The energy conflict in the Middle East has eased, oil prices have retreated, U.S. stock futures remain weak, and gold stabilized at $4,660 after a sharp decline.

The anticipated easing of tensions in the Middle East has led to a pullback in international oil prices from their near four-year highs, stabilizing assets in emerging markets. However, inflation concerns triggered by the energy shock have fundamentally reshaped global interest rate expectations. Markets are no longer betting on a Fed rate cut this year, and institutions even predict that the European Central Bank may raise rates as early as April. The sharp contraction in rate-cut expectations, coupled with liquidity demands, has caused fierce sell-offs in precious metals like gold. Currently, gold prices have stabilized with a slight increase.

Signs of easing in the mutual energy attacks between Middle Eastern nations have caused international oil prices to retreat from near four-year highs, alleviating market inflation fears. However, indications of a hawkish pivot by global central banks are driving significant adjustments in the precious metals market.

Overnight statements from the US and Israel eased market concerns about further escalation of conflicts in the Middle East. According to Xinhua News Agency, Israeli Prime Minister Netanyahu pledged to halt attacks on Iran’s energy facilities, stating, ‘I believe this war will end much sooner than people think.’ Trump also indicated that he would not deploy ground troops. As a result, Brent crude oil prices retreated from their highest closing level since July 2022 to around $107 per barrel.

The decline in oil prices has provided some support for assets in emerging markets. After the MSCI Emerging Markets Index plummeted 2.7% on Thursday due to surging oil prices, it showed signs of stabilization on Friday. The currency index for developing countries rose slightly by 0.2%, and both are expected to achieve weekly gains. Nevertheless, inflation worries driven by high energy costs have profoundly altered global monetary policy expectations. Bond markets are no longer pricing in a Fed rate cut this year, while the European Central Bank is even facing pressure to raise rates.

Yesterday, under dual pressures of dashed hopes for a rate cut and liquidity shocks, precious metals like gold experienced fierce sell-offs. Currently, gold prices have stabilized with a slight increase.

Key asset movements are as follows:

In the stock market:

- The MSCI Asia-Pacific Index edged down 0.2% on Friday. The Japanese stock market was closed today.

- South Korea’s Kospi Index once surged over 1% during Friday’s trading session but later pared gains to close up 0.3%, led by Samsung Electronics.

- US stock index futures were almost flat. Most European stock index futures saw slight gains, with the Euro Stoxx 50 Index futures rising 0.6%.

In commodities:

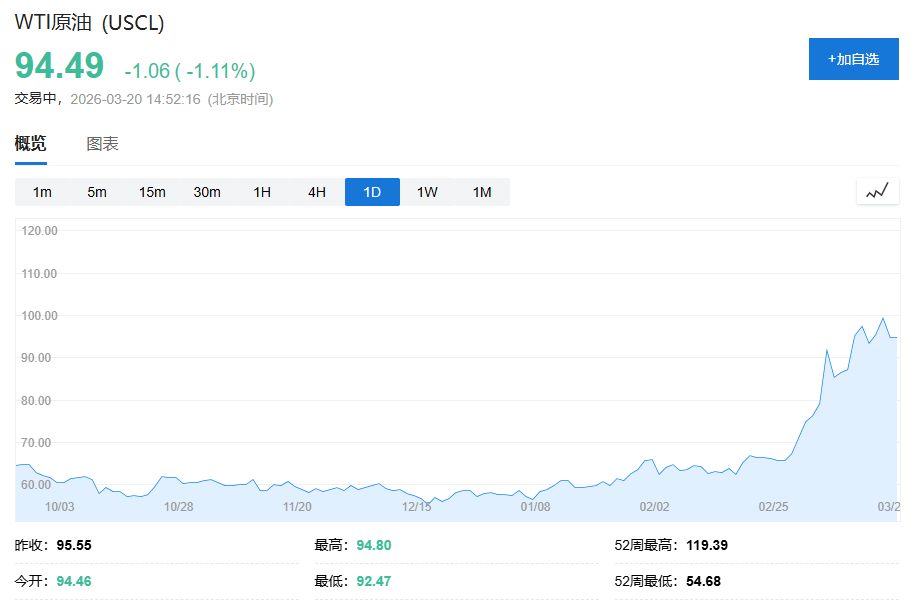

- WTI crude oil is currently down more than 1%, trading at $94.49 per barrel, while Brent crude oil has also seen a slight decline.

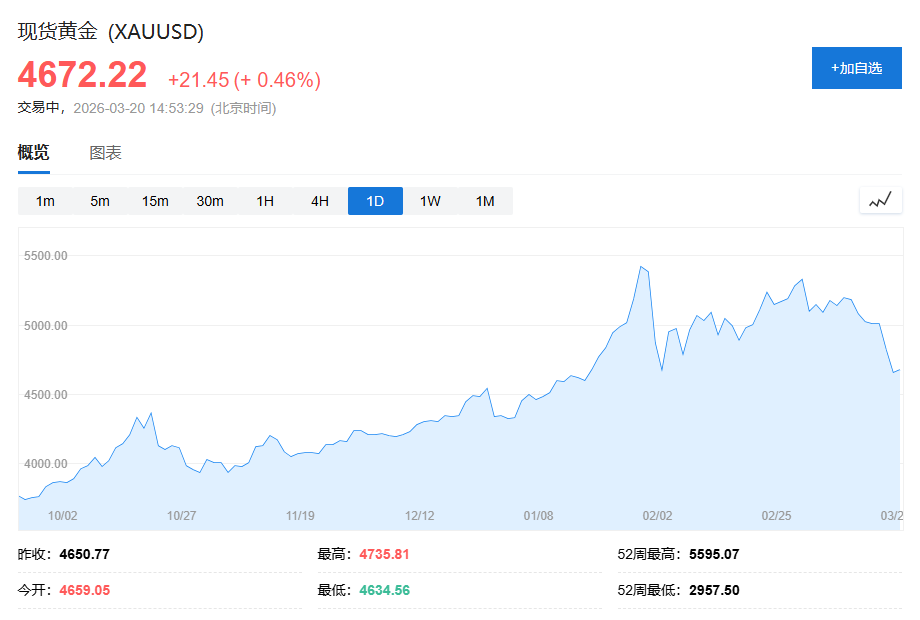

- Spot gold maintained its level near $4,660 after a sharp decline. Silver once fell by nearly 2%.

In the foreign exchange market:

- The Thai Baht led gains among currencies, while offshore Renminbi showed relatively weak performance.

Emerging market assets stabilized.

As oil prices retreated, emerging market assets demonstrated resilience ahead of the weekend. Mitul Kotecha, Head of Asian FX and Emerging Market Macro Strategy at Barclays, noted: ‘Comments from Israeli and U.S. officials helped inject a degree of calm into today’s markets, aiding in the recovery of emerging market assets.’

WTI crude oil is currently down more than 1%, trading at $94.49 per barrel, while Brent crude oil has also seen a slight decline.

Despite increased uncertainty due to geopolitical conflicts, investor sentiment toward emerging markets remains positive overall. A survey by HSBC revealed that the proportion of investors optimistic about emerging market assets has risen to its highest level since January 2021. Vincent Mortier, Chief Investment Officer of Amundi Group, pointed out that factors such as improved government finances and resilient growth expectations are supporting emerging market economies. Currently, emerging market equities account for only around 5% of global asset management, below the long-term average of 7% to 8%, with potential for gradual increases in the future.

In the Asia-Pacific market, South Korea’s Kospi Index rose over 1% on Friday before trimming gains to 0.3%, led by Samsung Electronics and Samsung C&T. The Thai Baht led gains among currencies, while offshore Renminbi showed relatively weak performance. However, weighed down by heavyweights like Alibaba, the MSCI Asia-Pacific Index edged down 0.2% on Friday.

US stock index futures were almost flat. Most European stock index futures saw slight gains, with the Euro Stoxx 50 Index futures rising 0.6%.

Inflation Concerns Reshape Interest Rate Expectations

Although oil prices have retreated in the short term, the impact on energy supply chains remains profound, with global inflation risks surging sharply. This has forced central banks around the world to reassess their monetary policy paths.

According to Reuters, institutions such as JPMorgan, Morgan Stanley, and Barclays have significantly adjusted their interest rate forecasts for the European Central Bank (ECB). Both Barclays and JPMorgan predict that the ECB will raise interest rates at its April policy meeting, followed by further hikes in June and July; Morgan Stanley expects two 25-basis-point rate increases in June and September. This shift stems from the upward inflationary risks brought about by the conflict in the Middle East.

It is not just the ECB; major central banks worldwide have signaled a hawkish stance this week. The Federal Reserve maintained interest rates but adopted a hawkish tone; the Bank of England made it clear that it is ready to “act” against inflation; and Australia’s benchmark bond yields climbed to their highest level in nearly 15 years. Garfield Reynolds, head of Bloomberg MLIV’s Asia team, pointed out: “The signal from the bond market is that any decline in oil prices may be temporary, and supply shocks in oil and natural gas will continue to intensify inflationary pressures.”

Diminished Hopes for Rate Cuts Trigger Precious Metals Selloff

The reversal of interest rate expectations became the core driver behind the plunge in the precious metals market. Since gold does not generate interest income, the contraction of rate cut expectations directly undermined its relative attractiveness.

Aakash Doshi, Global Head of Gold and Metals Strategy at State Street Investment Management, stated: “Before the outbreak of war, money markets expected the Federal Reserve to cut rates twice this year, whereas current market pricing reflects no easing expected this year.”

Spot gold plummeted 3.5% on Thursday, briefly falling to the $4,500 threshold and hitting a six-week low. On Friday, gold prices remained relatively low. Silver fell nearly 2%.

Meanwhile, both retail and institutional investors are simultaneously reducing their exposure to precious metals. According to VandaTrack data, SPDR Gold Shares, the world’s largest gold ETF, has faced net selling from retail investors for six consecutive trading days. Tom Wrobel, Director of Capital Advisory at Societe Generale’s commodity brokerage division, noted that trend-following hedge funds (CTAs) are actively reducing their gold positions amid the current volatile market conditions.

Suki Cooper, Head of Global Commodities Research at Standard Chartered, added that some investors are cashing in on profits following significant price increases in gold and silver over the past two years to offset losses in other assets. Additionally, the strengthening of the US dollar has diverted some capital flows. This selloff is not limited to gold and silver; platinum, palladium, and industrial metals like copper and aluminum have also declined successively, reflecting a systemic downward revision of market expectations for global economic growth.