Latham (NASDAQ:SWIM) Reports Sales Below Analyst Estimates In Q1 CY2026 Earnings

Reports Sales Below Analyst Estimates In Q1 CY2026 Earnings")

Residential swimming pool manufacturer Latham (NASDAQ:SWIM) missed Wall Street’s revenue expectations in Q1 CY2026, but sales rose 5.3% year on year to $117.3 million. On the other hand, the company’s outlook for the full year was close to analysts’ estimates with revenue guided to $595 million at the midpoint. Its GAAP loss of $0.07 per share was in line with analysts’ consensus estimates.

Is now the time to buy Latham? Find out in our full research report.

Latham (SWIM) Q1 CY2026 Highlights:

- Revenue: $117.3 million vs analyst estimates of $119.2 million (5.3% year-on-year growth, 1.6% miss)

- EPS (GAAP): -$0.07 vs analyst estimates of -$0.07 (in line)

- Adjusted EBITDA: $12.16 million vs analyst estimates of $12.88 million (10.4% margin, 5.6% miss)

- The company reconfirmed its revenue guidance for the full year of $595 million at the midpoint

- EBITDA guidance for the full year is $112.5 million at the midpoint, above analyst estimates of $110.4 million

- Operating Margin: -5.6%, down from -4.4% in the same quarter last year

- Free Cash Flow was -$58.22 million compared to -$50.33 million in the same quarter last year

- Market Capitalization: $678.4 million

Commenting on the results, Sean Gadd, President and CEO, said, “We continue to execute effectively on our strategic priorities and achieved sales growth in each of our product lines in the first quarter. Sales growth was led by gains in autocovers and liners and the benefits of the Freedom Pools acquisition, while adverse weather conditions in North America kept organic in-ground pool sales steady year-over-year. Adjusted EBITDA growth outpaced sales growth by a considerable margin, demonstrating Latham’s substantial operating leverage and cost discipline, which more than offset the impact of higher investments in growth initiatives.

Company Overview

Started as a family business, Latham (NASDAQ:SWIM) is a global designer and manufacturer of in-ground residential swimming pools and related products.

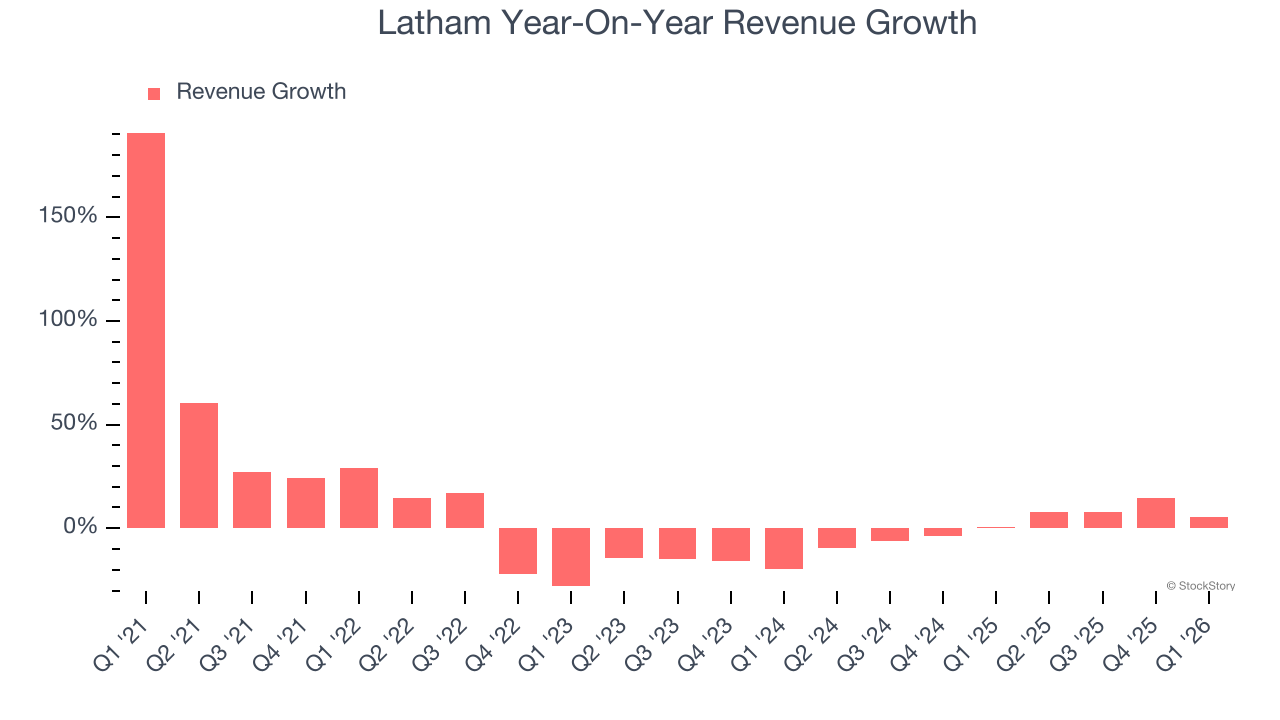

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Latham grew its sales at a weak 2% compounded annual growth rate. This was below our standards and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Latham’s annualized revenue growth of 1.1% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Latham’s revenue grew by 5.3% year on year to $117.3 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.2% over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

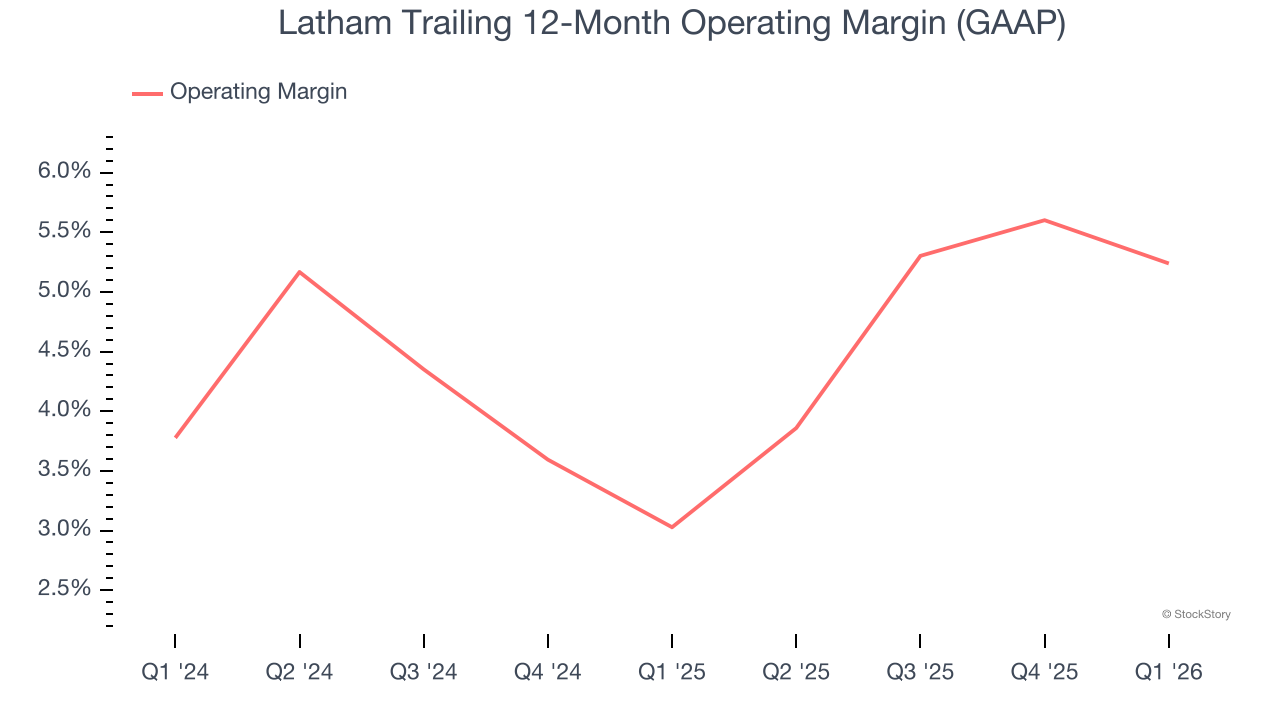

Operating Margin

Latham’s operating margin has been trending up over the last 12 months and averaged 4.2% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q1, Latham generated an operating margin profit margin of negative 5.6%, down 1.2 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

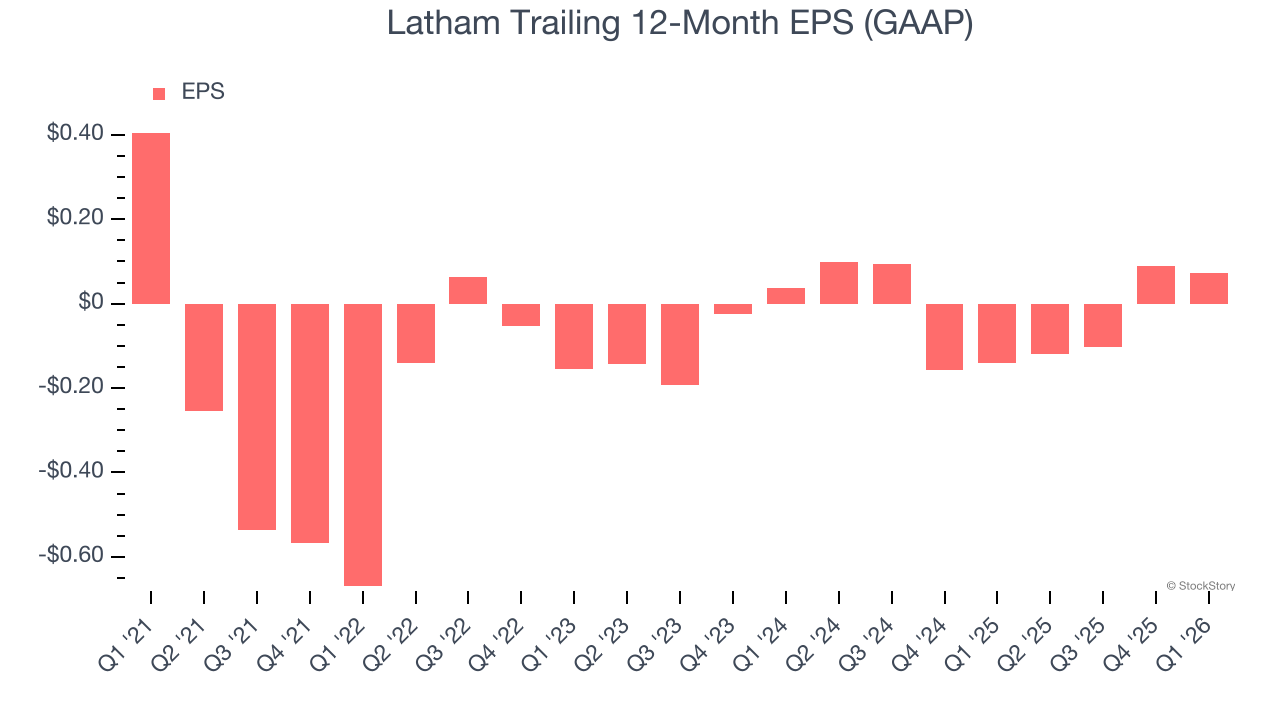

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Latham, its EPS declined by 29.3% annually over the last five years while its revenue grew by 2%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q1, Latham reported EPS of negative $0.07, down from negative $0.05 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 2.9%. Over the next 12 months, Wall Street expects Latham’s full-year EPS of $0.07 to grow 116%.

Key Takeaways from Latham’s Q1 Results

It was encouraging to see Latham’s full-year EBITDA guidance beat analysts’ expectations. We were also glad its full-year revenue guidance was in line with Wall Street’s estimates. On the other hand, its adjusted operating income missed and its revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $5.86 immediately following the results.

Is Latham an attractive investment opportunity at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

Is Up 17.4% After Strong Q2 Earnings And Steady Dividend Confirmation")

: Buy, Sell, or Hold Post Q1 Earnings?")