Nittetsu Mining And 2 Other Undiscovered Gems In Asia With Promising Potential

As global markets navigate a period of volatility, with small-cap and value-oriented stocks showing resilience amidst broader economic shifts, investors are increasingly turning their attention to underexplored opportunities in Asia. In this dynamic environment, identifying stocks with strong fundamentals and potential for growth can be key to uncovering hidden gems like Nittetsu Mining and others that may offer promising prospects amid shifting market sentiments.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

Let’s dive into some prime choices out of from the screener.

Simply Wall St Value Rating: ★★★★★☆

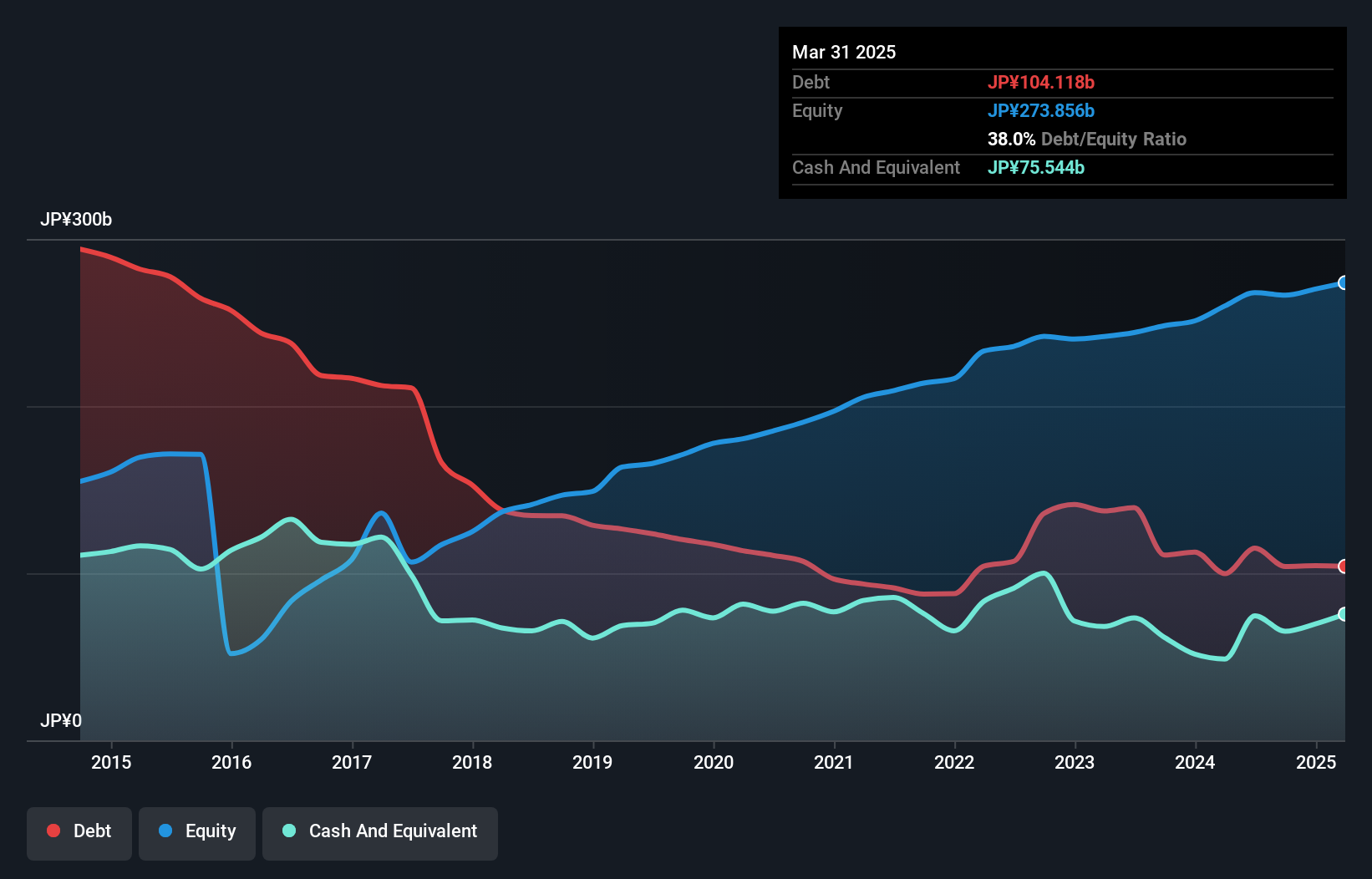

Overview: Nittetsu Mining Co., Ltd., along with its subsidiaries, is involved in mining operations both in Japan and internationally, with a market cap of ¥310.40 billion.

Operations: Nittetsu Mining generates revenue primarily from its mining operations across various locations. The company has a market capitalization of ¥310.40 billion, reflecting its substantial presence in the industry.

In the bustling realm of Asian markets, Nittetsu Mining stands out with its noteworthy performance. Over the past year, earnings surged by 18%, outpacing the broader Metals and Mining industry, which faced a -15% downturn. Despite a rise in its debt to equity ratio from 19% to 29% over five years, the company’s net debt to equity remains satisfactory at 7%. The firm enjoys high-quality earnings and positive free cash flow. However, recent share price volatility might be a concern for some investors. With an upcoming sales statement on February 6th, eyes will be on future growth indicators.

Simply Wall St Value Rating: ★★★★★☆

Overview: Tokuyama Corporation is a Japanese company engaged in the production and sale of diverse chemical products, with a market capitalization of ¥299.29 billion.

Operations: Tokuyama’s primary revenue streams come from its Chemicals segment, generating ¥108.25 billion, and the Electronic & Advanced Materials segment, contributing ¥88.39 billion. The Cement and Life Science segments also add significant revenues of ¥65.35 billion and ¥45.08 billion respectively.

Tokuyama, a noteworthy player in the chemicals sector, is trading at an appealing value, estimated to be 20% below its fair market value. The company’s net debt to equity ratio stands at a satisfactory 36.7%, and its interest payments are comfortably covered by EBIT with a coverage of 222.7 times. Over the past year, earnings have grown by 11.3%, outpacing the industry’s growth rate of 9.4%. Despite revising its guidance downward due to lower chemical product prices, Tokuyama projects a net income of ¥27.5 billion for the fiscal year ending March 2026 and continues to exhibit high-quality earnings performance amidst industry challenges.

Simply Wall St Value Rating: ★★★★☆☆

Overview: The San-in Godo Bank, Ltd., along with its subsidiaries, offers a range of banking products and services to both individual and corporate clients in Japan, with a market capitalization of approximately ¥266.03 billion.

Operations: San-in Godo Bank generates revenue primarily through interest income from loans and securities, alongside fees and commissions from its banking services. The bank’s net profit margin has shown fluctuations, reflecting changes in operating efficiency and external economic conditions.

San-in Godo Bank, with total assets of ¥8,557.2 billion and equity of ¥325.1 billion, is a noteworthy player in the banking sector. The bank’s deposits stand at ¥6,647.5 billion against loans of ¥5,319.4 billion, reflecting a solid base supported by low-risk funding sources comprising 81% customer deposits. Its allowance for bad loans remains insufficient at 69%, yet non-performing loans are appropriately managed at 1.4%. Recent activities include repurchasing shares worth ¥999 million and boosting dividends to JPY 28 per share from JPY 24 last year, signaling shareholder value enhancement efforts amidst steady earnings growth over five years at an annual rate of 12.6%.

Summing It All Up

Seeking Other Investments?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Tokuyama might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Is Up 12.2% After Defining a High-Grade Dilatant Zone")