Google’s Tech Breakthrough Has Created a Stunning Buying Opportunity for Investors. 1 Glorious Stock With Multibagger Potential to Buy Right Away.

Alphabet‘s (GOOG +1.05%) (GOOGL +1.37%) Google has been pushing the envelope in the field of artificial intelligence (AI). The tech giant has not just been using AI across its advertising and cloud computing applications to help boost user engagement and increase advertisers’ returns; it is also making progress on the hardware front.

Specifically, Google has been looking for ways to reduce the cost of AI computing by designing AI processors in-house so it doesn’t have to rely solely on expensive Nvidia chips. And now, it seems that the “Magnificent Seven” company has made another important breakthrough that could substantially lower computing costs.

Image source: Alphabet.

Solving an important bottleneck in the AI infrastructure ecosystem

In the past few years, hyperscalers, AI companies, and smaller data center players have been investing massive amounts in building out cloud infrastructure. However, that rising demand for AI computing capacity has overwhelmed hardware makers’ capacities, leading to shortages of various types of chips.

Memory is one such commodity: Demand has well outstripped what manufacturers can currently supply. That’s not surprising: Large quantities of compute memory, also known as dynamic random-access memory, are needed throughout AI data centers so that their high-end parallel processors can quickly access large datasets from storage to run AI workloads.

Specifically, AI accelerator chips are equipped with specialized high-bandwidth memory (HBM) chips. Manufacturing HBM consumes 3 times the wafer capacity of DRAM chips used in traditional applications. Booming demand for HBM has resulted in a wider supply shortage in the DRAM market that is expected to last for at least the next three years.

This, in turn, has resulted in a steep increase in DRAM prices.

Similarly, AI model training and inference applications are driving a massive increase in demand for NAND flash storage. According to an estimate by the researchers at MarketsandMarkets, the AI-centric storage market could increase in value by close to 800% between 2025 and 2035. Just as in the DRAM market, NAND flash is also experiencing a supply shortage.

However, Google claims that its TurboQuant technology can reduce the memory required for training large language models (LLMs) by “at least a factor of six,” as reported by Bloomberg. It remains to be seen when Google will deploy this algorithm, but the news that it could reduce the storage requirements in AI data centers has hammered the shares of Sandisk (SNDK +3.28%).

Today’s Change

(3.28%) $23.04

Current Price

$724.63

Key Data Points

Market Cap

$107B

Day’s Range

$711.00 – $736.00

52wk Range

$28.27 – $777.60

Volume

416K

Avg Vol

20M

Gross Margin

34.81%

Sandisk makes NAND flash storage products that are used in numerous applications, ranging from smartphones to personal computers (PCs) to gaming consoles to data centers. Its revenue and earnings have grown rapidly due to the NAND flash supply crunch, driven by eye-popping demand from AI data centers.

Investors are worried that Google’s new tech could dent Sandisk’s business, potentially leading to a drop in memory prices and crushing the company’s margins. But investors who are selling Sandisk stock are probably making a mistake.

Google’s storage algorithm could be a good thing for Sandisk

Morgan Stanley analyst Shawn Kim asserts that a potential drop in memory prices would actually be a good thing for Sandisk. Kim believes that lower memory prices could lead to increased AI consumption, as that would mean that companies could charge users less for AI solutions. He referred to the Jevons Paradox, which holds that lower resource costs lead to increased consumption.

This concept came back into the limelight last year after the emergence of DeepSeek’s cost-efficient AI model — an event that took a bite out of Nvidia’s stock price. Nvidia has been focused on reducing the cost of AI compute and inference since then, and the company continues to enjoy strong demand for its chips.

Sandisk could witness something similar if Google’s software can indeed achieve what it claims. After all, AI adoption is expected to increase steadily, driven by the productivity gains the technology can deliver. In the U.S., for instance, AI usage by businesses is forecast to jump to 22.1% by July from 18.2% in January, according to the U.S. Census Bureau.

AI adoption should continue heading higher in the long run, as according to IDC, each dollar spent on AI services and solutions could generate $4.90 in value. So, lowering the costs of the hardware needed to train and run AI applications should spur faster adoption of the technology, creating a long-term tailwind for Sandisk.

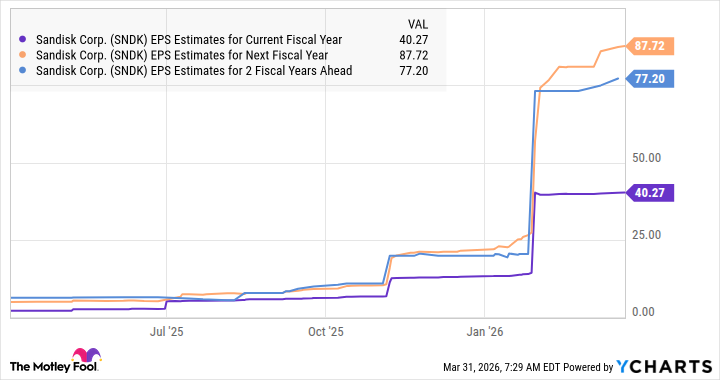

That’s why it would be a good idea to buy this AI stock following its recent pullback. The company has been growing at a solid pace, and analysts are expecting its earnings to jump to $40.27 per share in the current fiscal year from $2.99 per share in the previous one. Even better, its bottom line is expected to more than double in the next fiscal year.

SNDK EPS Estimates for Current Fiscal Year data by YCharts.

Of course, the chart above forecasts a drop in Sandisk’s earnings after a couple of years, but that may not actually occur, given robust storage demand. In fact, smartphone giants Apple and Huawei are reportedly packing in more storage into their smartphones to support AI workloads, despite the supply crunch.

So, if more memory becomes available due to the tech breakthrough that Google is claiming, Sandisk will be better able to meet the memory demands of manufacturers of smartphones and PCs, two areas that are witnessing a supply crunch. That could pave the way for sustained earnings growth. Sandisk may even outpace analysts’ expectations in the long run.

That’s the reason why it would be a good idea to buy this tech stock while it is trading at just 18 times expected forward earnings, a discount to the S&P 500 index’s forward earnings multiple of 20.4. Sandisk is extremely cheap given its outstanding earnings growth.

Even if its earnings do slip from their peak after a couple of years to $77.20 per share, if the stock at that point trades in line with the S&P 500 index’s average forward earnings multiple, its stock price would be around $1,575. That’s 2.7 times its current stock price, suggesting that investors who buy in now are getting an investment with multibagger potential.