New highs in oil prices struggle to shake the bond market’s ‘defection’; US Treasury trading logic quietly shifts to growth concerns.

The sell-off in the U.S. Treasury market has temporarily eased as investors, increasingly concerned that an energy crisis could push the Federal Reserve to raise interest rates, have turned to U.S. government bonds yielding at their highest levels this year.

According to Zhitong Finance APP, as investor concerns deepen over an energy crisis driving the Federal Reserve to raise interest rates and shift to chase U.S. Treasury yields hitting yearly highs, selling pressure in the U.S. bond market has temporarily eased.

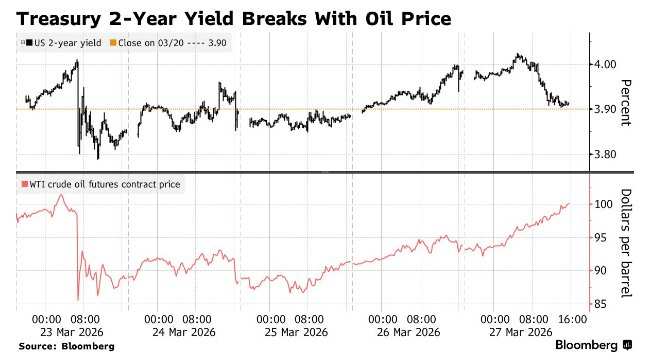

On Friday, benchmark U.S. Treasury yields retreated after climbing to their highest levels since mid-2025. The two-year yield, which is most sensitive to changes in Fed policy, fell by 9 basis points to 3.90% at one point, after earlier touching a high of nearly 4.03%, its highest level since June.

Despite crude oil prices breaking multi-year highs, the bond market rebounded, breaking the recent correlation between the two. Over the past month, investors largely ignored the drag of rising fuel costs on the economy, instead continuing to push yields higher amid growing inflation expectations.

Ian Lyngen, Head of U.S. Rates Strategy at BMO Capital Markets, stated: “The front end of the U.S. Treasury yield curve is no longer tracking energy prices as an inflation risk factor but is instead focusing more on downward pressures on economic growth and risk assets.”

Longer-term Treasury yields also retreated from their yearly highs. The 10-year Treasury yield still rose by nearly 2 basis points to 4.43% on the day, after briefly surpassing 4.48% for the first time since July. Yields across all maturities once touched intraday highs as oil prices continued to climb amid ongoing U.S. military action against Iran, now in its fifth week.

Despite WTI crude oil futures closing at $99.64 per barrel, the highest level since mid-2022, short-term Treasury yields remained near their daily lows. The global benchmark Brent crude also closed at multi-year highs.

This resulted in a steepening of the yield curve, breaking the pattern of the previous month when rising oil prices were accompanied by a flattening curve – a period when investors expected the Fed to respond to rising inflation.

In a report released Friday, Lyngen noted that the day’s market movements signaled the approach of a turning point, marking a shift in “how the market responds to further increases in oil prices,” towards driving a steeper yield curve.

Since the U.S. attack on Iran on February 28 disrupted oil supplies in the region, Treasury yields have generally moved higher with rising oil prices. On Thursday evening, President Trump extended the pause on strikes against Iranian energy facilities by 10 days, causing yields and oil prices to briefly retreat, though he expressed skepticism about the possibility of reaching a peace agreement.

The rise in yields reflects the potential inclusion of U.S. retail gasoline price increases in overall consumer inflation metrics, hindering the Fed’s ability to implement rate cuts that markets had widely anticipated before the conflict erupted.

John Briggs, Head of U.S. Rates Strategy at Natixis, stated that as long as the Strait of Hormuz remains closed, investors will be concerned about ‘inflation and central banks potentially responding with measures akin to those in 2022.’ The oil shock triggered by the Russia-Ukraine conflict in 2022 fueled a post-pandemic surge in inflation, ultimately prompting the Federal Reserve to raise interest rates cumulatively by more than five percentage points before mid-2023.

Macro strategist Michael Ball noted: ‘The next move in the U.S. Treasury yield curve is more likely to steepen, led by a potential reversal in front-end yields. Front-end yields had previously priced in oil-driven inflation aggressively but underestimated the impact of rising energy costs on growth and the labor market.’

Market expectations for inflation over the next year, though down from last week’s highs, have surged from about 2.2% at the start of the year to above 3%. Swap contracts reflecting future Fed rate decisions no longer signal any possibility of rate cuts this year and instead price in a greater than 50% probability of a rate hike.

Molly Brooks,利率策略师 at TD Securities, remarked: ‘The market has completely shifted, with participants moving from questioning when the next rate cut would occur to pricing in rate hikes through 2026.’

The Federal Reserve cut interest rates three times last year to address weakness in the labor market. While related concerns have largely dissipated, February’s employment data still came in weaker than economists had anticipated.

The March employment report will be released next week on April 3 under unusual market conditions, with stock exchanges closed for Good Friday (which is not a federal holiday). The bond market, which operates on a decentralized trading system, will have shortened hours due to the holiday (unless it coincides with a major economic data release date), giving investors only a limited time window to react to the data.

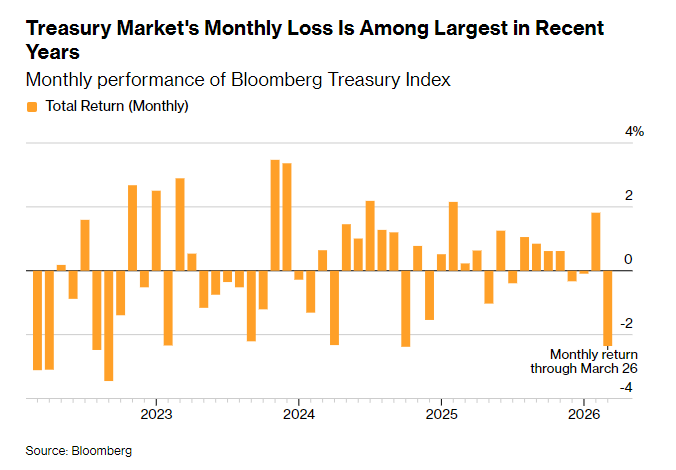

Friday’s market movements are set to result in one of the worst months for the U.S. Treasury market in nearly five years. According to relevant Treasury indices, the U.S. Treasury market has fallen 2.36% so far this month as of March 26. If this decline holds, it will mark the worst-performing month since October 2024.

Andrew Hollenhorst, an economist at Citi, noted in a report that upward pressure on Treasury yields also stems from the prospect of increased U.S. government borrowing—needed both to finance war-related costs and to refinance existing debt at higher interest rates.

This week’s auctions of two-year, five-year, and seven-year Treasury notes all cleared at yields higher than expected, reflecting the average interest rates demanded by investors to meet U.S. government financing needs. The three auctions collectively raised $183 billion.

This marks the worst performance for these three maturities in a single month since May 2024, when traders similarly scaled back bets on rate cuts.

Hollenhorst wrote that the U.S. Treasury bond auction ‘serves as a reminder that fiscal challenges intensify as interest rates rise,’ noting that ‘massive deficits are easier to finance when the Federal Reserve is expected to cut rates,’ while currently ‘expectations for defense spending are on the rise.’