The ChiNext Index fell by more than 1%, lithium mining stocks surged with a wave of limit-up trading, the renminbi broke through the 6.84 level, and the Hang Seng Tech Index dropped nearly 1% as technology stocks generally declined.

The concept of superhard materials experienced volatile gains, with Huanghe Whirlwind’s stock rising for two out of three days, Sifangda increasing by over 10%, and Liliang Diamond, Wolude, Boyun New Materials, and Huifeng Diamond following the upward trend. The power sector was active during early trading, led by green electricity stocks. Ganneng Co., Ltd. achieved a two-day consecutive rise, while Funeng Co., Ltd., Huayin Power, Mindong Power, Jinkai New Energy, and South Grid Energy also rose.

Lithium mining stocks surged, with individual stocks triggering a wave of limit-up trading, following an urgent announcement by Zimbabwe’s Ministry of Mines and Mining Development to immediately suspend the export of all raw ore and lithium concentrates.

On February 26, the A-share market experienced volatile declines, with the three major indices collectively falling in the morning session. The ChiNext Index dropped nearly 1%. Lithium extraction from salt lakes and lithium mining stocks surged, while sectors such as semiconductors and photovoltaics adjusted. The Hong Kong stock market saw a volatile pullback, with the Hang Seng Tech Index falling nearly 1%, and most technology stocks declining.

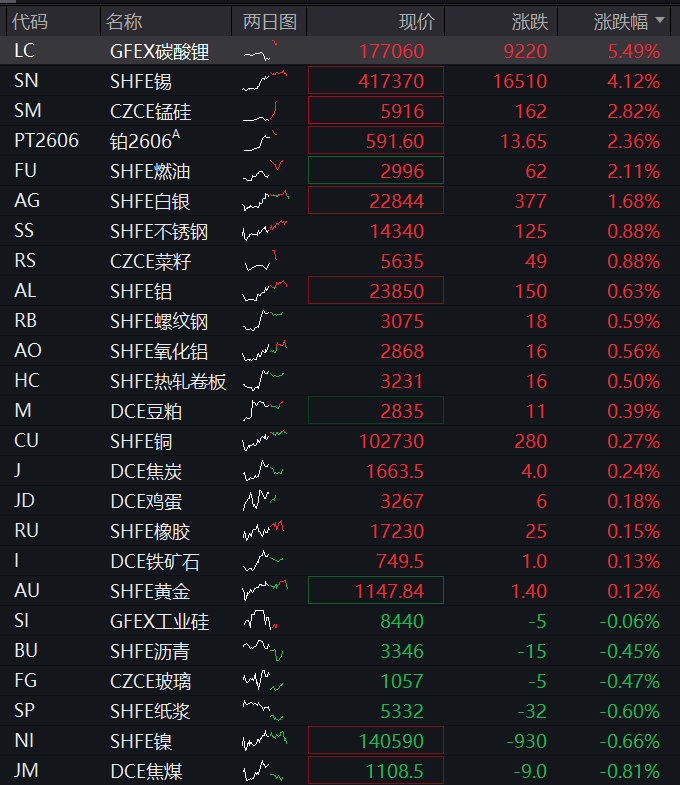

In the bond market, government bond futures fell collectively. In commodities, the majority of domestic commodity futures contracts rose, with lithium carbonate continuing its significant rally, currently up over 5%. In the foreign exchange market, offshore renminbi broke through the 6.84 level, reaching a high of 6.8384. Key market movements:

A-shares: As of press time, the Shanghai Composite Index fell 0.23%, the Shenzhen Component Index dropped 0.35%, and the ChiNext Index declined 1.14%.

Hong Kong stocks: As of press time, the Hang Seng Index fell 0.08%, and the Hang Seng Tech Index dropped 0.96%.

Bond market: Government bond futures fell broadly. As of press time, the 30-year main contract fell 0.29%, the 10-year main contract dropped 0.10%, the 5-year main contract fell 0.06%, and the 2-year main contract declined 0.01%.

Commodities: Most domestic commodity futures rose. As of press time, lithium carbonate gained over 5%, tin futures rose 4%, platinum, fuel oil, and ferrosilicon-manganese increased over 2%, silver futures gained over 1%, and stainless steel, rapeseed, aluminum, alumina, rebar, hot-rolled coil, soybean meal, copper, coke, rubber, eggs, iron ore, and gold also advanced.

09:57

The superhard materials sector saw volatile increases, with Yellow River Whirlwind Co. hitting limit-up for two out of three days, Four Directions Co. surging over 10%, and Power Diamond, Worldtech Advanced Materials, Boyun New Materials, and Huifeng Diamonds following the uptrend.

In terms of news, on February 23, Akash Systems announced the delivery of the world’s first NVIDIA GPU servers equipped with Diamond Cooling technology to NxtGen AI Pvt Ltd, India’s sovereign cloud service provider. These products are based on the NVIDIA H200 platform, marking the world’s first application of ‘diamond thermal conductivity technology’ in commercial AI server systems, achieving breakthrough innovation at the material level.

09:43

Offshore renminbi rose more than 100 points against the US dollar intraday, approaching the 6.84 level, with a high of 6.8421.

09:40

The electric power sector was active in the morning session, with green energy stocks leading the gains. Ganneng Co., Ltd. achieved two consecutive daily limit-ups, while Funeng Co., Ltd., Huayin Electric Power, Mindong Electric Power, Jinkai New Energy, and Southern Power Grid Energy followed with upward momentum.

In terms of updates, the National Energy Administration recently released the 2025 renewable energy grid operation outlook, indicating that by 2025, China’s newly installed renewable energy power generation capacity will reach 452 million kilowatts, a year-on-year increase of 21%, accounting for 83% of the country’s total new power installations.

09:37

The ChiNext Index fell by more than 1%. Photovoltaic, real estate, and fiberglass sectors were among the top decliners, with nearly 2,900 listed companies across the Shanghai, Shenzhen, and Beijing exchanges experiencing declines.

09:28

Lithium mining stocks led the market at the opening bell, with Jinyuan Co., Ltd. hitting the daily limit-up during pre-market trading. Keliyuan, Jiangte Electric Machinery, Dazhong Mining, Rongjie Co., Ltd., Guocheng Mining, and Tianhua New Energy all surged by over 6%.

09:26

The SSE Composite Index opened 0.09% higher, while the ChiNext Index dropped by 0.24%. Non-ferrous metals, chemicals, and steel sectors posted significant gains, with stablecoins, servers, and CPO concept stocks showing strong activity; meanwhile, oil and gas, photovoltaics, and satellite navigation themes weakened.

09:21

The Hang Seng Index opened 0.95% higher, and the Hang Seng Tech Index rose by 0.46%. Tianqi Lithium Industry surged by over 6%, while Ganfeng Lithium Industry increased by more than 5%.

09:01

Commodity futures opened with the main lithium carbonate contract rising by over 11%, tin futures on the Shanghai Futures Exchange up by over 5%, platinum and silver futures rising by over 2%, and fuel oil, aluminum alloy, liquefied petroleum gas, and aluminum futures gaining more than 1%. The Europe Container Shipping Line index fell by over 3%.

Quietly Recasting Its Risk Profile With New Legal And Global Affairs Chiefs?")