Sun Pharma-Organon deal: Outlook is mixed

Sun Pharma’s agreement to acquire all outstanding shares of NYSE-listed Organon & Co for $14 per share in a cash deal, implies an enterprise value of $11.75 billion for Organon. This includes $3.99 billion in market cap and nearly $8-billion debt of target company. Sun Pharma will finance the deal with its cash of $2-2.5 billion and the remaining through debt, which should increase net debt to EBITDA to 2.3 times of the combined entity versus current -1.44 times (negative due to net cash in balance sheet) for Sun Pharma in Q2FY26.

In the past, Sun Pharma acquired proven early-stage products, which had a clear growth outlook. Ilumya in 2014, Concert Pharmaceuticals in 2023 ($576 million primarily for Leqselvi) and Checkpoint Therapeutics in 2025 ($355 million primarily for Unloxcyt). These pointed acquisitions have performed well for the company with products ramping in sales. With Organon, the company is acquiring an established, but a slow-growing company with several product lines across multiple geographies while assuming significant debt.

Organon

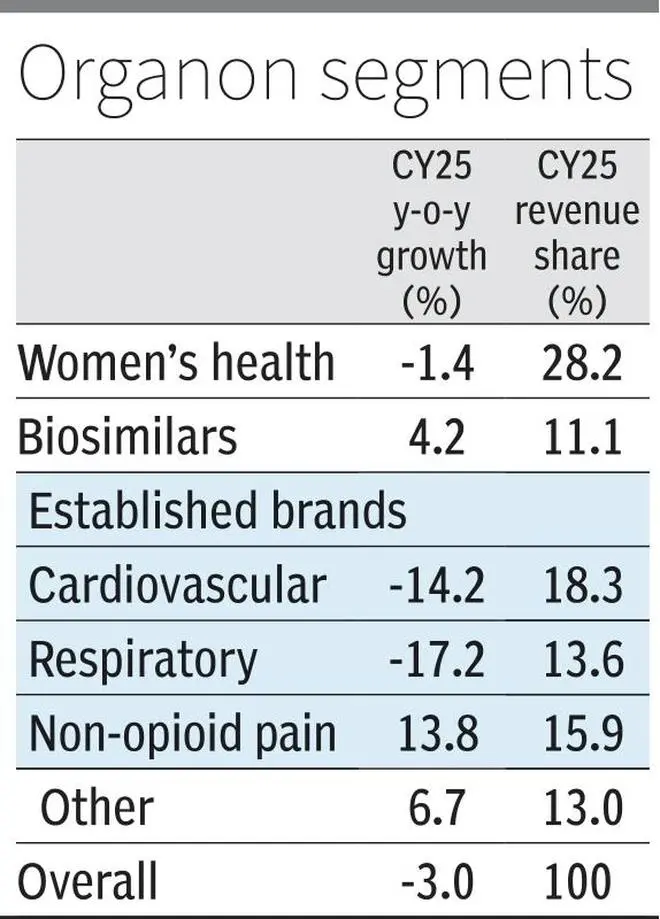

Organon is a multinational pharmaceutical with a leading position in the US in women’s health, including contraceptives (second position) and fertility (third position). It has strong presence in the US, the EU, China, Canada, Brazil and 140-plus countries with manufacturing base in Europe and EM — six sites. The segment break-up is as shown in the table.

The company reported muted revenue CAGR of -1 per cent in FY20-25, with FY25 revenue of $6.2 billion. The FY25 EBITDA margin of 30 per cent has declined from 47 per cent in FY20, attributed to loss of exclusivity for its large products. With a high debt burden (net debt to EBITDA of 6.5 times in FY25) and declining margins, the company reported net income CAGR of negative 20 per cent in FY20-25.

The weak financial performance is the reason for an EV of $11.75 billion for Organon compared to Sun Pharma, which also reported $6.2 billion in sales and 30 per cent EBITDA margin in FY25 but has an EV of $42 billion.

Deal outlook

Sun Pharma expects the acquisition to be EPS-accretive in the first year, which can be based on the following factors.

Firstly, the scale of operations will nearly double in revenue and EBITDA, and by 1.8 times in free cash flow for the combined entity. The company, in its initial assessment, expects $350 million in cost synergies.

Organon has a wider presence compared to Sun Pharma. A front-end presence in Europe and close to $800-million sales in China for Organon, being the most advantageous for Sun Pharma. The two entities can cross-sell their largely non-overlapping portfolio in these markets.

The combined entity will have a strong sales force of 24,000 personnel. Sun Pharma expects to leverage this strength by onboarding in-licenced products (late-stage biosimilars or innovative medicine, for instance).

Organon’s established brands business operates several generics facing high generic competition but strong market share in the US, China and Europe, which Sun Pharma expects to replicate for its portfolio. Also, the company has a strong product development capability but held back by debt concerns.

Sun Pharma also gets access to a sizeable biosimilars platform which it has not developed.

On the other hand, there are concerns as well. As shown in the table, Women’s Health, Cardiovascular, Respiratory segments are declining. The company should outline a plan to revive growth in these segments, and support growth in biosimilars, opioid and other segments.

The largest product Nexplanon (15 per cent of FY25 revenues) has several growth headwinds. The company studies established a five-year efficacy compared to three years earlier. While this is positive, short-term growth will be impacted. The lower allocation of public funds to Planned Parenthood – a large buyer could impact the sales as well. The company CEO resigned in October 2025 owing to concerns on practices relating to sales to wholesalers for the product in CY22 and CY24. While the issue has settled, the overhang should be monitored.

Also, Singular, its large respiratory product, faces a restricted warning in the US and reported 30 per cent decline in 2025.

Overcoming product-level challenges, restarting R&D (discontinued early-stage R&D programme in view of debt), supporting growth in established and innovative medicine while repaying debt in an entity that is of similar size to Sun Pharma will be challenging. The 10-12 per cent revenue growth of Sun Pharma will be impacted in the short term, which will impact the valuations as well.

Compared to product additions earlier, Sun Pharma’s current acquisitions present a considerable challenge, although it can more than double its footprint on strong execution. Investors will have to monitor deal progress and, more importantly, the plans for driving growth and paying down debt from the acquisition.

Published on April 27, 2026

Still Undervalued On Its FDA CAM2029 Milestone?")

Nears Key HCM Readout On An Undervalued Narrative")

And Celadon Pharmaceuticals (LSE:CEL) Keeping UK Cannabis Stocks On Watch?")

Vs The Rest Of The Branded Pharmaceuticals Stocks")