Analysts project 2026 revenue of $4.4 billion growing to $6.0 billion by 2030, a 7.7% CAGR, while normalized EPS is expected to jump from $8.38 in 2025 to $23.83 in 2026, a 184% recovery driven by the unwind of one-time litigation costs and accelerating oncology launches.

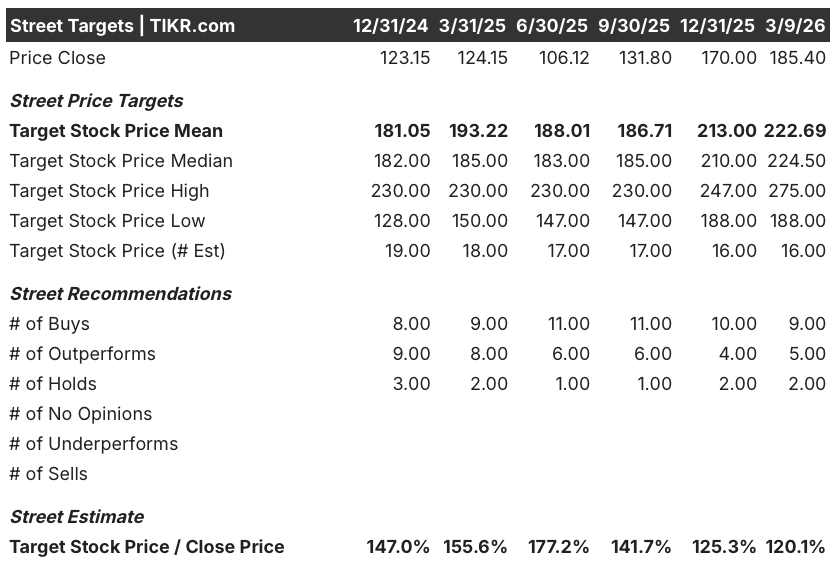

Fourteen analysts covering JAZZ currently rate the stock 9 Buys, 5 Outperforms, and 2 Holds, zero Sells, with a mean price target of $222.69, implying roughly 20.1% upside from the March 9 close of $185.40, a spread that reflects institutional confidence in the H2 2026 zanidatamab launch.

The analyst price target range runs from $188.00 on the low end to $275.00 on the high end, with the floor anchored to Xywav generic competition risk in H2 2026 and the ceiling tied directly to zanidatamab’s FDA approval and a successful GEA commercial launch.

What Does the Valuation Model Say?

TIKR’s mid-case valuation model prices Jazz at $229.21 by December 2030, a 23.6% total return at a 4.5% IRR, assuming a 6.8% revenue CAGR and net income margins recovering from 12.2% in 2025 to 37.1% by 2030.

The market is pricing Jazz at roughly 8x forward earnings, a sleep-company multiple, while the model prices in a 46% EBITDA margin recovery in 2026 from a depressed 17.2% in 2025, making the current multiple a structural mispricing.

Modeyso, the brain cancer drug launched in August 2025 with no prior approved competitor, generated $37 million in its first full quarter and already carries a peak U.S. sales target above $500 million, directly supporting the model’s margin expansion assumption.

Management confirmed on March 3 that the PDUFA review clock for zanidatamab in first-line GEA has started, a signal that the company’s oncology re-rating is a regulatory timeline, not a speculative one.

The key risk is Xywav, Jazz Pharmaceuticals’ narcolepsy and idiopathic hypersomnia drug generating $1.7 billion in 2025 revenue, facing generic high-sodium oxybate competition in H2 2026 that could compress the sleep franchise and undercut the model’s flat-to-mid-single-digit growth assumption for that product.

The single event to watch is the zanidatamab PDUFA date announcement from the FDA, which confirms whether a H2 2026 launch is on track and whether the $4.4 billion 2026 revenue estimate holds with a new oncology revenue stream contributing.

Should You Invest in Jazz Pharmaceuticals?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up JAZZ stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Jazz Pharmaceuticals alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze JAZZ stock on TIKR for Free →

One of the Shorted Biotech Stocks to Buy")

Valuation After Strong Long Term Returns And A High Current P/E Ratio")

Valuation After Petrelintide Phase 2 Data And Sharp Share Price Drop")