Is CoreWeave a Buy 1 Year After Its IPO?

CoreWeave (CRWV +8.06%) exploded onto the investing scene just over a year ago. The artificial intelligence (AI) infrastructure company launched its initial public offering in late March 2025 — and, with the company raising $1.5 billion, it was the biggest U.S. technology IPO in four years.

Customers have flocked to CoreWeave as it’s offering something in great need these days: capacity to run AI workloads. CoreWeave gives customers the opportunity to rent powerful graphics processing units (GPUs) as needed, and as a result, revenue has skyrocketed.

So now, one year after the company’s IPO, it’s a great idea to consider what’s happened so far, what may lie ahead, and whether the stock is a buy right now.

Image source: Getty Images.

CoreWeave’s position in the AI story

Let’s start by looking at how CoreWeave fits into the AI story. The company is an infrastructure player, but it’s different from cloud giants such as Amazon and Microsoft. While they offer customers a broad range of AI and non-AI services, CoreWeave focuses specifically on AI workloads — this allows the company to differentiate itself from the big guys and carve out a niche.

It’s also important to note that demand for AI chips has been so great that there’s plenty of business for market giants and smaller players. In fact, all of these players have one thing in common: They must quickly invest in infrastructure build-out to keep up with demand.

All of this demand can be seen in CoreWeave’s latest earnings reports. The company has reported triple-digit gains in revenue and, in recent times, has announced major contract wins. Last week, CoreWeave announced an agreement with Anthropic to support the development of its Claude AI models. This means CoreWeave is now working with nine of the 10 major AI model providers.

Today’s Change

(8.06%) $8.22

Current Price

$110.22

Key Data Points

Market Cap

$58B

Day’s Range

$103.88 – $114.09

52wk Range

$33.52 – $187.00

Volume

12K

Avg Vol

28M

Gross Margin

47.77%

A deal with Meta

CoreWeave may see demand from companies that don’t have their own GPUs or even market giants that do — but need additional infrastructure for their workloads. For example, AI powerhouse Meta Platforms has its own data centers but requires such enormous capacity that it’s turned to CoreWeave for support. Last week, Meta expanded its cloud capacity agreement with CoreWeave, announcing a $21 billion deal through 2032.

Tech giants have said they aim to spend nearly $700 billion this year as they scale up infrastructure, and smaller cloud players such as CoreWeave could benefit from the need for compute.

It’s also important to note that CoreWeave works closely with Nvidia and was the first to make the Blackwell and Blackwell Ultra products generally available. So customers know that if they turn to CoreWeave they may gain early access to the top chip designer’s latest GPUs.

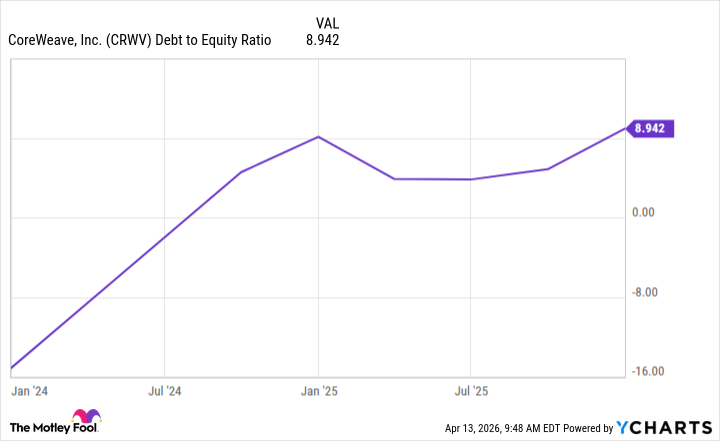

Now, to make all of this happen, CoreWeave has to invest heavily in infrastructure, and to do that, it relies significantly on debt. Its debt-to-equity ratio shows it’s highly leveraged, leaning on debt to fund its operations.

CRWV Debt to Equity Ratio data by YCharts

Some investors have shied away from investing in CoreWeave due to this dependence on debt. That said, CoreWeave has said that its investments aren’t being done to serve potential demand but instead to serve contracted backlog, which has reached more than $66 billion.

Demand remains strong

And cloud companies — from small players such as CoreWeave to the market giants I’ve mentioned here — all have spoken of solid demand from customers. So there’s reason to believe that CoreWeave’s revenue will keep climbing.

Now, let’s consider stock performance. The IPO came at a time when the overall market faced uncertainty. President Donald Trump had announced his plan to set tariffs on imported goods, and that hurt many stocks — particularly growth-oriented ones. So CoreWeave didn’t immediately soar, though the stock went on to climb about 300% in the months that followed its market launch.

The company, like peers, faced general concerns about AI spending later in the year, and this, along with worries about CoreWeave’s reliance on debt, has weighed on the stock periodically. Still, CoreWeave is up more than 175% since its IPO.

Considering all of this, is the stock a buy today? This depends on your investment strategy. If you’re a cautious investor, CoreWeave isn’t the best choice for you — until the company moves closer to profitability, you might want to keep it on your watch list. But aggressive investors who don’t mind some volatility might scoop up a few shares as this company could be in the very early stages of an exciting growth story.